February Currency Forecast

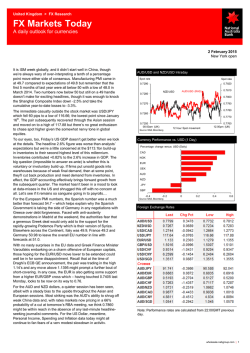

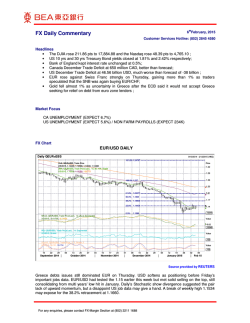

2750 14th Avenue, Suite 306 Markham Ontario, Canada, L3R 0B6 MTFX Section Analytics 6 Email: [email protected] Toll Free: 1.800.832.5104 Fax: 1.866.206.1740 FOREX CURRENCY FORECAST (2015 - 2016) FOREX MAJORS (USD) 2015 2016 SPOT Q1f Q2f Q3f Q4f Q1f Q2f Q3f Q4f Canadian Dollar USD/CAD 1.27 1.30 1.30 1.28 1.28 1.24 1.24 1.22 1.22 Euro EUR/USD 1.13 1.13 1.08 1.08 1.11 1.14 1.17 1.21 1.23 British Pound GBP/USD 1.50 1.51 1.48 1.48 1.53 1.54 1.56 1.58 1.60 Japanese Yen USD/JPY 118 119 122 125 122 117 116 115 114 Swiss Franc USD/CHF 0.92 0.88 0.89 0.90 0.89 0.88 0.86 0.83 0.83 Australian Dollar AUD/USD 0.78 0.77 0.76 0.74 0.76 0.79 0.81 0.83 0.85 New Zealand Dollar NZD/USD 0.72 0.72 0.71 0.73 0.72 0.73 0.72 0.72 0.72 OTHER PAIRS (USD) 2015 2016 SPOT Q1f Q2f Q3f Q4f Q1f Q2f Q3f Q4f Chinese Renminbi CNY/USD 6.25 6.25 6.25 6.20 6.20 6.15 6.15 6.10 6.10 Indian Rupee INR/USD 62.0 61.5 61.5 61.0 61.0 60.5 61.0 60.5 60.5 South African Rand ZAR/USD 11.6 11.5 11.8 12.1 12.0 11.9 11.7 11.7 11.8 Polish Zloty PLN/USD 3.71 3.95 4.15 4.13 4.05 4.05 4.03 4.00 3.95 Kenya Shilling KES/USD 92 91 93 94 95 97 92 90 88 CANADIAN CROSSES 2015 2016 SPOT Q1f Q2f Q3f Q4f Q1f Q2f Q3f Q4f Euro EUR/CAD 1.44 1.41 1.42 1.39 1.41 1.41 1.43 1.46 1.53 British Pound GBP/CAD 1.92 1.89 1.89 1.88 1.90 1.88 1.88 1.90 1.96 Japanese Yen CAD/JPY 100 101 100 104 107 108 108 109 111 Swiss Franc CAD/CHF 0.72 0.68 0.68 0.70 0.70 0.71 0.69 0.68 0.68 Austalian Dollar AUD/CAD 0.99 0.97 0.98 0.96 0.97 0.99 1.00 1.01 1.05 New Zealand Dollar NZD/CAD 0.93 0.94 0.92 0.93 0.92 0.91 0.89 0.88 0.88 Chinese Renminbi CNY/CAD 4.91 4.81 4.81 4.84 4.84 4.96 4.96 5.00 5.00 Indian Rupee INR/CAD 48.8 47.3 47.2 47.7 47.7 49.1 49.1 49.6 49.6 South African Rand ZAR/CAD 9.15 8.85 9.10 9.45 9.40 9.60 9.45 9.60 9.70 Polish Zloty PLN/CAD 2.92 3.05 3.20 3.25 3.15 3.30 3.25 3.30 3.25 Kenya Shilling KES/CAD 72 70 72 73 74 78 74 74 72 1.800.832.5104 [email protected] 2750 14th Avenue, Suite 306 Markham Ontario, Canada, L3R 0B6 Email: [email protected] Toll Free: 1.800.832.5104 Fax: 1.866.206.1740 MTFX Section Analytics 6 FEBRUARY 2015 - CURRENCY HIGHLIGHTS USD The US dollar continues to remain the darling currency of 2015. The collapse in oil prices is a win as America is still a net importer of oil. The collapse in oil means cheaper goods and more disposable income allowing domestic growth to accelerate. The US will continue to gain momentum in 2015 and we are more than happy to jump on the bandwagon. CAD The Bank of Canada surprised the markets last month with a rate cut of 25-bp, we’re expecting another 25-bp cut which seems to have already been priced in by the markets. A weaker Canadian growth profile compared to the US, a more pronounced rate spread between the Fed and the BoC, and the nosedive in oil will effectively crush the loonie in the coming months. EUR Draghi finally came through last month with some much needed QE. The proposed QE plan was twice as large what the street was expecting and has sent the Euro into a nosedive. The Euro’s slide is by no means over with the market looking for a test of 1.07. Though some analysts are calling for a 1:1 euro-dollar, we find parity to be unlikely. GBP The fate of the pound will be driven by politics rather than economic fundamentals in the medium term. With elections scheduled for May 7th neither of the two main parties seem capable of winning a majority leaving the market worried about an unstable government. However, the growth profile for the UK remains strong with the pound expected to rebound in Q3. 