U.S. Corporations and Equity Markets Can Survive the Strong Dollar

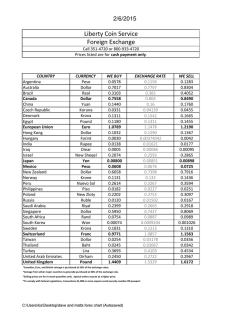

January 28, 2015 Market Update U.S. Corporations and Equity Markets Can Survive the Strong Dollar Rebecca Patterson, Chief Investment Officer • U.S. equity markets fell sharply Tuesday in large part on corporate earnings disappointment, in turn tied to the strong dollar • We expect the dollar to continue appreciating this year; while it is a lingering headwind for multinational U.S. companies, we see four reasons why the dollar will not undermine U.S. equities on a sustained basis: the pace of dollar gains should moderate, corporate hedging programs will become more aggressive, overseas demand should improve and help U.S. earnings, and equity markets will quickly discount this headwind as a consensus view • We remain comfortable with our current equity positioning: overweight equities broadly with a bias towards U.S. large-cap stocks and currency-hedged where possible on nonU.S. equities (particularly euro-denominated) For the last few decades, U.S. Treasury secretaries have shared a mantra: “A strong dollar is in the interest of the U.S. economy.” There is a lot of common sense to the statement, as a strong dollar increases Americans' purchasing power and helps control inflation, which in turn allows the Federal Reserve to keep borrowing costs relatively low. That’s all good for growth. Especially over the last few decades, though, as companies have become more global and have sourced revenues from an increasing number of countries, the “strong dollar” mantra has become more complicated. If a company is not adequately hedged (corporate treasury departments usually try to “neutralize” foreign exchange translation for earnings through hedging programs), weaker foreign currencies can hurt the firm’s revenues when it reports in U.S. dollars. That’s exactly what happened Tuesday. A number of high-profile, large U.S. corporations – ranging from Procter & Gamble to Microsoft to Pfizer - highlighted the damage they incurred from a strong dollar in the latest quarter, with several suggesting more pain could come throughout 2015. Partly in response, the S&P 500 fell more than 1.3% on the day. We expect more of the same this earnings season, for two reasons. First, most corporations hedge using consensus forecasts. For the euro/dollar exchange rate in particular, moves over the last several months were much more dramatic than what the consensus had expected. As a result, we believe that a number of U.S. firms will have found themselves “under-hedged” and with subsequent hits to their quarterly numbers. Second, we believe that many corporate executives use the earnings season as a way to guide investor expectations, with a bias to under-promise and over-deliver. In the current environment, for an executive to say that the dollar could hurt a firm for the year ahead will not make that company stand out as “failing,” since so many multinational firms will likely be in the same boat. Earnings estimates for the S&P 500 for calendar 2015 have fallen 3.3% year-to-date. The energy sector appears responsible for almost 70% of that reduction, though it comes as no surprise that tech and Market Update: U.S. Corporations and Equity Markets Can Survive the Strong Dollar industrials, two internationally exposed sectors, contributed to roughly 20% of the decrease in overall S&P 500 earnings estimates. Looking ahead, we believe the dollar will strengthen further. Despite a 17% gain in the trade-weighted dollar since last June, the currency remains well below longer-term historic averages. Support should come as well from an improving U.S. balance of payments and continued widening in differentials between interest rates in the U.S. and overseas (note the 10-year U.S. Treasury yield today stands just under 1.8% versus 0.37% in Germany and 0.28% in Japan). Additional dollar strength is certainly not good news for large U.S. multinationals. But we believe it will be much less of a headwind in the quarters to come than it is now, for four reasons. 