presentación - AAP

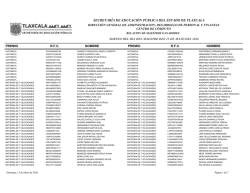

Information | Analytics | Expertise DICIEMBRE, 2014 PERSPECTIVAS DE LA INDUSTRIA AUTOMOTRIZ –PERÚ Lima, Peru Guido Vildozo, Manager Latin America Light Vehicle Sales Forecasts, IHS © 2014 IHS / ALL RIGHTS RESERVED Agenda • Entorno Económico • Perspectiva Global de la Industria Automotriz • Ciclos de plataformas/plataformas globales • Ventas Regionales • Ventas Perú • Conclusión © 2014 IHS 2 Crecimiento Económico –Mundial El pesimismo ha incrementado Annual real GDP growth in % 9.0 2013 2014 2015 Avg 2016-21 8.0 7.0 6.0 5.0 World average 2014 = 2.7% 4.0 3.0 2.0 1.0 0.0 -1.0 World United States Japan Eurozone Brazil Russia India China Forecast change since third-quarter 2014 World 2014 2015 Avg 16-21 -0.1 -0.3 -0.1 United States 0.1 -0.3 -0.1 Japan Eurozone Brazil Russia India China -0.2 -0.1 0.0 -0.1 -0.2 0.0 -0.8 -0.5 -0.6 0.6 -2.6 -0.1 0.1 0.3 0.1 -0.2 -0.3 -0.4 Source: IHS Economics © 2014 IHS Tasas de Desempleo Economías BRIC perfilan incremento en desempleo 16 14 October 2014 Percent, 2010-14 Unemployment rate 12 10 8 6 4 2 0 China Japan Russia United States Brazil Eurozone Germany Source: IHS Economics, monthly, in percent, historical actuals and current estimate © 2014 IHS Índice Inflacionario Expectativas inflacionarias han disminuido 16 14 Percent, 2010-14 CPI annual change 12 10 October 2014 8 6 4 2 0 -2 China India Japan Russia United States Brazil Eurozone Source: IHS Economics, monthly index annual percentage change, historical actual and current estimate © 2014 IHS Índices de Manufactura Estancamiento en China Purchasing managers’ indexes (Index, over 50 indicates expansion) Index, over 50 signals expansion 60 55 50 45 40 35 30 25 2006 2007 2008 2009 United States 2010 Eurozone 2011 2012 China 2013 2014 Japan Sources: Institute for Supply Management (US), Markit, National Bureau of Statistics (China) © 2014 IHS 6 World Outlook/ November 2014 Índices de Materias Primas No solo impacta petróleo Industrial materials prices IHS weekly indexes, 2002:1=1 6 5 4 3 2 1 0 2002 2004 2006 All industrial materials © 2014 IHS 2008 Chemicals 2010 2012 2014 Nonferrous metals 7 World Outlook/ November 2014 Índices de Cambio de Moneda Devaluaciones pronunciadas USD/local currency, 2013:1=100 Weekly exchange rate index 105 100 95 90 85 80 75 70 65 60 Jan-13 Apr-13 China © 2014 IHS Jul-13 India Oct-13 Brazil Jan-14 Apr-14 Russia Jul-14 Oct-14 South Africa 8 Dinámica de precio de petróleo Débil a corto plazo • Baja demanda en China Riesgos • Producción en NAFTA ha incrementado • Recuperación de producción en Libia • Arabia Saudita opta por incrementar producción • Incremento en exportaciones de Irán • Aceleración de la economía global • Tensión geo-politica (Iraq, Irán, Libia, Nigeria, Venezuela, etc.) • Costes de producción mas elevados © 2014 IHS Precio de Brent/Barril Caída en demanda fue repentina, incertidumbre en industria 140 US dollars per barrel 120 100 80 Q3 Forecast New Forecast 60 40 20 0 2000 2003 2006 2009 2012 2015 2018 2021 Source: IHS Energy, quarterly data © 2014 IHS Riesgos macroeconómicos Riesgo Síntomas China se estanca • Sector bancario colapsa. • Burbuja inmobiliaria. • Estimulo fiscal gubernamental. Eurozona vuelve a recesión • Problemas bancarios se intensifican. • Grecia