Emerging Markets Debt Indicator - Amazon Web Services

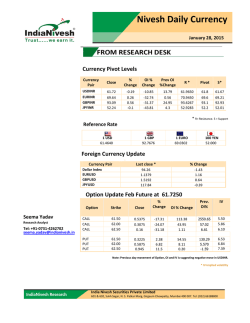

Indicator Emerging Market Fixed Income Emerging Markets Debt October 2014 Views expressed as at 10 October 2014. All returns below in US dollars unless otherwise stated. At a glance • The JP Morgan GBI-EM Global Diversified Index fell 5.11%. Bonds were down 1.02%, while currencies fell by 4.09%. • US economic data remained relatively strong, prompting a more hawkish statement from the Federal Reserve which supported a strong dollar and led to higher US Treasury yields, with a knock-on impact for emerging market debt. • Topic of the Month: What does US Dollar strength mean for emerging markets? Recent developments It proved a challenging month for emerging market debt, especially when measured against the US dollar. With US economic data remaining relatively strong, the Federal Reserve (Fed) tweaked its forward guidance. While maintaining that near-zero interest rates will remain in place for some time yet, they have indicated that when rates do start rising, they will do so at a quicker pace than previously communicated. As a result US Treasury yields have trended higher with some knock-on impact for emerging markets. Chinese data deteriorated somewhat with industrial production growth hitting a six-year low, while demand for loans moderated significantly in the third quarter. There was also a sharp rise in non-performing loans during the first half of the year. This prompted the Chinese authorities to inject US$81 billion into the country’s banking system, although it was noteworthy that policymakers appear to have become more accepting of the country failing to meet its 7.5% growth target. Protests in Hong Kong took centre stage towards the end of the month, something which will be closely monitored as developments unfold. Elsewhere in Asia, dataflow was mixed, with purchasing managers' indices (PMIs) generally moderating over the month, although as a region, Asia still looks in decent shape compared to other regions. Latin American macroeconomic data showed some modest signs of improvement with industrial production modestly exceeding expectations in Mexico and Brazil. The effects of the sanctions against Russia have been felt in eastern and central Europe, most notably in Poland with PMI and industrial production turning significantly weaker. Local currency bonds, as measured by the JP Morgan GBI-EM Global Diversified Index fell 5.11% over September. Bonds were down 1.02%, while currencies fell 4.09%. The Brazilian real was the worst performing currency as sentiment weakened given the uncertainty surrounding the presidential election and the S&P’s outlook downgrade. The Russian ruble fell to new lows versus the US dollar as further sanctions loom on the horizon and oil prices sliding well below $100 a barrel. By contrast, the Nigerian naira was the best performer following intervention by the central bank to prop up the local currency. The Chilean peso and Peruvian new sol also performed relatively well. Hard currency bonds, as measured by the JP Morgan EMBI Global Diversified Index, fell by 1.81%. The index yield ended somewhat higher at 5.40% while spreads over US Treasuries rose to 299 basis points. The best performing hard currency bond market was Argentina, followed by Ghana and Honduras. By contrast, the worst performers were Venezuela, Uruguay and Ecuador. Corporate bonds, as measured by the JP Morgan CEMBI Broad Diversified Index, fell 0.86% with spreads rising slightly to 298 basis points. Investment grade bonds (-0.78%) outperformed high yield bonds (-1.02%). The top performing sector was financials, with real estate and transport also holding up relatively well. Metals & mining was the weakest sector, while TMT and oil & gas were also particularly weak. Regionally, central and eastern Europe held up reasonably well, while Latin America was the weakest by some margin. This communication is only for professional investors and professional financial advisors. It is not to be distributed to the public or within a country where such distribution would be contrary to applicable law or regulations. Outlook and strategy The global growth outlook remains mixed. In developed markets, we continue to witness divergent fortunes; while the US continues with its impressive recovery, Europe and Japan look decidedly shaky. We expect this theme to broadly continue over the coming months, and consequently the impact on individual emerging markets will be varied. Chinese data flow has turned weaker again, focused mainly in the manufacturing and property sectors, but the services sector should help to offset some of this weakness, meaning growth should stay between 7 and 7.5% this year. Markets have become more concerned about the pace of Fed tightening, with forward guidance now indicating interest rates are set to rise at a faster pace than previously communicated, helping to explain the accelerated pace of US dollar appreciation. While we expect Treasury yields to rise, we expect this process to be gradual, rather than for a sharp correction. The negative impact of Fed tightening on global liquidity conditions should be partially offset by the European Central Bank’s easing cycle and there is also an increasing possibility of the Bank of Japan undertaking fresh monetary stimulus. Portfolio flows into emerging market debt were modestly stronger in September. We still feel positioning is relatively light and with comparatively attractive yields on offer we expect flows to remain generally supportive. On a more structural view, we believe global investors, particularly US institutional investors, remain structurally under-allocated to emerging markets which will provide a tailwind for flows over the medium term. Emerging