1.800.832.5104 [email protected] 2750 14th Avenue, Suite 306 Markham Ontario, Canada, L3R 0B6 MTFX Section Analytics 6 Email: [email protected] Toll Free: 1.800.832.5104 Fax: 1.866.206.1740 FEBRUARY 2015 - CURRENCY HIGHLIGHTS February 2015 2015f Spot USD/CAD MTFX Consensus Forecast EUR/USD 1.27 MTFX Consensus Forecast GBP/USD Consensus Forecast 1.13 MTFX 1.50 2016f Q1f Q2f Q3f Q4f Q1f Q2f Q3f Q4f 1.30 1.30 1.28 1.28 1.24 1.24 1.22 1.22 1.30 1.30 1.30 1.28 1.25 1.23 1.22 1.24 1.13 1.08 1.08 1.11 1.14 1.17 1.21 1.23 1.12 1.09 1.07 1.10 1.13 1.13 1.14 1.15 1.51 1.48 1.48 1.53 1.54 1.56 1.58 1.60 1.50 1.45 1.45 1.49 1.51 1.53 1.56 1.58 U.S. DOLLAR COMMENT: The US dollar remains the king of 2015 and investors continue to increase holdings in the USD as a result of strong economic fundamentals. The US economy seems to be gaining momentum with growth continuing to accelerate. Consumer confidence is strong and is likely to continue to improve aided by the drop in oil and gasoline prices. Unemployment is at multi-year lows and macro-economic data suggests that the US economy is poised to expand with a ramp up in industrial production, rising capacity utilization and housing starts. The collapse of oil prices is sending chills through many developed and emerging markets but for the US cheap oil is a win. The collapse in oil means cheaper goods and more disposable income allowing domestic demand and growth to accelerate. In this environment the USD is expected to appreciate against the majors with support from both fundamentals and flows. Declining oil prices will likely act as a positive catalyst for the USD in the near term. Strong fundamental economic data has reinforced the view that the Fed will begin to raise interest rates in Q2 2015. Recent comments from the Fed have reinforced this bullish view which has resulted in a significantly stronger greenback against most of the majors. The only credible risk to the bullish sentiment of the Fed could be a soft global growth profile stemming from Asia and Europe. Overall the USD remains the currency of choice in 2015 and is well positioned for further upward momentum against its peers. JANUARY CURRENCY RETURNS 0% -2% CAD EUR GBP -4% -6% -8% -10% -12% -14% -16% -18% EVENTS TO WATCH IN COMING MONTH ECONOMIC EVENT DATE USD ISM Manufacturing PMI FEB 02 USD ADP Nonfarm Payrolls FEB 04 USD Unemployment Rate FEB 06 USD Non Farm Payrolls FEB 06 USD Core Retail Sales FEB 12 2015 seems to be the year of the US dollar. 1.800.832.5104 [email protected] 2750 14th Avenue, Suite 306 Markham Ontario, Canada, L3R 0B6 MTFX Section Analytics 6 Email: [email protected] Toll Free: 1.800.832.5104 Fax: 1.866.206.1740 USD/CAD FEBRUARY 2015 HIGHLIGHTS February 2015 2015f USD/CAD Spot MTFX Forecast Consensus Forecast 1.27 2016f Q1f Q2f Q3f Q4f Q1f Q2f Q3f Q4f 1.30 1.30 1.28 1.28 1.24 1.24 1.22 1.22 1.30 1.30 1.30 1.28 1.25 1.23 1.22 1.24 USD/CAD CURRENCY TREND HIGHLIGHTS: The bank of Canada surprised the markets last month with a 25-bp cut, and we’re expecting another 25-bp cut in March given the collapse in oil. The second rate cut seems to be priced in to the loonie given the spectacular collapse in the month of January. 1.29 1.27 1.25 1.23 1.21 A weaker Canadian growth profile compared to the US, a more pronounced rate spread between the Fed and the BoC, and the nosedive in oil and other commodities will provide a potent mix to effectively crush the loonie in the coming months. 1.19 1.17 1.15 EVENTS TO WATCH IN COMING MONTH ECONOMIC EVENT DATE CAD Ivey PMI FEB 04 CAD Trade Balance FEB 05 CAD Building Permits FEB 06 CAD Employment Data FEB 06 CAD Retail Sales FEB 20 The weaker loonie should help exports and a recovery in oil prices could suggest a firmer loonie. However, the need to have exports become driving force of our economy and take the lead from housing and debt-driven growth seems a stretch. Expect 1.20 -1.25 loonie in the longer term. MARKET SENTIMENT: Bearish Bullish 1.800.832.5104 [email protected] 2750 14th Avenue, Suite 306 Markham Ontario, Canada, L3R 0B6 MTFX Section Analytics 6 Email: [email protected] Toll Free: 1.800.832.5104 Fax: 1.866.206.1740 EUR/USD FEBRUARY 2015 HIGHLIGHTS February 2015 2015f EUR/USD Spot MTFX Forecast Consensus Forecast 1.13 2016f Q1f