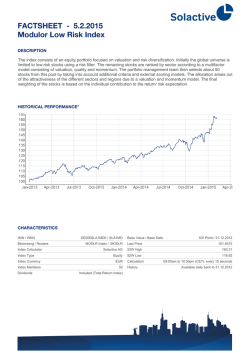

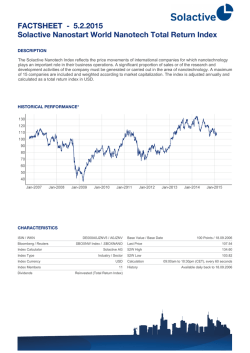

The alternative way to diversify your portfolio

Australian Financial Review, Australia 28 Jan 2015, by James Dunn Smart Investor, page 19 - 1,097.00 cm² National - circulation 62,455 (MTWTFS) Copyright Agency licensed copy (www.copyright.com.au) ID 365894775 PAGE 1 of 4 The alternative wayto diversify your portfolio Investment Thinking outside the box can protect you from market-related shocks. James Dunn It happens in art, fashion, music, literature, so why not investment? Eventually, the "alternative" becomes mainstream. Alternative investments are those that are not the traditional building blocks of a portfolio, being shares, cash, bonds and property. As they have different returns streams from mainstream investments, such as equities and bonds, where payments in the form of coupons or dividends can generally be expected every six months, alternatives can diversify a portfolio. They can also have a low - or even negative - correlation to the traditional investments, so at times when all the traditional markets appear to tear downwards at once, allocations to alternatives may move to a much lesser extent (low correlation) or move in the opposite direction (negative correlation). This ability to absorb shocks can take the risk out of portfolios. But alternatives are not without risk. The term alternative investments is usually taken to include: • Hedge funds, which are managed funds that can invest across many different markets and strategies, with maximum flexibility, so they can make money regardless of what the share and bond markets are doing. They can lose money, too. • Managed futures/commodity trading adviser (CTAs) strategies. • Absolute-return equity-based funds, such as long-short funds, which will simultaneously go long (buy) under-valued stocks and short (sell) over-valued securities, and "marketneutral" funds, which try to deliver above-market returns with lower risk by hedging out market risk, looking to negate the impact and risk of general market movements, trying to isolate the pure returns of individual stocks. • Private equity, being capital invested in a private company which is not yet listed on the sharemarket This is also known as "venture capital", which is really a private equity investment made at a very early stage. • Infrastructure assets, where income streams can be generous but not without risk. • High-yield assets, for example, funds that invest in distressed debt, junk bonds and mezzanine debt • Commodities, such as precious and base metals, oil and energy and soft (agricultural) commodities. • Agribusiness, such as investment in forestry, farming or horticultural businesses. • Art and other collectible items, such as coins and wine. More recently, the range of alternative assets available has been widened to include investment in insurancelinked securities (the value of which is driven by insurance events); water entitlements (traded in the Australian water market); social impact investments, where the investment both earns a financial return and generates a targeted positive social outcome; shipping funds; aircraft and other equipment leasing; weatherrelated derivatives; volatility derivatives, and; carbon trading. "Broadly speaking, you can really consider 'alternatives' to be an investment that produces a return stream that is very differentto that produced by equities or bonds," says Craig Stanford, head of alternative investments at Ibbotson Associates. "We look for assets with low correlation, but correlation isn't the only important thing - beta to the sharemarket is quite important as well. At times you may want a bit of sensitivity to stock market moves. The problem with having an investment that is negatively correlated to the stock market all the time is that you lose money when the stock market rises consistently." Inspired by endowment funds The move to alternative investments was pioneered by the big US endowment funds, which manage money on behalf of institutions such as Harvard, Yale and Stanford universities. Over the past 25 years these funds have diversified into large holdings in hedge funds, private equity and "real assets" (real estate and managed timberland), in a bid to insulate the funds from sharemarket moves by picking up diverse "illiquidity" premiums. Australian super funds began moving into the alternative investment space in the mid-1990s, looking for portfolio diversification and non-correlated returns. Alex Dunnin, executive director of research and compliance at research firm Rainmaker, says die proportion of Australian managed funds held in alternatives has risen from 10 per cent in September 2004 to 18 per cent in September 2014, led by the non-profit (industry fund) superannuation sector, which has lifted its allocation from 6 per cent to 17 per cent over that time. In contrast, the retail super funds have lagged behind, with 1 per cent in 2004 rising to 11 per cent in September 2014. "The retail funds have finally come on board," Dunnin says. "An interesting aspect here, though, is that when the non-profit funds get into alternatives they tend to do so through private equity and infrastructure, while retail funds tend to use hedge funds and commodities-presumably because the non-profit funds are happy having alternative 'real' assets, even if they aren't as liquid as they would like, while the retail funds are very reluctant to sacrifice liquidity." But despite the rise in the alternatives allocation, super funds are "still Australian Financial Review, Australia 28 Jan 2015, by James Dunn Smart Investor, page 19 - 1,097.00 cm² National - circulation 62,455 (MTWTFS) Copyright Agency licensed copy (www.copyright.com.au) ID 365894775 as hog-tied to equity risk as ever", Dunnin says. "Sharemarket and super fund returns are still 90 per cent correlated, suggesting that the alternative assets [that] funds are buying are very closely linked to equity markets." That may mean the equity market is just the lead indicator for the economy more broadly, Dunnin suggests, and that it is not possible to diversify away equity risk. "But with only about onethird of funds' asset-class investments beating their asset class benchmarks, the funds that want to beat the market are going to have to rethink what they invest in, and how," he says. Daniel Liptak, chief executive at specialist alternatives investment consultancy ZG Advisors, says it is this high sharemarket correlation that is "baked in" to Australian portfolios that