market inflation has fallen from its June peak and the outlook remains relatively benign as food and oil prices continue to moderate. This should help to mitigate the impact of pass-through from the stronger US dollar. Overall, we believe global growth patterns, positioning within the economic cycle and the external financing requirements of individual emerging market economies will remain significant determinants of individual market performance. Political developments will also be important to watch. In particular, the second round of the Brazilian presidential election will be on our radar, following the surprisingly strong performance of opposition candidate Aécio Neves in the first round. Topic of the month: What does US Dollar strength mean for emerging markets? Introduction After a summer of trendless markets and exceptionally low volatility, the autumn has started with one very clear and strong theme: a stronger US dollar (USD). Historically, such trends in the US dollar have tended to create significant headwinds across emerging market economies and assets. However, in this post global financial crisis world, we believe that care must be taken in drawing lessons from historical periods of US dollar strength. The rate hiking cycle in the US may look quite different this time from previous episodes. Other large developed economies such as Europe and Japan may be easing as the US tightens, providing some offsetting effects. And most importantly, many emerging markets have transformed themselves in a number of important ways over the last 15 years since the US dollar last rallied, making themselves significantly less vulnerable this time around. Why is the USD strong again? Market expectations at the start of the year were for a further rise in the long end of the US yield curve, with the 10year yield expected to push well above 3%. Instead, a pothole in US GDP growth in the first quarter, combined with strong technical demand and risk aversion to the Russia-Ukraine crisis, pushed the US yield curve lower. The US dollar was quite weak, in particular versus emerging market currencies, and trading volumes across many assets fell as volatility diminished. The markets became complacent. A strong rebound in growth in the second quarter and continued improvements in the labour market meant that by late August, focus turned to the fact that market expectations of US interest rates were anticipating slower hikes than the Federal Reserve’s (Fed’s) own projections. As a result, short-term US interest rates started to move up, and this trend accelerated when the Fed revised its own estimates up quite sharply at their mid-September meeting, as shown in Chart 1. The changing differential between short-term US interest rates and those elsewhere is a key driver of developed and emerging market currency movements, as well as US dollar denominated commodities. 2 Chart 1: Market pricing vs Fed expected pace of rate hikes on day of September 2014 FOMC 5 4 3 2 1 0 2014 2015 2016 2017 Longer Term Sep 2014 Median 0.125 1.375 2.875 3.75 3.75 Jun 2014 Median 0.25 1.125 2.5 Fed Funds Futures 0.099 0.819 1.854 Minutes Sep 2014 Sep 2014 Median Jun 2014 Median 3.75 2.527 Fed Funds Futures Source: Investec Asset Management; FRB; Bloomberg We believe it is important to differentiate between this current period of US dollar strength and the events of mid-2013. At that time, longer-term US interest rates had moved to very low levels, such that the ‘term premium’ (the excess yield on long-term vs short-term bonds) investors usually demand for the risk of holding longer-term bonds had turned negative; see Chart 2. The subsequent rebound in the ‘term premium’ caused the so-called ‘taper tantrum’ which hurt emerging markets which are more sensitive to longer term US interest rates. Today the ‘term premium’ is at more reasonable levels, suggesting less risk for emerging markets. Chart 2: US term premium (%) – measure of long-term interest rate uncertainty 2.5 5yr estimated term premium 2 1.5 TAPER 1 0.5 0 QE -0.5 -1 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 Source: Investec Asset Management; FRBNY 3 This is broad USD strength, not just against EM Currencies In fact, developed market currencies and commodities tend to be more sensitive to short-term US interest rate moves. The dollar index against G10 currencies (DXY) rose 8.6% in the third quarter, whilst Brent crude has fallen 22% in USD terms over the same period. Chart 3 shows the performance of the JP Morgan emerging market currencies index (EMFX) in Euro and Yen terms, where emerging markets have posted gains over the last few months. Consequently, the risk of material outflows appears lower as many investors have not suffered losses. Further aggressive monetary policy easing from both the European Central Bank and the Bank of Japan appear quite possible in the first half of 2015. This will not only ensure that outflow pressures remain limited from investors based in these currencies, but more fundamentally means that liquidity from these central banks may partially replace the gradual withdrawal of US dollar funding which has been ample for emerging markets over the last decade. Chart 3: JP Morgan EMFX index vs major developed market FX 110 in USD in EUR in JPY 105 100 95 90 85 80 Jan 2013 Mar 2013 May 2013 Jul 2013 Sep 2013 Nov 2013 Jan 2014 Mar 2014 May 2014 Jul 2014 Sep 2014 Source: Investec Asset Management; Bloomberg Importantly, the decline in many commodity prices has outstripped the fall in EMFX. Chart 4 shows Brent crude oil priced in selected emerging market currencies – the prices faced by domestic consumers. Unlike in 2013, the price is falling across all emerging markets, helping to lower inflation and deliver relative stability in local currency bonds. In countries