Q2f Q3f Q4f Q1f Q2f Q3f Q4f 1.13 1.08 1.08 1.11 1.14 1.17 1.21 1.23 1.12 1.09 1.07 1.10 1.13 1.13 1.14 1.15 EUR/USD CURRENCY TREND HIGHLIGHTS: Draghi and the ECB finally delivered QE to the Eurozone with the purchase of 60 billion euros per month through to September 2016. The ECB committed to a plan that was twice what the street was expecting resulting in the collapse of the Euro to multi- year lows. 1.22 1.2 1.18 1.16 The Euro lost 12% in 2014 and should continue its slide as the ECB rolls out its QE program. The lower exchange rate and lower financing costs should boost economic growth in the region and significantly improve economic fundamentals. 1.14 1.12 1.1 EVENTS TO WATCH IN COMING MONTH ECONOMIC EVENT DATE EUR German Manufacturing PMI FEB 02 EUR Retail Sales FEB 04 EUR German GDP FEB 13 EUR German Economic Sentiment FEB 17 USD German Manufacturing PMI FEB 20 The Euro’s slide is by no means over with the markets eyeing the 2003 lows of 1.08. Though some analysts have talked about a 1:1 euro-dollar, parity it seems unlikely given that economic fundamentals and a current account surplus should being to improve and stabilize the currency. MARKET SENTIMENT: Bearish Bullish 1.800.832.5104 [email protected] 2750 14th Avenue, Suite 306 Markham Ontario, Canada, L3R 0B6 MTFX Section Analytics 6 Email: [email protected] Toll Free: 1.800.832.5104 Fax: 1.866.206.1740 GBP/USD FEBRUARY 2015 HIGHLIGHTS February 2015 2015f GBP/USD Spot MTFX Forecast Consensus Forecast 1.50 2016f Q1f Q2f Q3f Q4f Q1f Q2f Q3f Q4f 1.51 1.48 1.48 1.53 1.54 1.56 1.58 1.60 1.50 1.45 1.45 1.49 1.51 1.53 1.56 1.58 GBP/USD CURRENCY TREND HIGHLIGHTS: While we agree with most analysts that there is a very small chance that the BoE will be raising rates before Q3-2015, our call is that the markets are over-dovish on the pound. Similar to 2014 the pound has the potential to surprise in the second half of 2015. 1.57 1.56 1.55 1.54 1.53 Economic fundamentals in the UK are strong compared to its peers, however, in the near term the pound will largely be driven by politics with the UK parliamentary elections scheduled for May7th. Neither of the two main parties seem capable of winning a majority leaving the market worried about an unstable government. 1.52 1.51 1.5 1.49 EVENTS TO WATCH IN COMING MONTH ECONOMIC EVENT DATE GBP Manufacturing/Services PMI FEB 2/4 GBP BoE Interest Rate Decision FEB 05 GBP Consumer Price Inflation FEB 17 GBP Employment Data FEB 18 GBP Retail Sales FEB 20 We expect politics to weigh on the GBP in the first half of the year, however, given the strong economic fundamentals we expect the UK outperform most of its peers in Q3/Q4 of 2015 giving a significant boost to the pound. MARKET SENTIMENT: Bearish Bullish 1.800.832.5104 [email protected] 2750 14th Avenue, Suite 306 Markham Ontario, Canada, L3R 0B6 Email: [email protected] Toll Free: 1.800.832.5104 Fax: 1.866.206.1740 MTFX Section Analytics 6 FOREIGN EXCHANGE DISCLAIMER This publication has been prepared by MTFX Inc. for informational and marketing purposes only. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinionscontained herein have been compiled or arrived at from sources believed reliable, but no representation or warranty, express or implied, is made as to their accuracy or completeness and neither the information nor the forecast shall be taken as a representation for which MTFX Inc., its affiliates or any of their employees incur any responsibility. Neither MTFX Inc. nor its affiliates accept any liability whatsoever for any loss arising from any use of this information. MTFX Analytics 2750 14th Avenue, Suite 306 Markham, Ontario Canada L3T 6X1 Toll Free: 1.800.832.5104 Fax: 1.866.832.5104 Email: [email protected] This report has been prepared by MTFX Inc. as a resource for its clients. The opinions, projections and estimates contained herein are our own and subject to change without notice. 1.800.832.5104 [email protected]

© Copyright 2026