December 2014 Quarter Review

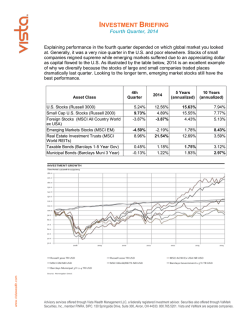

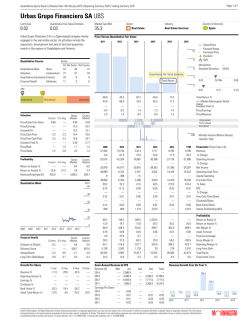

GKV Capital Management Economic and Investment Outlook Fourth Quarter 2014 2014 Year End Review Managing Expectations Dealing With Unpredictability Market Expectations in 2015 GKV Capital Management A note from: PETER VOGEL The bull market continued through 2014, however, it gave several deceptive moments of ending in a sharp downward correction. Although the S&P 500 index advanced by 12% last year it was not a smooth ride. The Ukraine crisis, geopolitical tensions, collapsing oil, diminishing growth around the world except in the United States and the termination of the Federal Reserve bond buying program, and even an Ebola outbreak caused periodic episodes of selling during 2014. Because the bull market was into its fifth year of recovery from its nadir in March 2009, the brief stock market paroxysms described above caused us twice to modestly increase cash reserves and decrease common stock exposure in portfolios. Twice we were wrong. On several occasions the stock market very swiftly fell by more than 5% last year, but it remained resilient and recovered these losses in equally swift ascensions. For long-term investing, patience and selection are critical variables to achieve investment success. In the short-term timing is an additional critical variable. Preservation of capital is a primary investment objective in our portfolios. During the two short but sharp stock price collapses in the first few quarters of 2014 we decreased common stock investments by about 10%. This action proved unnecessary and the reinvesting of these funds back into equities caused a reduction for the year in our common stock investment performance each time by about 2%. In 2007/2008 our quick determination of a change in economic and financial fundamentals allowed us to preserve client assets and to dramatically outperform the S&P 500 index in 2008. The increasingly pervasive high-frequency trading in the stock market has resulted in sudden, overly exaggerated stock price spasms, and twice in the first three quarters of 2014 we were fooled into believing these quick drops in prices were perhaps the harbinger of more long term adverse economic and financial changes. This was not the case, but our modest realignment of stock portfolios last year caused us to underperform the major stock market averages. Although our goal is to achieve performance commensurate with the major indices, this objective is superseded by the need to preserve capital and minimize risk. With this philosophy we will usually underperform a surging bull market but outperform a stable to declining one. If you wish to further discuss our financial outlook and how it pertains to your personal situation, please do not hesitate to contact me at [email protected]. President and Chief Investment Officer GKV Capital Management is an independent registered investment advisor. For more information about us please call (805) 497-2616 or visit gkvcapital.com Page 2 4Q14 Data Points DJIA YTD 7.5% S&P 500 YTD 11.4% NASDAQ YTD 13.4% Int-Term Bond YTD 4.4% 10-Year Treasury Yield 2.2% S&P 500 LTM 2.0% Dividend Yield S&P 500 EPS 2015 EST $131.14 S&P 500 P/E 15.9x Fourth Quarter 2014 Fourth Quarter Review Looking at the year-end results, 2014 was another positive year for investors. However, beneath the surface investors experienced a rollercoaster ride with two major sell-offs that threatened to wipe out all of the gains for the year. After a sharp sell-off in July and again at the end of September, the major indices pushed forward resulting in gains of 11.4% for the S&P 500, 7.5% for the Dow Industrials, and 13.4% for the Nasdaq Composite. It was for us, a difficult year for investment in stocks. The strong run-up in equity valuations in 2013 assumed economic strength in 2014 and into 2015, and was influenced positively by massive economic stimulus. Instead of accelerating growth, economic activity has been merely tepid with a weakening global outlook. The U.S. has remained stronger than the rest of the developed world, but we cannot carry the entire global economy on our own. Additionally the Federal Reserve continued to reduce stimulus finally ending its bond purchase program. consumer spending. U.S. GDP grew by 5% in the September quarter raising expectations that the economic recovery was gaining traction. In the fourth quarter GDP growth increased at an annualized 2.6% rate to bring the full year GDP growth to 2.4%. The fourth quarter growth was driven by a strong acceleration in spending on services and non-durable goods. Corporate earnings throughout 2014 were generally positive due largely to historically high profit margins. Companies have remained lean throughout this recovery but there is no Firm Wide Asset Allocation December 31, 2014 The market was driven forward largely by positive macroeconomic data, particularly by positive employment and Source: GKV Capital Management Ten Year Time Weighted GKV Performance of $100,000 Page 3 Source: GKV Capital Management GKV Capital Management room for increased profits without increased sales. In fact, expectations of strengthening sales never really materialized in 2014 causing earnings forecasts to be reduced throughout the year marginally. For example, earnings estimates on the S&P 500 for 2014 began the year at $121.48 and by December 31st had been revised down to $116.66. While the revised forecast still reflects positive annual earnings growth, we are still waiting for the much anticipated economic reacceleration. Healthcare, biotech, utilities