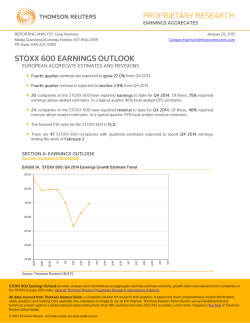

Conference call transcript