FCStone Morning Comments

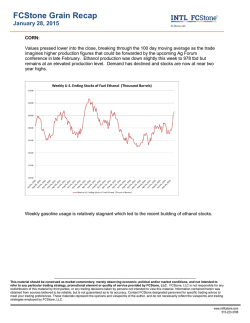

Morning Commentary February 5, 2015 CORN: STEADY We watched the grain complex give away some of the gains from the rally on Tuesday. March corn traded in a ten-cent range closing at down two cents at $3.83 ½. As expected, March gravitated toward the 100-day moving average of $3.78. Funds continued to liquidate longs, now net long 153K contracts. With not a whole lot of market moving news on the horizon, we are intently watching outside market movements. The USD continues to be a market mover for the entire commodity index. Crude retreated yesterday after a friendly stocks report. Ethanol production numbers were down 30K barrels per day and we expect production to continue that trend as producers are starting to feel the fallout from record low crude prices. Export sales came in at the lower end of the estimate at 845K MT vs. expected 800-1000. Milo continues to impress with another 223K MT net sales. Milo has now exceeded USDA annual sales estimate with 28 weeks left in the marketing year. With decent sales numbers and the dollar down a bit this morning expect tight trade. Support for March corn at $3.68 and resistance at $3.88 ½ and then $3.95. As of the break, CH15 was 1 ¾ higher. SOYBEANS: BETTER Export sales are out and the complex has little to be excited about. Though meal and beans were at the top end of the range, the top end of the range was not a tough number to reach. Looking elsewhere, there is not much to get excited about. Status quo pretty much reigns supreme. With the USD only marginally lower, I would not expect much of a bounce from that today. The volumes were all off yesterday across the complex, but damage was most severe in meal OI where over 7K came off the board. Basis is firm if not a tad stronger. Spreads are still range-bound. Tomorrow is the first day of GS roll. Look for better trade early, but both sides to trade following the USD path. Beans: V203,435/OI-704,614(-3,660) Meal: V-80,967/OI-363,430(7,575) Oil: V-96,644/OI-408,307(+1,142) As of the break, SH15 was 5 ¼ higher. WHEAT: HIGHER The wheat market continues to follow outside market factors, as KC is up 5 ½ this morning due to the USD and crude giving support. Weekly export sales came in at the middle of the estimate range with 397K MT sold for 2014/15. U.S. also made sales of 89K MT for 2015/16 marketing year. Taiwan purchased 86K MT of U.S. milling wheat in a tender this morning for Mar-Apr. shipment; varieties included DNS, HRW, and SWW. The UN FAO’s world food price index fell 3.6 points in January to 182.7 points, and its world cereal production for 2014 is pegged at a record high. Look for higher trade today on outside markets; USD down 170 points and Crude Oil up 137 points. The CME Group announced yesterday that most open outcry (pit) trading will close July 2, 2015, after volume of pit trade is down to 1% of total daily futures volume. As of the break, KWH15 was 5 ½ higher. CATTLE: MIXED Following a sharp rally across the commodity complex on Tuesday, most markets gave back a majority of those gains yesterday and the cattle market appeared more than happy to participate. But despite the $1.92 loss yesterday, the most-active Apr. live cattle contract still has not taken out the low set on January 26. Since then Apr. futures have traded in a general $148-152 range and aided bulls with mild relief… On the cash front, we did see packers move bids to $160 in the South yesterday and buy a small quantity of cattle that way. This would be fully steady, or even $1 higher than last week’s market, with most sellers now moving their asking prices to $161-162. This cash strength lent some support to nearby Feb. futures with the Feb/Apr. spread trading all the way out to $4.35 yesterday and fresh contract highs. Look for a mixed start this morning with mostly firmer outside markets. Any developing $161-162 cash trade should help support futures. Fund Position Accumulative Yesterday Corn +153,415 -6,000 Soybeans -11,787 -9,000 Soybean Meal +34,953 -3,000 Soybean Oil +16,048 -1,000 Chicago Wheat -22,819 -2,000 KC Wheat +12,184 N/A This material should be construed as market commentary, merely observing economic, political and/or market conditions, and not intended to refer to any particular trading strategy, promotional element or quality of service provided by FCStone, LLC. FCStone, LLC is not responsible for any redistribution of this material by third parties, or any trading decisions taken by persons not intended to view this material. Information contained herein was obtained from sources believed to be reliable, but is not guaranteed as to its accuracy. Contact FCStone designated personnel for specific trading advice to meet your trading preferences. These materials represent the opinions and viewpoints of the author, and do not necessarily reflect the viewpoints and trading strategies employed by FCStone, LLC. [email protected] [email protected] [email protected] [email protected] [email protected]

© Copyright 2026