and consumer-oriented shares outperformed in 2014. Energy companies declined sharply in the fourth quarter as the price of oil fell through the floor. The NYSE energy index declined 14% for the year. While geopolitical headline risks seemed to have lessened in the second half of 2014, global economic data has become increasingly negative raising new concerns for global growth prospects and how they might impact U.S. companies. More important has been slowing global GDP growth coupled with a strengthening of the dollar, which reached its highest point in more than four years. While the strength of the dollar is a positive reflection of the strength of the U.S. economy relative to the rest of the world, it has a negative effect on corporate profits for U.S. based companies exporting goods abroad and repatriating foreign profits. rate environment in the long-term, our expectation is predicated on the long awaited acceleration in economic growth. At the current rate, we should anticipate interest rates to remain near current levels through the summer. The low interest rates have had a very positive impact on significant bond holdings in 2014 resulting in fixed income gains of 4.6% for the year. The dramatic drop in the price of oil and energy prices in general resulted in a 0.3% decline in consumer prices in November. Low inflation, a strong dollar and slow growth will likely keep interest rates low. For 2014, positive performance in stocks was largely limited to the U.S. markets. Economic slowdown in China, continued malaise in Europe, and the expectation of rising interest rates in the U.S. resulting in a strengthening dollar all contributed to a sell-off in international markets. The DOW Global-excluding U.S. index posted a decline of 5.5% for the year. Our exposure to equities overall remains significant, closing the year with 53% of assets under management in equities, 38% in fixed income and only 4% in cash. The remaining 5% is in various real estate investments. Interest rates remain low with a 2.2% yield for the 10-year Treasury. While we continue to anticipate a rising interest GKV Performance 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 GKV Bonds 2.0% 4.5% 4.7% -1.6% 9.9% 5.4% 5.0% 6.9% 2.5% 6.5% Int Term Bonds 1.8% 4.2% 4.7% -4.7% 14.0% 7.7% 5.9% 6.9% 0.0% 4.4% GKV Stocks 5.7% 9.1% 17.4% -36.4% 28.1% 5.23% 3.0% 8.1% 28.5% 5.0% S&P 500 3.0% 13.6% 3.5% -38.5% 23.5% 12.9% 0.0% 13.4% 29.6% 11.4% GKV Total Acct* 2.5% 5.0% 8.0% -8.3% 9.2% 3.7% 3.2% 5.4% 12.2% 4.9% 10 Year Total 2004-2014 Annual 56.1% 4.6% 53.4% 4.4% 74.4% 5.7% 69.6% 5.4% 54.4% 4.4% Source: GKV Capital Management, December 31st, 2014 *GKV Total Account Performance calculated after fees Page 4 Fourth Quarter 2014 Managing Expectations “The financial markets generally are unpredictable. So that one has to have different scenarios... The idea that you can actually predict what's going to happen contradicts my way of looking at the market.” - George Soros “Generally unpredictable.” We find it hard to believe that Mr. Soros fully believes the quote attributed to him above. After all, what reasonable person commits vast sums of wealth to something unpredictable? We suppose it would depend on a broad or narrow interpretation of what is meant by the word “generally.” While the quote may be easily misinterpreted out of context, we are in agreement with Mr. Soros. The markets are generally unpredictable and anyone stating that they “know” with any certainty future investment returns doesn’t really know anything. And while predictions, both ours and others, are continually wrong, the overall long-term trend has been consistent. Investors make money over time with patience and diligence. Managing investments keeps you humble. Mistakes will be made and the worst ones occur when you most think you have everything all figured out. Our favorite example in recent history is the spectacular failure of Long-Term Capital Management in 1998. Run by ex-Solomon Brothers head of bond trading, John Merriweather, and with two Nobel laureates on the board, Myron Scholes and Robert Merton, the hedge fund completely unraveled, losing $4.6 billion in less than four months. Initially very successful, the hedge fund returned 21% in its first year, 43% the second, 41% in the third before going to zero. We have to confess, it is more fun highlighting others’ more spectacular mistakes to make you feel better about your own less significant failures. Value of $1,000 Invested at LTCM Although the markets are generally unpredictable and nothing can be known with certainty, we do have certain expectations in regards to investment performance or there would be no reason to invest at all. These expectations differ from one individual to another, but for the most part, investors expect to make a positive return over time. There is always the risk of loss, but the responsible investor should expect to be rewarded for their risk. To further define a reasonable expectation without bringing mathematics into the picture, most investors would claim that they expect at least a return commensurate with other investors taking similar risk. In other words, it is reasonable to expect to make 8% annually in the stock market if everyone else is making 8% in the stock market. We take our responsibility very seriously. Most of our clients will not have the time or the capability to recover from significant losses. We are always nervous about protecting our clients and yet we have to take risk in order to grow assets. While we have gotten used to making minor investment mistakes over the decades we are