such as Turkey where further currency depreciation is needed to adjust still-large current account deficits, the central bank can allow this without risking spiralling domestic prices. Of course, declining commodity prices are not good news for all emerging markets, and may weigh on some markets such as Nigeria and Chile. Chart 4: Brent crude denominated in selected emerging market currencies 130 in KRW in TRY in INR Jul 2014 Sep 2014 120 110 100 90 80 70 Jan 2013 Mar 2013 May 2013 Jul 2013 Source: Investec Asset Management; Bloomberg 4 Sep 2013 Nov 2013 Jan 2014 Mar 2014 May 2014 Big picture: this is different from the USD cycles in the 1980s and 1990s Some commentators have drawn parallels between the events of recent weeks and the start of the multi-year USD bull markets of the early 1980s and late 1990s, when the US again was largely the world’s only growth engine. There are reasons to believe that coming quarters may not see such a strong US dollar cycle, and certainly not with the same broad negative implications for emerging markets: 1. Many economists now estimate long-term potential US GDP growth rates at less than 2%, an assessment we would certainly share. In the early 1980s and late 1990s structural reforms and the technology revolution pushed potential US GDP growth above 3%. This meant the Fed had to raise policy rates much higher than it will do this time around. 2. The US basic balance of payments (current account plus long-term FDI) was in a small surplus at the start of the historic USD rallies. Whilst it has improved in recent years thanks to domestic energy production in the US, it remains in a modest deficit, creating some further headwinds. 3. Since the 1997 Asian financial crisis, most emerging markets have decreased the proportion of debt issuance denominated in US dollars and so there has been a drastic improvement in the net USD debt position of all but a few countries. The exposures to a stronger USD which triggered the string of EM crises in the 1980s and 1990s have been reduced to levels where they are well covered by foreign currency reserves in all but a handful of emerging markets. While sovereign debt is covered by such reserves, we acknowledge that there has been a significant increase in corporate USD debt exposure in the last three years. 4. Many emerging markets have made huge strides to reduce inflation to very manageable levels and create policy anchors which anchor inflation expectations. This means currencies can move more freely to adjust to the domestic economy without requiring drastic monetary policy interventions. Conclusion: More differentiation within emerging markets from this USD rally Instead, we feel that the current environment of modest USD strength, combined with sluggish Chinese growth and resulting lower commodity prices, creates opportunities for investing in strong relative themes across emerging markets. Terms of trade may continue to diverge, which will help drive currency movements. In particular, those emerging markets geared towards exporting to the US will likely to see robust demand, while declining energy prices will prove a positive trend for importers. Whilst economies with greater external funding requirements should still feel depreciation pressures from further adjustments in short-term US interest rates, we will also have to be alive to any increased probability of monetary stimulus from Europe or Japan which could drive renewed performance in current account deficit countries. Credible inflation anchors provide a further source of differentiation – many emerging markets have seen stable bond markets and continued easing biases from central banks despite rising US interest rates. Those countries which more credible inflation anchors can continue to deliver positive local bond returns in spite of the global environment. Most significantly, an environment of modestly stronger USD places an additional premium on countries delivering productivity growth and structural reforms. Countries which can deliver higher productivity will enhance their inflation anchors through improved supply side dynamics, along with better fiscal fundamentals, further differentiating local bond and credit returns. Their real effective exchange rates will also continue to appreciate on a long-term basis. Most interestingly, several emerging markets including India, Vietnam and the Philippines are moving further in this direction. The upcoming election results in Brazil may add another important name to the reform list. 5 Selected emerging markets at a glance Central and eastern Europe Czech Republic Inflation ticked higher in September to 0.7% year-on-year but was lower than expected and slightly below the central bank’s forecast. Activity data remains strong while higher consumer spending is being driven by the improving situation in the labour market and a favourable fiscal policy. We remain underweight in koruna rates and neutral in foreign and hard currency debt. Poland The central bank cut the reference rate by 50bps to 2%, in a more aggressive move than anticipated. In the press release, the central bank emphasised a further deceleration in economic growth during the third quarter as well as continued subdued inflation. We remain underweight in foreign currency, and market weight in local and hard currency bonds. Romania In line with our expectations the central bank cut its main policy rate by 25bps to 3%, and further reduced reserve requirements on new leu-denominated liabilities. In its statement, the central bank emphasised lower-than-expected inflation on the back of declining agricultural prices, subdued euro area inflation, a negative output gap and lower inflation expectations. We remain overweight in local bonds and market weight in foreign and hard