Beef Market Trends

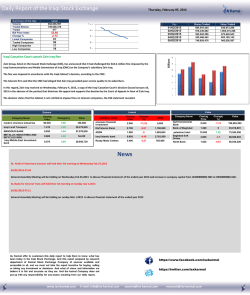

_________________________________________________________________________ AGRI TRENDS Weekly Market Analysis W 30 January 2015 The world sugar situation! There have been large amounts of sugar in the world market, and hence the lower sugar prices. The rise in prices earlier this decade encouraged a major expansion in production which has led to a quick build-up in stocks. For 2015, the world sugar output is however expected to decrease, as lower prices are depressing the industry and discouraging production. The lower prices have resulted in the closing down of mills because they were not profitable, especially in Brazil. Brazil and India are the biggest producers and they are both under pressure. In India, The lower prices have put increasing pressure on the government to subsidize exports and reduce stockpiles. On the local front, the drought in the KZN is expected to reduce production levels. The January 2015 RV price for the 2014/15 season in respect of the cane delivered in December 2014 was declared at R3358/t. Beef Market Trends International:.High supplies out of New Zealand, as well as the impact of the port slowdown in the US has flowed through to manufacturing beef prices over the past week. The port slowdown makes buyers hesitant, and there are also reports in the market that recent storms slowed food service demand, as customers were likely to stock up at the supermarket and stay indoors. Schedules have however continued to soften with the dry weather. New Zealand steers and cows traded 1,08% and 1,45% lower at NZ$ 457 and NZ$ 340 per head. The US cattle herd has expanded in 2014, for the first time in eight years. The USDA has reported that the nation’s cattle supply increased by st 1% in the year through the 1 of January to 89.8 million head. In the US, beef traded mostly lower as follows: Top side traded lower at $275,84/cwt, Rump traded higher at $358,44/cwt and Strip loin traded lower at $498,35/cwt. Chuck traded lower at $318,58/cwt, Brisket traded lower at $341,22/cwt which gave us on average carcass price of $355,56/cwt. Domestic: When compared to last week, prices have traded mostly lower. The prices of the different meat classes were as follows: Class A prices decreased by 2.84% to 32.20/kg, Class C prices increased by 2,75% to R28.67/kg and Contract prices decreased by 1,61% closing at R32.99/kg fifth quarter included. The weaner prices traded slightly lower compared to last week and at R21.11/kg. The average hide price traded slightly lower at R18,09/kg. Hide prices have been on a downward trend over the past months following the international prices lower. Absa Weekly Market Analysis Outlook Internationally, beef prices are expected to move sideways in the short term with a possible downward pressure due to higher supplies out of New Zealand and the port slowdown. In the medium term, possibilities of good rains could slow slaughter rates in Australia, which could support prices. Normally during January and February, prices tend to drift lower due to the overhang of the overspending during the festive season, and the demands on consumers as the new school year stars. Currently, it is a typical January-February months in terms of supply and demand, and therefore prices are expected to remain at soft levels. Mutton Market Trends International: In New Zealand, this January, dry conditions have forced many farmers to slaughter, pushing more lambs on to the market, which should also provide an atmosphere of a well-supplied market for Easter demand. Demand is yet to pick up in a number of key markets including China and the Middle East. Markets are resistant to take on more stock because there are significant inventories already in place, leading to softening in export returns from these markets. Schedules have continued to be soft. The New Zealand lamb and mutton traded lower this week compared to last week; lamb closed the week at NZ$75.7/head for 15kg. Ewes closed lower at NZ$56.4/head for a 21kg ewe. Import parity prices for lamb and mutton were slightly mixed at R52.86/kg and R36.69kg respectively as there were declines in international prices. Australian supplies are expected to start tightening in 2015 and exports return to normal levels should good rainfall continue to be realized. There are expectations of reduced supplies in Australia.. Domestic: The mutton prices traded slightly stronger during the week with Class A trading slightly higher at R56.65/kg and Class C slightly higher at R41.17/kg compared