continually learning new lessons and striving to face our shortcomings. Our approach to taking risk is to manage that risk so that in the case of a failure the outcome is not cataclysmic. In any endeavor, you must survive to be able to learn from your mistakes. As a teenager you learn to drive and to the consternation of every parent, you learn the biggest lessons through some close calls. As long as you survive to learn the lessons, you become a better driver. The average career on Wall Street is short lived. Some managers, like Long-Term Capital management have cataclysmic failures. Most have mediocre performance. Some have trouble being wrong and have difficulty evaluating the requisite risks. This business is a struggle, but it’s that challenge that gets us in the door every day. We take a conservative approach to managing portfolios and to manage risk we diversify our clients’ assets generally between stock and bonds, and at times in real-estate investment vehicles. We further diversify portfolios in various industries or in the case of bonds with different issuing entities and maturities. At the close of 2014, firm wide, 38% of clients’ assets were invested in bonds, 54% in equities and 4% in cash. Each of these major asset classes have different characteristics and carry different risks and expectations. By utilizing a blend of Page 5 GKV Capital Management these security types we are able to reduce the volatility of a portfolio. Therefore, our total results, stocks, bonds and cash combined, tend to perform somewhere between the major stock indexes and the major bond indexes. S&P 500 Annual Performance Although the markets are unpredictable there are certain reasonable expectations for returns based on long-term performance results. As the disclaimer goes, past performance cannot predict future returns, but it can and should serve as a guide. Looking at the S&P500 since 1958, stocks in the index have yielded an annual return of 7.1% excluding dividends. As the chart on this page shows, the volatility of the index is tremendous making the market “generally” unpredictable. The standard deviation over the period is 16.6%, meaning that two-thirds of the time the market will be up 8.5% +/- 16% and a full one-third of the time it will be up or down even more! By contrast, the bond market has produced stable returns, 4.7% over the last 10 years with considerably lower volatility as measured by the standard deviation during the period of 3.2%. Two-thirds of the time bonds have returned between 1.5% and 7.9% in the last ten years. While this is materially Stocks vs. Bonds—Returns and Volatility* lower than the S&P500 return of 7.7% over the same period, the sleepless nights have been far fewer. Investment professionals will point out that with the specter of rising interest rates, bonds may produce sub-par results in the coming decade, however our point is that we are using various security types to reduce volatility and manage risk. We have been steadily reducing our fixed income holdings as interest rates have bottomed. As a portfolio manager, we expect our returns for equities to be roughly commensurate with the major stock indexes. We expect our bond portfolio to perform roughly in line with the major relevant bond index. We expect the blend of stocks and bonds to yield a less volatile long-term gain that is likely to trail the stock indexes when they are up significantly and to be far better than the stock indexes when they are down. For example in 2008 when the S&P500 declined 39%, our accounts, after fees, declined only 8%. The stocks we held in 2008 declined 36%, which is a little better than the index but because we held few stocks, our overall performance was far superior. Conversely, in 2013, when the S&P500 was up 30%, our accounts were up 12%. The stocks we held in our accounts gained 29%, again we matched the index, but because our accounts were not 100% stocks, our total account performance was lower. We are managing assets to protect wealth and grow assets responsibility over time. Looking at the last 10 years, we find that the reduced volatility came at a very small price to performance. The compound annual growth for all GKV managed accounts was 4.4% after fees, from December 31st, 2004 to December 31st, 2014. Over the same period, the S&P500 gained only 5.4% and the Barclays Intermediate-Term Index gained 4.4%. The complete 10 year data is available on the chart on page 4 of this report. The historical statistics can tell us a lot about the market and should be used to guide our expectations. We are striving to manage assets in a responsible manner and avoid the mistake of trying to swing for the fences and chase unreasonable returns. All this is not to say we are infallible and don’t make mistakes. To the contrary, 2014 was a tough year for us as our equity investments underperformed the major indices. Across all accounts, our equity portfolio was up 5% versus 11% for the S&P500. In our effort to protect capital we reacted to swings in the market too hastily. While not a disaster, we are disappointed nonetheless. We expect 2015 to be another challenging year with slow growth in the U.S. and slower growth globally. The prospect of increasing interest rates and a strengthening dollar may put further pressure on stock valuations and corporate earnings. Page 6 *S&P500 and Barclays Intermediate-Term Bond Index Fourth Quarter 2014 Looking Forward The economic outlook remains positive although there is little to get excited about. With the reduction in stimulus to propel stock valuations, we expect stock prices to track