currency debt. Hungary Hungary’s economy is clearly picking up with growth expected to exceed 3% year-on-year in 2014. Public spending, manufacturing and EU fund absorption are the main factors behind the sharp acceleration in investment. Despite the strong momentum, it will be challenging for the Hungarian economy to maintain this rate of growth in 2015 amid a slowdown of investment and headwinds for external demand. We are neutral in local and foreign currency debt, while we moved to an overweight position in Hungarian hard currency debt. Latin America Brazil Brazilian markets are very volatile and are primarily being driven by the unfolding political drama around the presidential election. Dilma Rousseff won the first round, as predicted by the polls, but the sharp fall-off in support for Maria Silva and Aecio Neves’ subsequent progression to the run off against Rousseff took the markets completely by surprise. After a huge sell off in both the currency and the bond markets as Dilma’s poll ratings steadily improved, Neves’ strong showing has swung the pendulum back towards a reasonable probability of a more market friendly administration and pushed markets sharply higher. Against this backdrop, the challenges for the next president, whoever it is, are huge and rising. The drought continues and inflation is creeping steadily higher again. Despite the challenges, we continue to see value in the high local yields given the very poor growth outlook, and have used the recent sharp back up in yields to increase our overweight. We maintain a small overweight in the hard currency bonds, generally preferring other regional credits such as Peru. We also used the recent weakness in the Real to move back to marketweight, as valuations moved more towards fair value. Chile Growth continues to be weak, although recent numbers have started to improve at the margin. Against this backdrop, the central bank has remained dovish, cutting rates from 3.50% to 3.25% at its last meeting, with mixed indications that there is a little more to come. We believe that with their still relatively upbeat growth forecasts for next year, which are in line with our own, and still uncomfortably high inflation, the window to ease further has now almost closed. We continue to hold our overweight peso position, as we believe it continues to present good value relative to copper and that growth has bottomed. We also believe that the authorities are unlikely to have appetite for much more currency weakness. Given this view and a somewhat more cautious view on inflation, we remain neutral local bonds, but stay overweight in hard currency, which continues to look attractive relative to other regional investment grade credits. 6 Venezuela We have continued to hold our overweight position in hard currency bonds relative to an Argentine underweight. The performance of this credit has been a rollercoaster ride, despite the recent positive news that PDVSA will be able to sell some USD at the weaker SICAD 1 and 2 rates, rather than at the official rate. We continue to expect to see these modest responses from Nicolas Maduro’s government to the crisis. This, combined with our view that Venezuela has the ability and the willingness to pay and service its debt over the medium term, keeps us constructive given the extremely cheap valuations. We are, however, cogniscant that the debt and interest payments due in October are likely to keep spreads under pressure until they are out of the way. Argentina Argentina continues to make unorthodox moves, tightening control where it can and putting the economy under increasing pressure. Recent growth and inflation numbers have all printed better than expected, but once again we are becoming increasingly sceptical of the reliability of this data. While Cristina Kirchner’s response to the U.S. Supreme Court’s contempt of court ruling and a second coupon failing to reach restructured holders have done little to close the growing rift between the government and the holdouts, it was the resignation of the central bank governor and his replacement with a more pliable candidate that finally caused spreads to widen. We continue to believe that the market is overpriced given the economic risks and the increasing probability that any resolution of the current default is likely to extend into 2016 and a new administration. We therefore maintain our underweight position relative to Venezuela. Colombia Economic activity slowed at the margin but remains on track to be the regional outperformer this year, with adjustments by market players concentrating more on the extent of the positive output gap than a marked deceleration. However, the central bank left rates on hold and also halved dollar purchases to US$1bn, suggesting comfort with current levels of the peso. We allowed dilution of our overweight in local bonds into the final instalment of index rebalancing. We also took profits on our underweight position in the peso relative to the Mexican peso during the recent bout of currency weakness. We remain comfortable with our overweight in hard currency on improving underlying fundamentals. Mexico Forward looking indicators continued firming while continued rise in consumer confidence suggests prospects of the recovery are already boding well for what has been anaemic domestic demand. Despite closing our long position in the currency relative to the Colombia peso we remain constructive and expect it to be a long-term outperformer in the region. Inflation is set to remain at the top of the band and combined with the impending normalisation of rates in the US and deteriorating fiscal metrics, we continue to favour an underweight in local bonds. We hold our underweight in hard currency as we see spreads largely pricing the strong