Daily Market Commentary

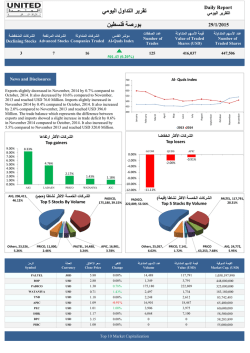

ABC 02 February 2015 Sri Lanka Sri Lanka Markets Update Daily Market Note Domestic Markets HSBC research is available online: USD/LKR spot closed at 133.10/40 against an opening level of 133.35/65. Spot opened trading today at 133.20/45 and is currently trading at 133.12/32. Overnight liquidity was a surplus of LKR 31.1 Bio and O/N Money averaged at 5.84% Source : Reuters (24/11/14) Internet http://www.hsbcnet.com http://www.hsbc.lk Reuters HSBS Disclaimer This report must be read with the disclaimer, disclosures and analyst certifications on p5 that form part of it. Issued by The Hongkong and Shanghai Banking Corporation Limited. Source : Reuters (24/11/14) Regional Currency Performance against USD LKR -0.27% THB -0.24% Contacts -0.05% BDT INR 0.39% IDR 0% 0% 0% 0% 0% 0% Local currency depreciation/appreciation 0.21% 0% 0% 0% Source : Reuters (01/01/14 to 24/11/14) Point to point inflation came at 3.2%, up from 2.1% in December while annual average inflation came at 3.2% down from 3.3% in December PUBLIC Head of Sales Perry Savundranayagam 1% 2421697, 2334222, 2325435 Corporate Sales Eraj Rajapakse DO Arundhaka Dep Rajiv Jayawardena DO DO Santhush Weerakoon DO Email–[email protected] ABC Sri Lanka Markets Update USD/LKR Spot-closing (27 Jan 2015)=133.15/40 Inter-Bank call money ( 27 Jan 2015) 5.82% USD/LKR forward Premiums Treasury Bill Rates – Auction rates - net of tax SLIBOR 3 mth 145/175 cents 6 mth 280/320 cents 12 mth 535/595 cents 3 mth 6 mth 12 mth USD Sovereign Bond 2015 2020 O/Night 1 Month 3 Month 6 Month 12 Month 5.80% (5.80%) 5.90% (5.90%) 6.05% (6.05%) 3.04% 4.62% 5.91% 6.29% 6.57% 6.82% 7.10% Economic Indicators All share Price index S&P SL 20 Index Daily Turnover 7,180.05 down by 196.46 points (-2.66%) 3,962.24 down by 172.46 points (-4.17%) Rs. 2,065.17 million CBSL SDFR CBSL SLFR Statutory Reserve Ratio(SRR) 6.50% (January 2014) 8.00% (January 2014) 6.00% (June 2013) Consumers Price Index Inflation y-o-y % Inflation 12m moving ave 180.20 (Dec 2014) 1.6% (October 2014) 3.8% (October 2014) GDP Growth Gross Official Reserves Government Revenue Government Expenduture Unemployment 7.70% (2014 3Q) $ 7.37 Bn (Dec 2014) $ 8.75 Bn (2013 CBSL Annual Report) $ 12.84 Bn (2013 CBSL Annual Report) 4.5% (2014 2Q) Outstanding External debt $ 39.7 Bn (2013 CBSL Annual Report) Exports $ 898.50 mn (Oct 2014) Imports $ 1750.20 mn (Oct 2014) Trade Deficit $ -851.70 mn (Oct 2014) Derivatives – IRS (Bid) USD 0.6950 1.3240 1.8050 2 Year 5 Year 10 Year Central Bank rates NZD 3.50% GBP 0.50% CAD 0.75% CHF -0.75% GBP 0.8670 1.2621 1.5827 AUD USD EUR JPY AUD 2.4175 2.6100 2.9020 EUR 0.1088 0.2988 0.7238 2.50% 0.25% 0.05% 0.00% Stock Markets International Currency Markets DJI (USA) Nikkei 225 FTSE 100 17,813.98 (1.48%) 17,511.75 (1.05%) 6,796.63 (1.02%) USD/JPY GBP/USD EUR/USD AUD/USD USD/CAD Commodity Markets LIBOR - USD Gold IPE brent WTI 3 mth 6 mth 12mth $ 1,280.50 $ 49.06 $ 46.79 117.64 1.5078 1.1310 0.7783 1.2734 0.2526% 0.3554% 0.6224% US Treasuries Asian Currencies 5 yr 10yr 1.3240% 1.7810% USD/IDR USD/INR 12,690 61.84 30yr 2.1420% USD/THB 32.56 Source: Reuters/Daily FT *All rates above are for indicative purposes only. 2 PUBLIC Sri Lanka Markets Update ABC FX Edge More central bank easing; the downside of USD strength Central banks continue to surprise markets with policy easings, including Russia today and Denmark on Thursday. Dollar strength is getting some blame for downside misses on US corporate earnings. That has implications for FX hedging, but it could also have political and monetary policy ramifications down the road. Russia cuts rates Central banks continue to surprise with easing measures. Russia's central bank cut its policy rate 200bp to 15%, despite surging inflation which roughly doubled during 2014 to 11.4% and a persistently weak ruble. The central bank said the cut is due a change in the balance of risks and it now sees inflation peaking in Q2 and decelerating thereafter. That may well pan out over time but in the near-term, cutting rates in an environment of still-high