earnings growth. Unfortunately, we are concerned about corporate earnings going into 2015. Since the significant recession in 2008, earnings have recovered nicely, driving the stock market to new highs. The current recovery has been unusual by historical standards in both its tepid growth and long duration. We believe that the slower than typical growth has made the longer than usual duration of this recovery both possible and reasonable. Corporate earnings recovered dramatically after the recession and have continued to increase in subsequent years driving the equity markets higher. However much of the earnings growth has come from increases in profitability rather than growth in revenues. The growth rate of earnings is slowing as we reach limits in corporate profit margins. This coupled with weakness in the rest of the world has prompted companies to reduce their earnings outlook for 2015. S&P 500 Performance and Earnings Growth what might look like an expensive market a reasonable value. Conversely, if the forecast is too rosy, then the market isn’t worth what investors are currently paying and the value will adjust. While it is entirely possible that revenue growth could accelerate with earnings improving as 2015 progresses, we have been experiencing the opposite trend with continual reductions in estimated earnings. Until recently the reductions have been slight. We remain positive for the overall outlook for the U.S. economy and the prospects of individual companies, but given the trends in earnings, we think double digit gains for the major indices will be difficult to achieve in 2015. The S&P 500 closed the year at 2,051 which is 16.9x the earnings forecast for the next twelve months based on the latest revised earnings forecast of $121.31. We find this valuation to be expensive. Consider that at the start of 2014, the S&P500 was trading at 16.0x the latest 2014 forecast of $115.77. We find little reason, given the slower earnings growth expectations in 2015 for the market to be trading at a premium to year-ago levels. A 16x multiple puts the S&P500 at 1,941. We expect individual stock selection to be critical for performance in 2015. We are focusing our attention in subsectors of healthcare, technology, biotech, and select companies with superior growth prospects. We expect to reduce our exposure to stocks marginally to hedge the risk of a significant correction. We anticipate a positive 2015, but like 2014 the slow growth and reduced earnings expectations may lead to significant volatility. Since the close of the year, largely due to the dramatic reduction in the price of oil, we have seen a fairly dramatic reduction in earnings estimates. From an initial 2015 forecast for the S&P500 of $137.19 made in March of 2014, the current forecast has been reduced to $121.31, an 11.6% reduction. This figure represents only 4.7% growth over the current 2014 estimate of $115.77 which is hardly enough to propel the stock market to dramatic new highs, in our opinion. The earnings estimates and growth rates are important because they drive what investors should be willing to pay for equities. If growth accelerates, greater future earnings make Page 7 S&P 500 Earnings Estimate Revision History Personal Portfolio Management Southern California 125 Auburn Ct. Suite 200 Westlake Village, CA 91362 Northern California 2950 Buskirk Ave. Suite 300 Walnut Creek, CA 94597 GKV Capital Management is a registered advisory firm operating since 1975. We manage separate accounts for families, charities and retirement. Four of the largest asset bubbles have occurred in the last 25 years. Volatility has taken a significant toll on investment assets requiring new strategies to protect and grow wealth. As an independent portfolio management firm making direct investments on our clients’ behalf, GKV Capital has the flexibility and expertise to respond to the changing investment environment to reduce risk, minimize losses and grow wealth. Phone: 805-497-2616 Fax: 805-379-3216 E-mail: [email protected] Our Investment Philosophy We take a dynamic view of the macro economy to determine expected returns in the near-term of various asset classes. Within these classes individual investments are selected for clients’ accounts on an account by account basis. We do not buy and hold, but seek to take advantage of changes in market sentiment and fundamentals to avoid losses and create opportunity. As an independent portfolio manager we have the flexibility to adjust investment exposure rapidly. We make direct investments on behalf of our clients buying individual securities, generally stocks and bonds eliminating costly mutual fund fees. We are a fee-only advisor, we do not receive commission and we do not sell any financial products. Client assets are held at an unaffiliated brokerage firm. GKV Capital Management is a registered investment advisor with the SEC under the 1940 act. This newsletter provides general investment information and is not intended to provide specific financial, investment, legal, or tax advice. Any discussion of individual securities should not be taken as a recommendation for any reader to buy or sell such securities. You should consult with your own advisor and/or do your own research before acting on any of our opinions, which we change without notice. The data provided in this newsletter is believed to be reliable, but are not guaranteed as to accuracy or completeness. The value of the securities mentioned herein may fall or rise and are not insured by any government or private company. ©2015 GKV Capital Management Company Inc.

© Copyright 2026