deja la unión. • Contagio llega a Italia, Portugal, o Francia. Shock en precio de Petróleo • Conflictos en Medio Oriente o África. • Incremento repentino. • Rusia. Estados Unidos deja de crecer • Consumidor se pone conservador. • Crecimiento salarial se estanca. • Crisis inmobiliaria retorna. © 2014 IHS jun-2005 sep-2005 dic-2005 mar-2006 jun-2006 sep-2006 dic-2006 mar-2007 jun-2007 sep-2007 dic-2007 mar-2008 jun-2008 sep-2008 dic-2008 mar-2009 jun-2009 sep-2009 dic-2009 mar-2010 jun-2010 sep-2010 dic-2010 mar-2011 jun-2011 sep-2011 dic-2011 mar-2012 jun-2012 sep-2012 dic-2012 mar-2013 jun-2013 sep-2013 dic-2013 mar-2014 jun-2014 Light vehicle sales Millones Ventas globales a ritmo anualizado Mercado impulsado por EEUU y China primordialmente 90 85 80 Source: IHS © 2014 IHS SAAR Global 75 70 65 60 SAAR sin China 55 50 45 40 © 2014 IHS 12 Ventas regionales a ritmo anualizado Los BRICs han desacelerado 2.8 Seasonally Adjusted Selling Rates Indexed 2007=1 2.6 ASEAN C Europe E Europe Gr China India Japan Korea Mid-East/Africa N America S America W Europe GC 2.4 2.2 Lehman Collapse 2.0 1.8 1.6 1.4 AS 2007 Sales Level IN SA 1.2 JK MEA NA EE WE 1.0 0.8 CE 0.6 Jan'14 Jan'13 Jan'12 Jan'11 Jan'10 Jan'09 Jan'08 Jan'07 0.4 Source: IHS Analysis, X12 Seasonal Adjustment © 2014 IHS 13 Million units Ventas globales 2013-2014 87.2 + 0.2 - 0.2 + 0.4 86.7 - 0.6 + 0.6 - 0.7 86.2 + 1.0 85.7 85.7 85.2 + 1.9 84.7 +3% 84.2 83.7 83.2 83.3 2013 © 2014 IHS Greater China North America West Europe Middle East/Africa Japan/Korea South Asia Central/East Europe South America 2014 14 Ventas globales Venderemos 200 millones de unidades adicionales! 110 Total sales 2006-13: Annual sales, in millions 100 577 million vehicles Total sales 2014-21: 767 million vehicles 90 88.6 85.7 80 70 60 2021 2020 2019 2018 2017 2016 2015 2014 2013 2012 2011 2010 2009 2008 2007 2006 2005 2004 2003 2002 2001 50 Source: IHS Automotive Sales Forecasts © 2014 IHS 15 Ventas globales China vende mas que todos los mercados en desarrollo 50 40 Mature Markets China Others 30 Change 2001-21: MM down 5% China up 1,400% Others up 200% 20 10 2021 2020 2019 2018 2017 2016 2015 2014 2013 2012 2011 2010 2009 2008 2007 2006 2005 2004 2003 2002 2001 0 Source: IHS Automotive, Mature Markets = US, Canada, Japan, S Korea, Australia, NZ, W Europe © 2014 IHS 16 Ciclo promedio por Región Region 2000 2005 2010 2015 2020 Europe 7.0 7.1 6.0 6.3 6.0 Greater China 8.7 7.7 5.8 7.8 7.1 Japan/Korea 3.8 6.0 5.1 7.1 5.2 North America 5.6 5.2 5.5 5.5 4.9 South America 11.3 3.1 8.4 6.9 5.5 • Integración de plataformas globales a NAFTA, China y USA acelera renovación de producto • Promedio global cae debajo de los 6 años en coordinación global • Impacto de la Euro crisis en desarrollo de plataformas Europeas. © 2014 IHS © 2014 IHS 17 Program Cadence 6.8 7.0 Multi-Region Platforms 70% 6.1 6.0 5.2 5.0 4.0 3.0 2.0 1.0 Multi Region Share Weighted Cadence (Years) “Mega” Plataformas 60% 50% After 2015, multiregion (global) platforms approach 70% of volume 40% 30% 0.0 2010 2012 2014 2016 2018 2020 20% 2000 Global Launch Events Launch Event Count 2010 2015 2020 Average Platform Volume (Over 50K/Year) 161 160 2005 140 140 110 106 115 113 120 128 125 2020 115 90 100 73 80 2015 60 40 2010 20 0 2010 © 2014 IHS 2012 2014 2016 2018 2020 0 100,000 