fundamentals. Panama Reports of inflated government revenues and understated fiscal deficits for the first half of the year were confirmed by the new administration as they sought to widen the ceiling of the fiscal rule. While the overiding expectation is for President Varela to be more successful in reigning in spending than his predecessor, a still expansionary stance targeting infrastructure and a less glossy starting point suggest that convergence is likely to be gradual. We remain underweight dollar bonds. Peru Political noise has been on the rise in the lead up to gubernatorial elections, which comes after yet another cabinet reshuffle that narrowly passed a confidence vote and a series of corruption scandals that have hampered the execution of previously announced fiscal measures. We closed our overweight in the sol relative to the Brazilian real to lock in some profits on the cross. We remain underweight local bonds which underperformed the benchmark after significant selling by offshore investors. We continue to hold an overweight in hard currency bonds reflecting the strong relative debt dynamics in the region. 7 Middle East, Commonwealth of Independent States (CIS) and South Africa Georgia Georgian CPI moved higher to just below the central bank target of 5% while second-quarter GDP softened to 5.2%. We continue to expect a gradual moderation into year end and then a pick-up next year. Georgia Rail’s first-half results showed a widening in EBITDA margins, despite a drop off in oil volumes. We are neutral Georgia’s dollar bonds through a holding in Georgia Rail. Israel Low inflation and weak growth added impetus to the central bank’s desire for a weaker shekel, which sold off a further 3% over the month. Even so, this is unlikely to be enough to prevent a negative inflation reading in September. The central bank kept rates at 0.25% but the minutes of the MPC meeting were dovish. We remain neutral the Israeli shekel. Kazakhstan The new Kazakh 10-year and 30-year dollar bonds attracted huge investors interest and cleared 25 and 30 basis points lower than initial market guidance. We opted to stay on the sideline believing that it would cause a revaluation of our overweight position held through quasi sovereign bonds, which it did. There is little appetite from the central bank for another tenge devaluation but the currency’s appreciation against the Russian ruble is increasing the risk to our overweight. Russia The Russian economy continues to struggle under the heavy weight of sanctions and geopolitical risks which are causing significant capital outflows. The central bank has chosen to remain focused on its inflation-targeting framework and thus did not substantially increase interventions in the foreign exchange market. As such, the ruble continued to sell-off, heightening the risk to inflation itself, but somewhat mitigating the negative budgetary effects of a lower oil price. We remain neutral all Russian assets (hard currency bonds, local bonds and the ruble) but are underweight the quasi-sovereign bonds. South Africa On balance, the last month’s data has been poor again, with widening trade and budget deficits. Overall PMI did improve slightly, although new orders did note, and the economy is still heading for c.1.5% GDP growth this year. The prospective central bank governor, Lesetja Kganyago, is a good choice and points to policy continuity. We believe the current profile of market rate hike expectations to be too aggressive and added shorter-dated bonds. We continue to hold an underweight position in the rand (versus the Turkish lira) and an underweight exposure to South Africa’s dollar bonds. Turkey Despite confirmation of weak second-quarter growth of -0.5% quarter-on-quarter, the high frequency numbers have since ticked up somewhat. The central bank remains between a rock and a hard place, with a need to keep rates on hold at 8.25% due to political risks weighing on the lira. There was some relief with inflation surprising to the downside as it fell to 8.9% during September. Syria, and specifically the northern town of Kobane, has become a complicated issue for the government worried about a unilateral Turkish attack on IS eliciting a violent retribution. The dithering has in turn incited protest from its Kurdish population. We built an overweight in the front end of the yield curve, believing that central bank will be hard-pressed to hike rates amid such a weak growth environment, with base-effects supporting disinflation at least until the second quarter of 2015. We continue to hold our overweight position in the lira against the rand. Ukraine The ceasefire in eastern Ukraine remains fragile – some would argue it is non-existent in Donetsk, where there is continued fighting for control of the airport. While rebels push for more independence for the region there are continued efforts for a diplomatic solution at a higher level. The drop-off in economic output has been meaningful and deposit withdrawals from the banking sector remain high. The central bank has enforced further measures to support the weakening currency. Despite disruptions in the east, tax collections have been relatively strong. We are neutral Ukraine’s dollar bonds and hold a small overweight in the hyrvnia. 