1. Fewer currency surprises. When currency trends are gradual, it is easier for corporations to adjust businesses, broadly as well as currency hedging in particular. Given how far some of the major currencies have fallen already versus the dollar, we see less risk that continued dramatic currency moves continue. As an example, the euro has lost some 18% against the dollar just since last May, more than double the average annual (absolute) change of 8.5% since 1999, the year the euro was launched. As of Jan. 28, the end-2015 consensus EUR/USD forecast was 1.12, with a forecast range of 0.96 to 1.14. Three months earlier, that same end-2015 forecast had been 1.20, with a range of 1.10 to 1.35. For corporations to be truly caught off guard, the euro would need to weaken significantly beyond these new more bearish expectations, and quickly. While possible, it is not our base case. 2 2. Corporations are dynamic. Over the last few decades, as companies have grown more global, their treasury departments have become more sophisticated; in many cases, large U.S. multinationals employ entire teams dedicated to managing currency risk. In general, currency values and positioning are evaluated daily, with changes to hedging programs made regularly. One common approach used by large firms is to hedge the bulk of currency risk (as high as 75% or 100%) for the coming quarter, with less risk hedged the further the company goes out in time. The idea here is that firms can’t know with much conviction what a currency might do over the coming two or three years, but could have at least an educated guess looking at the next quarter or two. After this latest dollar “shock,” it is reasonable to assume that a number of companies have added to hedges to reduce further risk to their USDbased revenues. That means that, as we look forward, the negative currency surprise each quarter should become more muted. 3. Weak foreign currencies are helping demand. Central banks overseas are easing monetary policies and weakening their local currencies to spur growth – so far this month, eight central banks have announced easier policy, with the European Central Bank taking center stage. That’s clearly good news for U.S. companies selling their products or services abroad. While monetary easing feeds through to economic growth with a lag, there are at least some early signs that U.S. firms might see some benefit in the quarters to come. Germany is a good example – exports account for about half the country’s GDP, so a weaker euro is great news for exporters and broader business confidence. Over time, that also feeds through to consumer Market Update: U.S. Corporations and Equity Markets Can Survive the Strong Dollar confidence and spending. Just this week, Germany released its January Ifo business sentiment index, which rose for the third consecutive month. Together with other recent business confidence surveys, the Ifo suggests German GDP rising at just above a 1.5% annualized pace at the start of this year, a nice improvement from growth well under 1% in recent years. 4. Bad news is getting priced in quickly. The selloff in U.S. equities Tuesday was certainly led in large part by dollar-related disappointment. As a rule, markets react to what’s not priced in – they react to surprises. As the strong dollar headwind is increasingly understood and discounted into earnings estimates, it should become less of a market driver. Hiding in smaller-cap U.S. equities with less international exposure, in our view, is not an easy solution given their richer valuations and less liquidity than large-cap peers. While we hold some small- and mid-cap equity exposure, we remain comfortable with our bias towards large-cap U.S. equities along with our (mostly) currency-hedged overseas equity exposure. Investors should not extrapolate from Tuesday’s earnings news and the subsequent market storm. We see calmer weather ahead, helped not just by an improving U.S. economy but by dynamic corporations and markets, as well as growthsupportive monetary policy globally. This material is for your general information. It does not take into account the particular investment objectives, financial situation, or needs of individual clients. This material is based upon information obtained from various sources that Bessemer Trust believes to be reliable, but Bessemer makes no representation or warranty with respect to the accuracy or completeness of such information. Views expressed herein are current only as of the date indicated, and are subject to change without notice. Forecasts may not be realized due to a variety of factors, including changes in economic growth, corporate profitability, geopolitical conditions, and inflation. The mention of a particular security is not intended to represent a stock-specific recommendation, and our view of these holdings may change at any time based on stock price movements, new research conclusions, or changes in risk preference. Atlanta • Boston • Chicago • Dallas • Denver • Greenwich • Houston • Los Angeles • Miami Naples • New York • Palm Beach • San Francisco • Seattle • Washington, D.C. • Wilmington • Woodbridge Cayman Islands • New Zealand • United Kingdom Visit us at www.bessemer.com. Copyright © 2015 Bessemer Trust Company, N.A. All rights reserved.

© Copyright 2026