to the previous week. The price for feeder lambs traded slightly higher at R24.01/kg. The average price for dorper hides traded higher at R95/hide and merino traded slightly lower at R60,83/hide respectively. The landed imported price of mutton rib from Australia and New Zealand traded slightly higher at R 27,80/kg compared to the previous week and mutton shoulders traded the same at 44,25/kg according to (Association of Meat Importers and Exporters) AMIE. Outlook Internationally, prices should remain soft on the back of softer demand in the market and slow growth in global economies. The market is currently well supplied. Demand is expected to improve in the weeks heading to Easter. In the medium term, good rains out of Australia are expected to curb domestic supplies. Locally, prices are expected to be under pressure in line with seasonal trends and higher volumes as lambs come to weight. Absa Weekly Market Analysis Pork Market Trends International: US pork prices all traded lower over the past week, despite a decrease of 5,85% in loads. Carcass prices traded 7.26% lower at US$78.04/cwt, Loin traded lower at US$87.13/cwt, Rib prices traded 3.38% lower at US$145,57/cwt and Ham traded lower at US$63.08/cwt. The import parity decreased on the back of the lower international prices. US hogs continued to trade at lower levels last week, as herds bounce back from a virus. New vaccines and herd immunity have slowed the spread of the virus. Market watchers are bracing for record production as hogs bred after the virus was brought under control to reach slaughter weight. The USDA has reported that an estimated 2.32 million hogs were processed for pork in the week though 24th of January, which is an increase of 4.6% from the same week last year. The big supplies comes at the same time that demand is slowing, as US pork exports have fallen in recent months. Domestic: Domestic prices have declined over the past week with Porker prices at R25.80/kg while Baconer prices still strong at R24.00/kg. Last year, prices were on an upward trend while grain prices were low which in turn improved the profitability in the industry. Outlook Internationally, prices are expected to soften slightly as a result of higher supplies in the market, as production volumes increase on the back of lower grain prices. Domestic prices are also expected to continue to decrease on the back of higher production volumes. In some regions demand is not too strong and there are enough supplies in the market. The industry as a whole will, however, remain highly profitable especially if the rains continue to increase grain yields. Absa Weekly Market Analysis Poultry Market Trends International: The poultry prices in the US traded mostly lower over the week compared to the past week, because there are higher volumes in the market. Whole bird prices traded 2.96% lower and at 93.9 USc/lbs. Breasts and leg Quarters traded at 138,0 USc/lbs and 45.0 USc/lb respectively. In the US, broiler supplies have been increasing steadily in the past few months. The latest data also points out that higher production volumes is expected to continue into February and March. The growth in production is expected to come through both higher slaughter numbers as well as notable increases in broiler weights. Meanwhile, Ghana is considering banning Nigerian poultry products on a temporary basis after reports of rising cases of avian flu. This ban is to prevent the spread of the disease. Domestic: Poultry prices remained firm during this week compared to the previous week. Frozen birds traded slightly higher at R22.97/kg compared to the previous week. Whole fresh medium bird prices traded slightly higher at R23.14/kg while IQF traded slightly lower at R19.93kg. There are talks that there is no build-up of stocks in the market currently and that there is sufficient to good demand to support the stock levels. There are however some low value products that are currently well supplied. The South African Poultry Association is trying to reach an agreement with the US poultry exporters on how much US poultry should be allowed into the country. This comes as the industry is under pressure from US exporters to end duties on poultry imports. These US exporters have threatened to block the inclusion of SA in the new US-Africa Agoa (African Growth and Opportunity Act) trade agreement should the country not be compliant. Outlook Internationally, prices are expected to maintain the downward trend as a result of higher production volumes, and pressure from competing meats. This