200,000 300,000 400,000 500,000 18 Brasil Ventas por concesionario 0 200,000 400,000 600,000 800,000 0 Fiat Fiat Chevrolet Chevrolet Volkswagen Volkswagen Toyota Toyota Ford Ford Nissan Nissan Mitsubishi Mitsubishi Citroen Citroen Renault Renault Peugeot Peugeot LCV 200 300 400 500 # dealers Sales Network Sales 2013 (LCV) LCV Sales per Dealer Sales 2013 Total Total Sales per Dealer Fiat 592 186,708 315 719,225 1,215 Chevrolet 488 142,993 293 594,944 1,219 Volkswagen 449 142,460 317 583,171 1,299 Toyota 143 42,630 298 175,505 1,227 Ford 493 27,413 56 323,258 656 Nissan 159 25,139 158 88,921 559 Mitsubishi 184 21,376 116 55,781 303 Citroen 160 20,497 128 55,480 347 Renault 252 15,566 62 220,972 877 Peugeot 138 5,752 42 46,463 337 Brand © 2014 IHS All light vehicles 100 600 700 Argentina Ventas por concesionario 0 50,000 100,000 150,000 200,000 0 Volkswagen Volkswagen Toyota Toyota Fiat Fiat Renault Renault Chevrolet Chevrolet Peugeot Peugeot Citroen Citroen Ford Ford Mercedes-Benz Mercedes-Benz LCV © 2014 IHS All light vehicles 20 40 60 80 # dealers Brand Sales Network Sales 2013 (LCV) LCV Sales per Dealer Sales 2013 Total Total Sales per Dealer Volkswagen 80 46,432 580 157,572 1970 Toyota 47 27,400 583 53,708 1143 Fiat 77 25,713 334 103,678 1346 Renault 67 23,659 353 139,151 2077 Chevrolet 66 22,825 346 139,771 2118 Peugeot 76 22,640 298 98,183 1292 Citroen 45 21,386 475 40,626 903 Ford 93 21,338 229 117,611 1265 100 Chile Ventas por concesionario 0 10,000 20,000 30,000 40,000 50,000 60,000 70,000 0 Nissan Nissan Mitsubishi Mitsubishi Toyota Toyota Chevrolet Chevrolet Peugeot Peugeot Fiat Fiat VW VW Kia Kia Renault Renault LCV © 2014 IHS All Light Vehicles 20 40 60 # dealers Sales 2013 (LCV) LCV Sales per Dealer Sales 2013 Total Total Sales per Dealer 55 10,549 192 28,858 525 Mitsubishi 64 8,164 128 11,185 175 Toyota 73 8,025 110 26,843 368 Chevrolet n.a. 6,568 n.a. 57,554 n.a. Peugeot 52 5,865 113 12,006 231 Fiat 38 4,277 113 6,506 171 VW 30 3,884 129 8,149 272 Kia 53 3,550 67 32,444 612 Renault 56 501 9 4,768 85 Brand Sales Network Nissan 80 Mexico Ventas por concesionario 0 50,000 100,000 150,000 200,000 250,000 300,000 0 Nissan Nissan Toyota Toyota Volkswagen Volkswagen Ford Ford Chevrolet Chevrolet Mitsubishi Mitsubishi Peugeot Peugeot Renault Renault Fiat Fiat LCV © 2014 IHS All light vehicles 50 100 150 # dealers Brand Sales Network Sales 2013 (LCV) LCV Sales per Dealer Sales 2013 Total Total Sales per Dealer Nissan Toyota Volkswagen Ford Chevrolet Mitsubishi Peugeot Renault Fiat 156 47 166 136 125 55 31 n.a. 50 68,212 24,204 9,854 7,347 6,965 2,807 2,802 1,828 1,592 437 515 59 54 56 51 90 n.a. 32 263,477 60,740 156,313 85,194 193,072 8,997 6,941 21,187 8,228 1689 1292 942 626 1545 164 224 n.a. 165 200 Perú Ventas por concesionario 0 10,000 20,000 30,000 40,000 50,000 0 Toyota Toyota Nissan Nissan Hyundai Hyundai Mitsubishi Mitsubishi Kia Kia Volkswagen Volkswagen LCV © 2014 IHS All Light Vehicles 10 20 30 # dealers Brand Sales Network Sales 2013 (LCV) LCV Sales per Dealer Sales 2013 Total Total Sales per Dealer Toyota 30 16,491 550 38,900 1,297 Nissan 23 3,646 159 11,550 502 Hyundai 14 3,484 249 22,359 1,597 Mitsubishi 37* (incl. Fuso) 2,667 (w/o Fuso) 72 4,042 (w/o Fuso) 109 Kia 16 2,022 126 22,808 1,426 Volkswagen 23 1,840 80 5,719 249 