8 Africa ex South Africa Egypt Egypt posted real GDP growth of 2.1% for fiscal year ended 30 June 2014. Rapid growth in manufacturing, transportation and communication sectors was dragged down by continued contraction in the energy sector. High frequency indicators point to an acceleration in real growth during the summer as industrial production improved to a two-year high while August tourist arrivals posted their strongest figures since the 2011 revolution. On the balance of payments side, Egypt’s situation is slightly more precarious as financing of a deteriorating current account deficit has become almost wholly dependent on private and GCC transfers. Kenya In line with several other African economies, Kenya announced a revision to its GDP estimates resulting in a 25% increase in GDP to US$55bn. Increased coverage was given to growing industries such as mobile money and informal businesses. Stronger GDP growth was also met with a decline in inflation to 6.6% (from 8.1%) on the back of lower fuel and food prices. Although recent news has been positive, we remain underweight the Kenyan Shilling relative to the Ugandan Shilling as excess liquidity resulting from increased fiscal expenditure and the reluctance of the central bank to raise rates should keep the Kenyan shilling under pressure. Ghana During the month, Ghana issued a US$1bn Eurobond clearing at a yield of 8.25%. The Eurobond provides temporary respite with the real test being the commitment of government to follow through with a possible IMF program. Meetings between the IMF, World Bank and Ghana will be completed during the first half of October. We took profit on our overweight cedi position following a 15% rally in the currency as we expect seasonal currency pressures to reassert themselves during the latter part of the year, while IMF execution risks remain high. Nigeria With elections looming early in 2015 the People’s Democratic Party moved to assert themselves as favourites by confirming President Goodluck Johnathon as their only candidate for elections, while the opposition All Progressives Congress party is yet to announce presidential candidates. This made it the first time since Nigeria’s return to democracy that the PDP presidential candidate won’t have to contest in the primaries. On the economic side, GDP growth was relatively robust at 6.5%, driven by manufacturing growth, but risks remain to the downside following recent oil price weakness. The central bank decided to leave rates on hold, but have taken an increasingly hawkish tone given recent naira volatility. We closed our naira overweight during the latter part of the month as lower oil prices, below target oil production and the possibility of increased political noise as we move closer to elections have balanced risks to the downside. Uganda Ugandan inflation eased further during the month with core inflation coming in at 2.0% (down from 3.1%). This was as a result of a deflationary food environment and base effects from 2013 tariff hikes, which we expect to moderate in the coming months. We remain overweight the Ugandan shilling relative to the Kenyan Shilling as we believe that the central bank will continue to keep real rates high to maintain currency stability while running an expansionary fiscal program. Zambia Uncertainty around the health of President Michael Sata, resolution of exporters VAT repayments and weak Chinese growth all weighed on the local unit over the month. President Sata failed to give his scheduled address at annual UN meetings due to illness and was subsequently flown back to Zambia where uncertainty around a succession and a lack of communication has encouraged the local succession rumour mill. The ministry of finance made another U-Turn regarding the repayment of $600m of VAT refunds to exporters, when the initial decision to repay was followed by an announcement of a delay to further study the impact of repayment. We expect clarity on VAT repayments when the budget is announced on the 10 October 2014, and with recent pressure from global mining houses to cut investment and jobs in the country due to the VAT issue, we expect the government to acquiesce and repay in a staggered fashion. We reduced our overweight over the month after a strong run but remain positive given IMF involvement and the high yield on offer. 9 Asia China Economic data took a turn for the worse last month but, with the latest PMI stabilising, growth is not expected to capitulate from here. The property sector remains a headwind to growth, offset somewhat by the services sector and strong external demand resulting in impressive trade numbers. We expect this theme to continue, with the strong trade balances likely to keep the renminbi on a relatively strong trend. We retain our overweight in the currency. India Inflationary pressures are expected to moderate over the next couple of months as the monsoon rains pick up. Nevertheless, the central bank kept rates on hold this month, sighting risks to the upside on its medium-term inflation targets. S&P upgraded its outlook to ‘Stable’ from ‘Negative’, alleviating fears of a potential downgrade to junk status. We increased our overweight in the rupee. Indonesia Politics made an unexpected turn for the worse. The opposition coalition led by Prabowo has gained strength and is making life difficult for President-elect Joko Widodo. We still expect a strong economic team to be named and fuel hikes to be pushed through, but it looks like it will be difficult for Widodo to conduct more reforms until he gains more political support. Based on modest fundamental improvements, we maintain a small overweight in the currency as well as hard currency bonds, but are monitoring closely. Malaysia The fuel subsidy cuts were a positive surprise as markets were beginning to worry about the commitment to fiscal consolidation. Based on these developments, we remain comfortable with our small overweight position in the ringgit. We remain neutral local bonds which are close to fair value in our view, especially as inflation will remain somewhat elevated. Philippines he central bank hiked interest rates again and with a slight drop in inflation during September, it clearly shows they have moved ahead of the curve for now. While the balance of payments position remains strong, with