is due to expected higher slaughter rates and expected increases in broiler weights. Domestic prices are also expected to decline in line with seasonal trends. There is however sufficient demand to meet supplies, as there is not a build-up of stocks in the market. Livestock Prices (R/kg) 30 Jan 2015 Beef Mutton Pork Poultry Current Week Previous Week Current Week Previous Week Current Week Previous Week Current Week Previous Week Class A / Porker / Fresh birds Class C/ Baconer / Frozen birds Contract / Baconer/ IQF Import parity price 32.20 33.14 56.65 54.45 25.80 25.82 23.14 23.08 28.67 27.90 41.17 38.77 24.00 23.85 22.97 22.88 32.99 33.53 57.00 55.27 24.90 24.84 19.93 20.03 49.81 51.46 36.67 36.48 24.21 27.11 15.39 15.27 Weaner Calves / Feeder Lambs/ Specific Imports: Beef trimmings 80vl/b/Mutton Shoulders/Loin b/in /chicken leg1/4 21,11 21,28 24,01 24,00 - - 50,45 50,45 44,25 44,25 37.50 37.60 20.85 20.80 Absa Weekly Market Analysis Yellow Maize Trends International: When compared to the previous week, maize closed the week lower. The average US yellow maize spot price closed the week 3.55% lower at US$171,73. Maize saw pressure from favourable crop conditions in South America as well as ample global grain supplies. Prices were weighed down by the large world supplies as well as soft demand. There seemed to be good exports from Ukraine, which provided strong competition for the US crop. There are cargo backups at the West Coast ports as a result of labour disputes, and this is also pushing the prices of maize down in Illinois. China, on the other hand has large domestic stocks which might lessen demand from that side. Domestic: The local maize market for yellow maize traded 0.18% higher at R2016/ton, on the back of weather concerns. Prices are lower than a year ago, mainly as a result of good summer rains up to now creating the perception that stock levels will increase. However, weather may influence prices significantly. The average exchange rate for the week moved sideways to R11,55/US$ compared to R11,55US$ the previous week. The futures prices traded higher as follows: Mar-15 contracts increased by R56/t to R2094, May-15 contracts increased by R25/t to R2065/t, Jul-15 increased by R38/t to R2058/t, Sep-15 contracts increased by R33/t to R2091/t while Dec-15 also increased by R33/t to R2148/t. The Crop estimate Committee (CEC) released the preliminary area planted estimates last week. The report showed that the preliminary area estimate for maize was at 2,656 mil hectares, which is a decrease from 2,688 mill hectares which was planted in the previous season. However, the area for yellow maize was 31800 hectares higher than that planted in the previous season at 1,169 mill hectares. Outlook International maize prices are expected to remain bearish, with pressure coming from the ample global supplies and favourable conditions in South America. On the local front, prices increased on the back of dry weather conditions. However, there were some scattered showers in parts of Mpumalanga, North West and western Free State, which unfortunately were not enough to bring some relief. Prices are expected to continue to increase in the next week as dry conditions are expected to remain, especially in the western side of the country, and therefore provide some support to prices. Recent weather forecasts continue to show no signs of rain this coming week. Yellow Maize Futures 30 Jan 2015 CBOT ($/t) SAFEX (R/t) Ask 2,100 2,060 2,020 May-15 Put 120 98 79 Mar-15 May15 Jul-15 Sep-15 145.66 2,094 148.197 2,065 Jul-15 Ask Put 151.96 154.72 157.71 2,091 2,148 Sep-15 Ask Put Call Call 85 103 124 2,100 2,060 2,020 145 123 102 2,058 Call 103 121 140 2,140 2,100 2,060 Dec-15 173 151 130 124 142 161 Absa Weekly Market Analysis White Maize Trends International: The US white maize spot market traded 1.27% lower at an average of US$ 160.22/t over the past week compared to an average of US$ 162.29/t the previous week. Import parity prices traded 0.93% lower, compared to the previous week supported by the lower international prices. Domestic: The local average white maize spot price traded 0.18% higher or R3,60/t higher at R2016/t compared to the previous week. This was due to weather concerns. The CEC results have revealed its area estimates for white maize at 1,488 mill hectares, which is a decrease of 63550 hectares from the previous season. Outlook Internationally, white maize price are expected to continue with decreases as with yellow maize prices in the short term due to ample global supplies. Locally prices are