Trade is weak, with some chances of revival

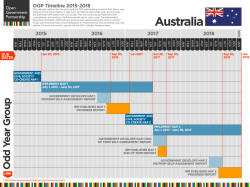

Trade is weak, with some chances of revival Despite lower oil prices, the USD appreciation will help the GCC strengthen its relationship with Asia. World: Trade & GDP %chg, YoY 25 %chg, YoY 5 Since 2011 20 World Trade 4 World GDP (rhs) Sep‐14 Jul‐14 May‐14 Mar‐14 Jan‐14 Nov‐13 Sep‐13 Jul‐13 May‐13 Mar‐13 Jan‐13 Nov‐12 Sep‐12 Jul‐12 May‐12 Mar‐12 ‐1 Jan‐12 ‐5 Nov‐11 0 Sep‐11 0 Jul‐11 1 May‐11 5 Mar‐11 2 Jan‐11 10 Nov‐10 3 Sep‐10 15 Source: Asiya Research on Datastream, 2015. www.asiyainvestments.com/research The global economy never fully recovered from the financial crisis. Following the temporary rebound in 2010, world real gross domestic product (GDP) grew by a mere 2.5% per annum, compared to an annual average growth rate of 3.1% in the twenty years leading to 2007. The global economy remained weak in 2014 with no major change expected for this year. In fact, many organizations have begun downgrading their outlooks for 2015. This month, the World Bank cut its forecast for global GDP growth this year from 3.4% to 3.0%, which still remains high compared to other forecasters. Despite economic strength in the US, UK and India, the rest of the global economy will remain weak; namely in the euro zone, Japan and BRIC economies (Brazil, Russia, India and China). In the last two years, global trade, the sum of world exports and imports, hardly expanded. According to International Monetary Fund (IMF) figures, trade grew 2.6% YoY in the nine months leading to September 2014, 1.5% in 2013 and 0.5% in 2012. Although the trend is positive, the growth rate is still much lower than the pre‐crisis average of 9.3% YoY (1988‐2007). Cyclical factors are one reason behind the slowdown in global trade and its bearish outlook. On one hand, the subpar consumption growth rates in major economies will translate in lower import demand, hampering export‐intensive economies. On the other hand, lower oil and other commodity prices is dampening the reported trade numbers even if the quantity sold is unchanged. Oil exporters such as the GCC are already affected by lower export rates. The weakness in trade is also partly due to a structural shift. First, the two largest economies (US and China) have managed to attract larger parts of the supply chain. Because more products are produced domestically they need to import and export less. This is evident in the decline in Chinese imports of parts and components – from 60% of total imports in the mid‐1990s to 35% today – and the reduction in US manufacturing imports as a share of total imports. Second, it has become more difficult to finance trades since the crisis. Recent financial crime regulations have limited trade flows. Higher capital requirements under Basel III planned to be implemented in 2019 also suggest constraints ahead. According to a 2014 International Chamber of Commerce survey, 71% of banks expect export finance to be negatively affected by these changes. In order to return to the double‐digit trade growth rates witnessed before the crisis, some of these structural challenges need to be addressed. Cyclical factors however can rapidly change. Current market trends may help some economies exit today’s business cycle stage earlier than expected. First, lower oil prices; slashed prices should boost the disposable income of net energy importers, such as China, India, the euro zone, Japan and, to a lesser extent, the US, helping boost trade volumes. Second, the US dollar appreciation; the stronger dollar will facilitate the depreciation of most currencies, creating greater competitiveness for these economies and boost exports. These two market trends are widely expected to continue this year and may support trade levels. Given the current global environment, a surge back to pre‐crisis trade growth rates is unlikely in the short‐term. However, as the US and China reduce their reliance on trade and regulations come into play, world trade will expand, although in a more fragmented and selective manner. Given the current market trends, winners in the short‐term will be the Asia’s less developed economies, such as the ASEAN countries, who will take advantage of the lower oil prices, and the GCC, who will be protected by the US dollar peg. These two regions will continue to benefit from their competitive advantage. In a period of weak global trade, the GCC and emerging Asian trade partnership is becoming increasingly important. Prepared by Camille Accad ‐ For more information please visit: www.asiyainvestments.com or email: [email protected]. Asiya Investments is an Asia‐focused investment company. Licensed and regulated by the Central Bank of Kuwait, it facilitates capital flows between the Middle East and emerging Asia by providing financial and advisory services, and managing third party capital. IMPORTANT DISCLAIMER: The information contained in this report is prepared by the Research Department of the Asiya Investments is believed to be reliable, but its accuracy and completeness are not warranted. Research recommendations do not constitute financial advice nor extend offers to participate in any specific investment on any particular terms. Investors should consider this material as only a single factor in making their decisions. About KCIC: Asiya Investments is a subsidiary of KCIC which was founded by an Emiree Decree with a capital of KD 80 million and a mandate to invest in domestic demand‐driven sectors in Asia, namely energy, real estate, healthcare, infrastructure, and financial services. KCIC is the Parent Company of a Group that includes Asiya Investments Dubai Limited and Asiya Investments Hong Kong Limited. Asiya Investments Dubai Limited serves as the investment advisory hub for KCIC. Asiya Investments Hong Kong Limited is fully equipped with a skillful and experienced investment team which has further demonstrated KCIC's commitment to the Asian markets. The publicly‐listed Group employs a team of Asia specialists and currently manages assets in excess of a billion. Key shareholders of KCIC include the Kuwait Investment Authority (Kuwait's Sovereign Wealth Fund), National Investments Company (one of the leading investment banks in the Middle East), and Alghanim Industries (one of the largest conglomerates in the Middle East).

© Copyright 2026