inflation and general RUB weakness would mostly seem to increase risk that each of those respective trends persist. But more broadly, the rate cut continues the trend of policy easings and/or dovish shifts by central banks around the world. Denmark cut again; we expect the EUR-DKK peg to hold On Thursday, Denmark's central bank cut its rate on certificates of deposit to -0.50% from 0.35%. The cut follows the two previous 15bp cuts on January 19 and 22, as the rate had been held at -0.05% since last September. The Danish central bank also acknowledged intervening in the FX market to defend the EUR-DKK peg. EUR-DKK has stabilized above 7.44 in the past week but that may have been assisted by FX intervention, and with the DKK continuing to trade on the strong side of the 7.46 peg, the central bank felt the need to take additional measures in the form of yet another rate cut. There is measurably increased interest in the DKK since the Swiss National Bank removed the cap on the CHF, with some speculating that the EUR-DKK peg could break and the krone appreciate more markedly. We recognize the new risks to EUR-DKK that have materialized on the back of the SNB policy change as well as the weaker EUR ramifications of ECB QE, and it is not surprising to see the market put more pressure on the currency pair. But Denmark's position is different from that of Switzerland's and we expect the DKK peg to hold, for several reasons. The EUR-DKK peg has much greater longevity than the CHF ceiling, dating to the launch of the EUR in 1999 as part of ERM-II, which replaced the DKK's previous link to the deutschemark, which commits it to trade within a 2.25% band on either side of 7.4603. DKK flows and volumes are much smaller than the CHF which makes it an easier currency for authorities to defend. And it has the support of Denmark's central bank as well as the ECB, while the CHF ceiling was a unilateral policy enforced only by the SNB. None of this precludes the potential for markets to test the resolve of Danish and Eurozone policy makers, but we see a much better chance that they can collectively hold the EUR-DKK peg. USD strength and US corporate earnings; motivation to hedge Dollar strength continues to get attention--and blame--for downside misses in US corporate earnings. That is not too surprising in hindsight, given the sizeable scope of the USD's rally in the past year. In essence, even those companies which expected some USD strength in 2014 probably did not forecast, budget and hedge to sufficiently account for the full extent of the currency's appreciation. For example, at the end of 2013, a period when many US corporates would have completed their forecasted FX budget rates for end-2014, the consensus forecasts for EUR-USD 3 PUBLIC Sri Lanka Markets Update ABC was 1.2800, compared to its actual 2014 close near 1.2100. For USD-JPY, the end-2014 consensus forecast in December 2013 was 109.00, well below where it finished this past December at 119.74. There are a variety of implications stemming from the forecast-miss, but we will highlight just three. First, with the USD remaining strong, and currently trading at measurably stronger levels against most currencies just since the end of Q3 2014, US corporates are likely to be more active hedgers, which mostly translates into more USD buying. That could be more evident during calendar periods such as month-end (this week) and quarter-end. But the upshot is that, to some extent, USD strength begets more strength. Strong USD and the political fallout Second, US industry will not necessarily take USD strength and the associated hit to corporate earnings lying down, especially if there is the perception that the USD's gains are stemming from policies abroad that are actively weakening foreign currencies. There has already been stepped up pressure from Congress on the Obama administration to put more focus on currencies and currency manipulation in the current negotiations for the Trans-Pacific Partnership trade agreement. And continued USD strength could well see Congress put broader pressure on the US Treasury (i.e. beyond specific