very low implied interest rates on currency forwards and valuations around fair value, we remain neutral the peso. We remain underweight hard currency bonds on expensive valuations. Singapore Economic data remains mixed. We expect no change in the policy settings at the central bank’s October meeting, but do expect they will be most comfortable with the currency in the lower end of the band given the challenges facing some export sectors, especially in electronics. We remain overweight local bonds and underweight the currency. South Korea Policymakers have been voicing their concerns over the continued appreciation of the won vis-à-vis the Japanese yen, and the impact this has on Korean export competitiveness. Based on this dynamic, we closed our overweight in the won and moved to an underweight position later in the month. The bond market has priced in a high chance of further rate cuts, hurting our underweight position in bonds; we think the risk is that the central bank stays on hold as growth continues to recover moderately, hence we retain our position. Sri Lanka While exports continue to perform well, import growth has picked up meaningfully over the last couple of months, resulting in a notable widening of the trade balance. Given the change in this dynamic, we took profits on our overweight in hard currency debt as spreads continued to outperform the benchmark and similarly rated peers. 10 Taiwan Data has turned a little less positive over the month, with a notable drop in the PMI and trade data disappointing. A big drop in inflation last month means the central bank is unlikely to allow the Taiwan dollar to appreciate from here, and there is a risk that Occupy Central protests could lead to further unrest in Taiwan. We remain underweight the Taiwan dollar. Thailand GDP growth and imports are rebounding slowly. The military government is increasing spending, mostly on infrastructure, but broadly-speaking is applying fiscally prudent principles. The central bank seems clearly on hold, allowing little room for bonds to rally, and as such we remain underweight. With exports still weak, we believe the baht will underperform relative to its peers. Corporate bonds Focus of the Month: Oil E&P companies In the JPMorgan CEMBI index, 8.5% of issuers are oil exploration and production companies. The headline oil prices have been declining recently with Brent down 20% YTD. The oil prices started declining in early July, and, as a result, we should see the first real impact on company financials in third-quarter results, which will be released over the coming weeks. Our in-house financial modelling allows us to estimate the impact of the downward moves in oil prices on the issuer’s credit quality ahead of the results. Initially, we consider the different oil benchmarks that our companies follow. Brent is the most liquid oil price benchmark, but other benchmarks also represent a meaningful portion of the oil market. Over the last three months, Brent, Dubai benchmark and WTI have declined in line by 16-18%. The oil benchmarks are usually quoted in U.S. dollars, but emerging market oil producers face most of their operating cost and a substantial portion of their capital expenditure in local currencies. With local currencies weaker in the third quarter vis-à-vis USD, the oil price impact on the bottom line of emerging market oil companies will be less than the USD-denominated oil prices suggest, because a substantial proportion of costs is local currency linked. For example, most oil producers from EM countries have a 4-10% pricing mitigant due to EM currency devaluation, with the extreme example being rouble denominated Brent oil, which is down only 6% since June 30th. In addition to oil prices, we focus on the volume growth for the oil producers. We expect our selected high yield oil credits to deliver 5-15% production growth on a year-on-year basis. This should mitigate the recent decline in oil prices. Our portfolio companies are also positioned in the lowest half of the oil cost curve, and as such enjoy a substantial cushion unlike the higher cost producers. Overall, at the current oil prices, we expect some increase in leverage and deterioration in cash flows among emerging market oil producers. However, the oil price decline should be mitigated by local currency weakness, production growth and a competitive positioning on the cost curve. We continue to monitor the demand-supply dynamics in the oil market that ultimately drives the oil price. Should oil prices adjust further, we will be recalibrating our positioning in the sector. Sector-by-sector Commodity Emerging market (EM) financial bonds retreated slightly during September. Brazilian banks were the biggest underperformers as election results surprised the market negatively, while Russian banks recovered from the previous month’s low levels and outperformed. The new issue market was busy after the summer holidays, and continued to be dominated by Basel III-compliant subordinated issuances. We remain underweight Russia and increased positions in selective high yield names with stable fundamentals and attractive valuations. Financials Emerging market (EM) financial bonds retreated slightly during September. Brazilian banks were the biggest underperformers as election results surprised the market negatively, while Russian banks recovered from the previous month’s low levels and outperformed. The new issue market was busy after the summer holidays, and continued to be dominated by Basel III-compliant subordinated issuances. We remain underweight Russia and increased positions in selective high yield names with stable fundamentals and attractive valuations. 