expected to follow the trend of the local yellow maize. White Maize Futures 30 Jan 2015 SAFEX (R/t) May-15 Ask Put Mar-15 2,123 Call Ask May15 Jul-15 Sep-15 Dec-15 2,101 Jul-15 Put 2,096 2,130 2,180 Call Ask Sep-15 Put Call 2,140 126 87 2,140 148 104 2,160 165 135 2,100 104 105 2,100 126 122 2,120 143 153 2,060 84 125 2,060 106 142 2,080 123 173 Absa Weekly Market Analysis Wheat Market Trends International: Wheat closed the week lower compared to the previous week. Wheat saw some losses due to weak export demand as well as plentiful world supplies. Indications that global supplies are more than enough to meet demand continued to drive prices down. Wheat prices were under pressure from favourable weather in key US producing regions. The average weekly wheat spot price traded 3.52% lower compared to the previous week at US$228,8/t. Soft red wheat traded 2.94% lower, while hard red wheat traded 4.05% lower. Import parity traded 2.8% lower due to the lower international prices. Beneficial rain is expected to continue in the US, after showers improved moisture in the past weekend. There are also reports of the slowdown in exports in Russia and Ukraine. Domestic: The average SAFEX wheat spot price increased from last week’s and traded at R3911/t despite the lower international prices. Mar-15 futures increased by R68/t to R3968/t, May-15 futures increased by R72/t to R4027, Jul-15 futures traded higher by R58/t to R4038/t while Sep-15 traded R1/t higher at R3904/t. the CEC released the production estimates, and has shown that the expected production of wheat for 2014/15 season is 15500 tons higher than the previous forecast at 1,776 mill tons. Outlook Internationally, wheat prices are expected to follow a downward trend in the short to medium term due to large global supplies in the market which should put pressure on market prices. Further pressure will also be from the favourable growing conditions in the US. Domestic prices can be pressured this coming week by the production results of the crop estimate committee as well as the ample supplies in the international market. However, the weaker exchange rate could pressure prices, and therefore prices could continue trading higher. Wheat Futures 30 Jan 2015 SAFEX (R/t) CME ($/t) May-15 Ask Put 4,060 4,020 3,980 118 97 78 Mar 2015 May 2015 Jul 2015 Sep 2015 Dec 2015 3968 184.67 4027 186.14 4038 187.91 3904 190.92 n/a 195.55 Call Ask Jul-15 Put 85 104 125 4,080 4,040 4,000 155 133 113 Call Ask 113 131 151 3,940 3,900 3,860 Sep-15 Put 170 148 129 Call 134 152 173 Absa Weekly Market Analysis Oilseed Market Trends International: Soybeans closed the week lower compared to the previous week. Soybeans saw spillover pressure from other grains and better than average yields in South America. Further pressure was drawn from the weakening demand in China, with prices of the oilseed dropping 5.99% in January. There is optimism over crop prospects in Brazil and Argentina, which reinforces the idea for ample global supplies. This Monday, prices continued to be weighed down, with the crop weather improving in South America, with scattered showers in Brazil this week easing concerns about drought decreasing soybean yields. Soybean prices week on week traded 1.2% lower at US$ 353.11/t. Soya meal traded at US$336/t, which is higher compared to the previous week while soy oil traded 5,5% lower at US$30.43/t compared to a week ago. Domestic: The average soybean spot prices traded 2,29% lower at R5549/t compared to the previous week. This is due to the lower international prices. The average sunflower spot prices for the week traded 0.76% lower at R4,940/t compared to the previous week. The CEC has estimated an increase in soybean plantings at 620 300 hectares. The area estimate for sunflower seed is however less than that of the previous season at 561 000 hectares. Outlook Internationally, prices are expected to continue to slide lower over the short to medium term due to expectations of a bumper South American crop, which would boost the already abundant global supplies. Additional cancellations from China could further pressure prices. Locally, the soybean prices are expected to trade sideways to downwards in the short to medium term following the lower international prices. Nonetheless, the weather market is expected to continue to have a significant impact on the domestic price movements. Oilseeds Futures 30 Jan 2015 Mar-15 May-15 Jul-15 Sep-15 Dec-15 CBOT Soybeans (US $/t) 353.11 355.53 357.37 351.49 349.58 CBOT Soy oil (US c/b) 30.00 30.24 30.46 30.52 30.29 CBOT