40 Millares Perú Venta de Vehículos Ligeros SAAR 250 Miles de Unidades 200 150 100 50 2007 2008 2009 2010 2011 2012 2013 2014 LV Sales (left scale) © 2014 IHS 24 Perú Ventas Vehículos Ligeros 0.30 Million Units Peru puede sorprender 0.25 0.20 0.15 0.10 0.05 0.00 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019 Current Base © 2014 IHS 25 Perú Market Share 100% 90% Percentage 80% 70% 60% 50% 40% 30% 20% 10% 0% 2008 Jianghuai Mazda Renault/Nissan © 2014 IHS 2010 2012 Chery Mitsubishi Toyota 2014 Ford Volkswagen Hyundai 2016 Honda Suzuki 2018 2020 Fiat General Motors Millones Perú Bodytype Units 0.08 0.07 0.06 0.05 0.04 0.03 0.02 0.01 0.00 2010 © 2014 IHS 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 Perú Hyundai Motor Company, alimentados por carros pequeños 90 80 70 60 50 40 30 20 10 - 70% 100% 60% 90% 50% 80% 40% 70% 30% 60% 20% 50% 10% 40% 0% 30% -10% 20% -20% 10% 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 0% 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 Kia Hyundai YOY A 40 35 30 25 20 15 10 5 0 2010 2011 2012 2013 2014 2016 2017 2018 2019 2020 © 2014 IHS 4 2015 B C D E HVAN Perú Toyota Motor Corporation, Hilux pierde mercado 100% 100% 90% 80% 80% 60% 70% 60 50 40 40% 30 20% 20 60% 50% 40% 0% 30% 10 -20% 20% - -40% 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 Lexus Hino Daihatsu Toyota 10% 0% 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 YOY B C D E HVAN 25 20 15 10 5 0 2010 2016 © 2014 IHS 2011 2017 2012 2018 2013 2019 2014 2020 2015 29 Perú Renault-Nissan Alliance, Tiida desacelera 25 60% 100% 50% 90% 20 40% 80% 30% 70% 20% 60% 15 10% 10 0% -10% 5 -20% - -30% 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 Lada Renault Nissan YOY 50% 40% 30% 20% 10% 0% 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 B C D E 12 10 8 6 4 2 0 Series4 Series8 © 2014 IHS Series6 Series9 Series5 Series10 Series7 Series11 30 Perú General Motors, Sail y Spark van con tendencia negativa 25 140% 100% 120% 90% 20 100% 80% 80% 70% 60% 60% 15 40% 10 20% 0% 5 -20% - -40% 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 Hummer Cadillac Daewoo YOY Chevrolet 50% 40% 30% 20% 10% 0% 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 A B C D E 12 10 8 6 4 2 0 2010 2016 © 2014 IHS 2011 2017 2012 2018 2013 2019 2014 2020 2015 31 Perú Suzuki, estable 100% 100% 90% 80% 80% 60% 70% 12 10 8 40% 6 20% 4 60% 50% 40% 0% 30% 2 -20% 20% - -40% 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 Suzuki Maruti-Suzuki YOY 10% 0% 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 A B C D 8 7 6 5 4 3 2 1 0 2010 2016 © 2014 IHS 2011 2017 2012 2018 2013 2019 2014 2020 2015 32 Perú Volkswagen Group, apuesta a gama de pequeños 12 100% 10 80% 8 - 40% 60% 20% 50% SEAT Audi Porsche 40% 30% -20% 20% -40% 10% 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 Volkswagen 80% 70% 0% 2 90% 60% 6 4 100% 0% YOY 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 A B C D E F HVAN 6 5 4 3 2 1 0 2010 2016 © 2014 IHS 2011 2017 2012 2018 2013 2019 2014 2020 2015 33 Perú Mitsubishi Motor Company, L200 sufre en ventas 120% 100% 100% 90% 7 6 80% 5 60% 4 3 80% 70% 60% 40% 50% 20% 40% 2 0% 30% 1 -20% - -40% 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 Mitsubishi 20% 10% 0% 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 A