11 Heavy Industrial We remain overweight industrials in Latin America, with a bias towards investment grade companies. We expect Latin American infrastructure companies to benefit from state sponsorship through infrastructure spending, while many Asian industrials have been impacted by weaker demand from property companies in China and slower GDP growth. Real Estate The real estate sector had a reasonable month in September. China’s market remained weak; prices recorded a further decline in August, though volumes rose. However, bonds were supported by fresh stimulus measures from the government, notably the relaxation of restrictions on second-time home buyers and the injection of capital into the top four state-owned enterprise (SOE) banks to facilitate mortgage lending. Longer-dated bonds were re-priced for expectations of higher US interest rates. In Indonesia, the bigger developers continued to show improving pre-sales. TMT September was a weak month for the TMT index. Large high yield telecoms companies in Latin America (LATAM) were sold by US accounts taking profit and reducing exposure to off-index investments, which had a negative impact on relative performance due to our overweight in some of these credits. However, this was offset by our investments in Asian investment grade credits, which held up well. Consumer It was another tough month for the Agricultural credits, with further weakness from Mriya Agro Holding on its restructuring plans infecting other Ukrainian agricultural names. In LATAM, concerns over the headwinds from depressed sugar prices pushed yields wider in the highly-levered sugar and ethanol players. While we continue to watch the sector closely – as we are concerned over economic instability pressuring the real consumers –, we take comfort from our maintained exposure to the industry through the more geographically-diverse players, such as those involved in the global protein sector. Utilities With Brazilian election polls suggesting a tight race, concerns that the incumbent president, Dilma Rousseff, would stay in power drove yields wider in the state controlled utilities. The increasing degree of state intervention experienced by such firms during Rousseff’s current term has meant that investors regard them as offering limited profitability. We prefer to maintain the bulk of our utility exposure in corporates which benefit from strong governmental support through clear regulation, allowing the corporates to invest with a clear grasp on future profitability and thus maintaining stronger standalone credit fundamentals. 12 Important information This document is not for general public distribution. If you are a private investor and receive it as part of a general circulation, please contact us at +44 207 597 1900. The information discusses general market activity or industry trends and should not be construed as investment advice. The economic and market forecasts presented herein reflect our judgment as at the date shown and are subject to change without notice. These forecasts will be affected by changes in interest rates, general market conditions and other political, social and economic developments. There can be no assurance that these forecasts will be achieved. Investors are not certain to make profits; losses may be made. Past performance should not be seen as a guide to the future. The information contained in this document is believed to be reliable but may be inaccurate or incomplete. Any opinions stated are honestly held but are not guaranteed and should not be relied upon. This communication is provided for general information only. It is not an invitation to make an investment nor does it constitute an offer for sale and is not a buy, sell or hold recommendation for any particular investment. In the US, this communication should only be read by institutional investors, professional financial advisors and, at their exclusive discretion, their eligible clients. It must not be distributed to US Persons apart from the aforementioned recipients. In Australia, this document is provided for general information only to wholesale clients (as defined in the Corporations Act 2001). All data sourced from Bloomberg and Investec Asset Management. Outside the US, telephone calls may be recorded for training and quality assurance purposes. Issued by Investec Asset Management, October 2014. For more information please contact: Australia Level 23, The Chifley Tower 2 Chifley Square Sydney, NSW 2000 Telephone: +61 2 9293 6257 Facsimile: +61 2 9293 2429 Botswana Plot 64511, Unit 5 Fairgrounds, Gaborone Telephone: +267 318 0112 Facsimile: +267 318 0114 Channel Islands PO Box 250, St Peter Port Guernsey, GY1 3QH Telephone: +44 (0)1481 710 404 Facsimile: +44 (0)1481 712 065 Europe (ex UK) Woolgate Exchange 25 Basinghall Street London, EC2V 5HA Telephone: +44 (0)20 7597 1999 Facsimile: +44 (0)20 7597 1919 19422 - 10/14 www.investecassetmanagement.com Hong Kong Suites 2602-06, Tower 2 The Gateway, Harbour City Tsim Sha Tsui, Kowloon Hong Kong Telephone: +852 2861 6888 Facsimile: +852 2861 6861 Namibia 100 Robert Mugabe Avenue Office 1, Ground Floor Heritage Square Building Windhoek Telephone: +264 (61) 389 500 Facsimile: +264 (61) 249 689 Singapore One Fullerton #02-01 1 Fullerton Road Singapore, 049213 Telephone: +65 6832 5052 Facsimile: +886 2 8101 0900 South Africa 36 Hans Strijdom Avenue Foreshore, Cape Town 8001 Telephone: +27 (0)21 416 2000 Facsimile: +27 (0)21 416 2001 Taiwan Unit C, 49F, Taipei 101 Tower No.7, Section 5, Xin Yi Road Taipei 110, Taiwan Telephone: +886 2 8101 0800 Facsimile: +886 2 8101 0900 United Kingdom Woolgate Exchange 25 Basinghall Street London, EC2V 5HA Telephone: +44 (0)20 7597 1900 Facsimile: +44 (0)20 7597 1919 United States 666 5th Avenue, 37th Floor New York, NY10103 US Toll Free: +1 800 434 5623 Telephone: +1 917 206 5179 Facsimile: +1 917 206 5155

© Copyright 2026