makes "some form of non-correlated return" necessary. "In Australia, there are really only 10 equity managed funds that do 80 per cent to 90 per cent of the daily volume on the Australian Securities Exchange, and really only the top 20 companies in Australia that are of interest to offshore investors, because they are large enough to invest in," Liptak says. "As we know, one of the best free kicks anyone can have is a well diversified portfolio, but you're not diversified if you don't have something that's not correlated to the market's returns because those returns are at the whims of the largest investors." Liptak advocates using some of the Australian equity market-neutral funds, and some of the managed futures/CTA offerings. "The best market-neutral managers have an excellent record, going back 14 to 15 years, of considerably outperforming the ASX200 Accumulation Index, and they are completely non-correlated to the market. They also have very low correlation to each other, such that it is actually possible to build a more diversified portfolio by investing in several of them." Considering the CTAs The other place to look at would be the CTAs/managed futures. The best of them clearly and demonstrably have low correlation to the market, and they've consistently worked in the past "They follow trends, so last year they were short commodities - they made PAGE 2 of 4 lots of money on the commodities fall. They tend to be on the other side of an equity fall - they tend to make money when shares start falling," he says. Liptak is also interested in newer alternative exposures such as water, social impact investing and shipping funds. "Water makes a lot of sense, it's completely uncorrelated returns, and it's a fairly unique opportunity for Australian investors, because we have such a large and sophisticated water trading market. Social impact investing is also very interesting; again, it is uncorrelated returns, but there just haven't been that many done yet, and it's still at the super fund/highContinued next page Sharemarket and super fund returns are still 90 per cent correlated, suggesting the alternative assets funds are buying are very closely linked to equity markets. Alex Dunnin, Rainmaker Australian Financial Review, Australia 28 Jan 2015, by James Dunn Smart Investor, page 19 - 1,097.00 cm² National - circulation 62,455 (MTWTFS) Copyright Agency licensed copy (www.copyright.com.au) ID 365894775 PAGE 3 of 4 Manv routes to riches Australian alternative investment funds, 12 months to Dec 31 (%) Water makes a lot of sense for its completely uncorrelated returns and it's a fairly unique opportunity for Australian investors because we have such a large and sophisticated water ling market Equity-based alternatives Non-equity-based alternatives Fund of alternative funds A5X total return SOURCE: ZG ADVISORS From previous page The alternative path to a diverse portfolio net-worth/family office investor level." Another spot to get uhcorrelated returns is in shipping funds, he says, but again, it's hard for retail investors to get into that area. Liptak also likes the concept of insurance-linked securities, and volatility exposure, as a "nice spot to make uncorrelated returns, as well". But he adds, "your manager needs to be good". Gary Brader, chief investment officer of QBE, is looking to place up to $100 million of his $31 billion QBE investment portfolio in social impact bonds, to help diversify its assets. "Intuitively it is highly likely that the performance of these sorts of assets will not be correlated to anything else we own, so fundamentally and technically there is a compelling argument for this kind of investment" he says. Alexander McNab, director of Blue Sky Alternative Investments, says that for retail investors, alternative investments can be both a shock absorber and a return generator. "The traditional Australian Financial Review, Australia 28 Jan 2015, by James Dunn Smart Investor, page 19 - 1,097.00 cm² National - circulation 62,455 (MTWTFS) Copyright Agency licensed copy (www.copyright.com.au) ID 365894775 approach to managing risk is dialling up or down your allocation to government bonds. Increasing that reduces the overall portfolio risk, but because government bonds have a low expected return; you lower the overall expected return of the portfolio," he says. The problem with the full menu of alternative exposures, he says, is access and liquidity. "The challenge for retail investors up until now has been that if you wanted to allocate to alternatives, how would you do it? If you look across private equity, infrastructure, the vast majority of managers have focused on institutional funds, rather than vehicles for retail investors. Plus there are issues with liquidity. "The business model for a financial planner revolves around platforms. Platforms demand liquidity and daily pricing and so on. But you're beginning to see the emergence of alternatives vehicles aimed at retail investors; for example, listed investment companies [LJCs] and exchangetraded products tETPs]." Last year, Blue Sky launched Blue Sky Alternative Access Fund Limited (ASX code: BAF), an LIC giving investors access to a range of alternative asset classes, including private equity, venture capital, water entitlements and infrastructure, hedge funds and real estate. "We wanted to offer retail investors and SMSFs exposure to alternatives, but through a liquid vehicle," McNab says. Likewise, ETPs have given investors a simple, cheap and transparent means of gaining exposure to commodities, through a single stock. Some are physical ETPs - backed by a holding of the commodity - while more recent offerings are synthetic ETPs, which use derivatives - for example, indices over futures contracts or swaps -to generate returns from a much wider range of major commodities, for example the agricultural commodities, the industrial metals and the energy commodities, which cannot be owned physically by retail investors. Andrew Spence, senior investment adviser at Hillross CBD in Sydney, uses commodity ETPs as a portfolio diversifier and inflation hedge for SMSF and wealthy investor clients. "The story for us in commodities is one of low-tonegative correlation, and protection from inflation. We wanted an alternatives allocation that will hold the portfo- PAGE 4 of 4 lio together, and make it more robust in a downturn or a left-field event like the [global financial crisis]," he says. FBA020 Blue Sky's Alex McNab: alternatives can be a shock absorber, PHOTO: BEN RUSHTON

© Copyright 2026