trade agreements) to take a more active stance against those countries which are viewed as intentionally driving their currencies down, such as naming them manipulators in Treasury's semi-annual FX report (the next one is due in April). That seems most unlikely since no country has been named as a currency manipulator since 1994 (i.e. the bar is very high). And just last Friday, after the ECB announcement of QE, Treasury Sec. Lew reaffirmed that "a strong USD is "good for America." But if Treasury won't act, Congress may take matters into its own hands. Legislation aimed at countering currency manipulation abroad often has a reasonable amount of support from both Republicans and Democrats, and that could be the more likely risk going forward. If political pressure and focus on currencies intensifies, it will be one potentially important development that could create headwinds for the USD. The Fed is also watching Third, this week's FOMC statement added "international developments" in the list of items the Fed will consider in judging the appropriate stance of monetary policy. That makes perfect sense given the risks from weaker foreign growth and global disinflation pressures. Within that broad array of issues, USD strength is another factor adding to downward pressure on already-low US inflation. The Fed does not target the USD but if gains in the currency create too much downside pressure and risk to prices, it is one condition that would argue for a delay in the start of Fed tightening. If such a sequence develops--and we have already seen markets push back the expected start date of Fed lift-off in the past month--that too would potential temper USD strength. 4 PUBLIC Sri Lanka Markets Update This document is issued by The Hongkong and Shanghai Banking Corporation Limited (HSBC). The information contained herein is derived from sources we believe to be reliable, but which we have not independently verified. HSBC makes no representation or warranty (express or implied) of any nature nor is any responsibility of any kind accepted with respect to the completeness or accuracy of any information, projection, representation or warranty (expressed or implied) in, or omission from, this document. No liability is accepted whatsoever for any direct, indirect or consequential loss arising from the use of this document. Any examples given are for the purposes of illustration only. The opinions, if any, in this document constitute our present judgement, which is subject to change without notice. This document does not constitute an offer or solicitation for, or advice that you should enter into, the purchase or sale of any security, commodity or other investment product or investment agreement, or any other contract, agreement or structure whatsoever and is intended for institutional customers and is not intended for the use of private customers. The document is intended to be distributed in its entirety. This document is not a research report or a document for giving of investment advice. No consideration has been given to the particular investment objectives, financial situation or particular needs of any recipient. Unless governing law permits otherwise, you must contact a HSBC Group member in your home jurisdiction if you wish to use HSBC Group services in effecting a transaction in any investment mentioned in this document. This document, which is not for public circulation, must not be copied, transferred or the content disclosed, to any third party and is not intended for use by any person other than the intended recipient or the intended recipient's professional advisers for the purposes of advising the intended recipient hereon. Copyright. The Hongkong and Shanghai Banking Corporation Limited 2011. ALL RIGHTS RESERVED. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of The Hongkong and Shanghai Banking Corporation 5 Limited. ABC The Hongkong and Shanghai Banking Corporation Limited Address:No 24 Sir Baron Jayatilake Mawatha, Colombo 1 Tel: +94 112 421697 Fax:+94 114 793575 Website: www.hsbcnet.com Website: www.research.hsbc.com PUBLIC

© Copyright 2026