YOY B C D HVAN 2 2 2 1 1 1 1 1 0 0 0 2010 2016 © 2014 IHS 2011 2017 2012 2018 2013 2019 2014 2020 2015 34 Perú Mazda Motor Corporation, plan agresivo de crecimiento 6 200% 100% 90% 5 150% 80% 70% 4 100% 60% 50% 50% 40% 3 2 30% 1 0% - -50% 20% 10% 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 Mazda 0% 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 B YOY C D 3 2 2 1 1 0 2010 2016 © 2014 IHS 2011 2017 2012 2018 2013 2019 2014 2020 2015 35 Perú Fiat Chrysler Automobiles, fortalecerá gama Fiat 4 80% 70% 60% 50% 40% 30% 20% 10% 0% -10% -20% -30% 4 3 3 2 2 1 1 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 Chrysler Fiat Iveco Jeep Dodge YOY 100% 90% 80% 70% 60% 50% 40% 30% 20% 10% 0% 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 A B C D E F 2 2 2 1 1 1 1 1 0 0 0 2010 2016 © 2014 IHS 2011 2017 2012 2018 2013 2019 2014 2020 2015 36 Perú Honda Motor Company, HR-V será la novedad 100% 100% 90% 80% 80% 60% 70% 6 5 4 40% 3 20% 2 60% 50% 40% 0% 30% 1 -20% 20% - -40% 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 Acura Honda 10% 0% 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 B YOY C D E 4 4 3 3 2 2 1 1 0 2010 2016 © 2014 IHS 2011 2017 2012 2018 2013 2019 2014 2020 2015 37 Perú Bayerische Motoren Werke AG 80% 100% 70% 90% 3 3 60% 2 50% 2 1 1 30% 40% 20% 30% 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 BMW 60% 50% 0% Mini 70% 40% 10% - 80% 20% 10% 0% 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 E YOY D C B 1 1 1 1 1 1 0 0 0 0 0 2010 2016 © 2014 IHS 2011 2017 2012 2018 2013 2019 2014 2020 2015 38 Perú Daimler AG 70% 100% 90% 60% 80% 50% 70% 3 2 2 40% 1 30% 1 - 40% 30% 10% 20% 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 Mercedes-Benz 50% 20% 0% Smart 60% 10% 0% 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 F YOY E D C A 1 1 1 1 1 0 0 0 0 0 2010 2016 © 2014 IHS 2011 2017 2012 2018 2013 2019 2014 2020 2015 39 Mexico Producción Inversiones se aceleran (Millions of units) 5.5 5.0 4.5 4.0 3.5 3.0 2.5 2.0 1.5 1.0 2002 2004 2006 2008 2010 2012 PROD © 2014 IHS 2014 2016 2018 2020 TOTAL VOLUME PLATFORMS BEING PRODUCED NUMBER OF LAUNCHES VOLUME/PLATFORM © 2014 IHS 2010 2,258,727 19 0 2011 2,547,270 19 1 2012 2,865,872 19 2 2013 2,926,860 19 2 2014 3,243,398 22 4 2015 3,360,884 21 0 2016 3,562,545 28 7 2017 4,225,453 27 1 2018 4,492,197 31 7 2019 4,802,667 30 2 2020 4,930,505 29 1 118,880 134,067 150,835 154,045 147,427 160,042 127,234 156,498 144,910 160,089 170,017 41 Sumario • El crecimiento económico global ha desacelerado, precio del crudo puede generar problemas • Industria automotriz apuesta a boom en demanda • China y EEUU empujan a la industria automotriz, pero se espera que resto del mundo retome crecimiento • Velocidad en desarrollo de plataformas incrementara y globalizara • Perú esta a la par con otras naciones de la región en ventas por concesionario • Gama de SUVs crecerá y será mas competitiva • Automotrices apuestan a crecimiento impulsado por producción en Mexico (incluidas las marcas de lujo). • Vamos Perú! © 2014 IHS 42 Thank you! Muchas Gracias! Muito Obrigado! Guido Vildozo Manager, Latin America Vehicle Sales [email protected] For more information, please contact IHS Customer Care 800 447 2273 (IHS CARE) +44 (0) 1344 328 300 [email protected] © 2014 IHS 44

© Copyright 2026