Soy cake meal (US $/t) 329.90 324.00 321.80 319.40 314.10 SAFEX Soybean seed (R/t) 5,263 4,850 4,890 4,940 n/a SAFEX Sunflower seed (R/t) 5,020 4,859 4,913 n/a 5,000 SAFEX Sorghum (R/t) 2,200 2,200 2,200 2,500 n/a Sunflower Calculated Option Prices (R/t) Absa Capital Trading Desk: 011 – 895 5524 Mar-15 May-15 Jul-15 Ask Put Call Ask Put Call Ask Put Call 5,060 144 104 4,900 199 158 4,960 316 269 5,020 123 123 4,860 177 176 4,920 294 287 4,980 103 143 4,820 157 196 4,880 273 306 Absa Weekly Market Analysis International: The Australian wool was stronger for the week in the market and Wool & Cotton Price Trends closed higher on Au 1070c/kg. Cotton 13,000 has also increased and showed some 12,500 Weeks recovery over the past week and closed 12,000 at US 57,74c/lb. India has made a 11,500 decision to sell fibre in the domestic 11,000 market at a time when China is going 10,500 slow on imports. This could put further 10,000 downward pressure on global prices. 9,500 India is the world’s second biggest 9,000 producer of cotton. In New Zealand, 03/10/14 07/11/14 12/12/14 16/01/15 03-15 lamb wool prices increased at auctions Australia Wool SA Wool SA Cotton in the past week due to increased *Last 3 points 3 months forecast demand for the fibre used in clothing, as buyers benefited from a decline in the local currency. Wool (c/kg) 2,550 2,450 2,350 2,250 2,150 2,050 1,950 1,850 1,750 1,650 1,550 1,450 Cotton (c/kg) Fibres Market Trends th Domestic: The last wool auction for 2014 took place on the 28 Jan 2015. The local market traded lower and closed 5.21% lower than the previous sale. The market has reported good demand for good quality wool. The next sale will be on the 04th of February. Domestic cotton prices have increased on the back of higher international prices. Outlook Prices of fibre are expected to be under pressure in the short term, and this leads to the short term outlook of decreases in prices, drawing pressure from the lower oil prices. Should demand improve, prices might gain some support. Fibres Market Trends Week ending 30 Jan 2015 Wool prices SA (c/kg) prices Wool market indicator 19μ micron 21μ micron Cotton prices 10562 11515 10801 SA derived Cotton (R/kg) Cotton Prices 17.10 Australian prices (SA c/kg) 9,850 11,041 10,528 New York AIndex (US$/kg) 1.48 Australian Future Mar 2015 (AU$/kg) 11,75 11,45 New York future Mar2015 (US$/kg) 1.32 Australian Future Jul – 2015 (AU$/kg) 11,60 11,30 New York future Jul-2015 (US$/kg) 1.33 Absa Weekly Market Analysis Vegetables Market Trends Cabbage: Cabbage prices increased this week by 1,8% week on week to R3421/t. The price increase was despite to a 10,3% increase in volumes. Prices are expected to continue to move sideways to upwards in line with seasonal trends. Carrots: Carrot prices decreased by 11,8% week on week to R2590/t. The price decrease was due to a 15,1% increase in the volumes of carrots. Prices are expected to continue to move sideways to downwards due to higher supplies. Onions: Onion prices decreased by 3,4% week on week to R2687/t. The price decrease was due to a 18,1% increase in volumes compared to the previous week. Prices are expected to trade sideways due to higher supplies and less demand after month end buying. Potatoes: Potato prices increased by 3,0% week on week to R2519/t. The increase in prices was despite increases in volumes of 12,2% compared to the previous week. Prices are expected to trade sideways in the short term and continue with the downward trend weighed down by wet bags of potatoes and the poor quality potatoes in the market. Tomatoes: Tomato prices increased 47.9% week on week to R8324/t. The price increase was due to a decrease in volumes of 13,9% during the past week. Prices are expected to carry on with the upward trend supported by lower volumes as well as following seasonal trends. Vegetable Prices: Fresh Produce Market (Averages on the Pretoria Bloemfontein Johannesburg Cape Town and Durban markets) Week ending This week’s Previous This week’s Previous week’s 30 January 2015 Average week’s Total Total Price (R/t) Average Volumes (t) Volumes (t) Price (R/t) Cabbages 3421 3360 1279 1159 Carrots 2590 2938 1985 1725 Onions 2687 2782 6499 5505 Potatoes 2519 2447 13201 11767 Tomatoes 8324 5629 3379 3923 Disclaimer: Although everything has been done to ensure the accuracy of the information, Absa Bank takes no responsibility for actions or losses that might occur due to the usage of this information. Enquiries: Karabo Takadi Analyst: Agri Info Absa Agri-Business E-mail: [email protected]

© Copyright 2026