newsrelease acquisition announcement

N

E

W

S

R

E

L

E

A

S

E

2 February 2015

ACQUISITION ANNOUNCEMENT

THIS ANNOUNCEMENT AND THE INFORMATION CONTAINED HEREIN IS RESTRICTED AND IS NOT FOR

RELEASE, PUBLICATION OR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN WHOLE OR IN PART, IN OR INTO THE

UNITED STATES, CANADA, AUSTRALIA, JAPAN, SOUTH AFRICA, JERSEY OR ANY OTHER STATE OR

JURISDICTION IN WHICH SUCH RELEASE, PUBLICATION OR DISTRIBUTION WOULD BE UNLAWFUL.

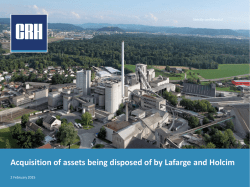

Proposed Acquisition of certain assets being disposed by Lafarge S.A. and Holcim Ltd

CRH plc ("CRH" and together with its subsidiaries, the "Group") announces that it has entered into a binding

commitment to acquire certain assets (hereafter referred to as “NewCo” or the “Business”) from Lafarge S.A.

("Lafarge") and Holcim Ltd ("Holcim" and together with Lafarge referred to as the “Sellers”) for an Enterprise

Value of €6.5bn (the “Acquisition”).

Key highlights

•

•

•

•

•

•

•

•

•

•

•

Enterprise Value (“EV”) of €6.5bn

Funded by €2.0bn cash from balance sheet, new debt and a 9.99% equity placing

NewCo 2014E* EBITDA of €752 million

€90m net synergies run rate by year three

Acquisition of high quality assets across four regional platforms with leading market positions

On completion, CRH will be the global #3 building materials player

ROIC in-line with CRH's WACC in first full year of ownership

c.25% EPS accretive in first full year of ownership

Pro-forma 2014E* net debt / EBITDA expected to be 3.2x, to be reduced by disposals arising from

previously announced portfolio review

Completion expected mid-2015

CRH 2014 EBITDA guidance confirmed to be not less than €1.625bn

Commenting on these developments, Albert Manifold, CRH Chief Executive, said:

“This transaction represents a significant value creation opportunity for CRH. We are acquiring a quality

portfolio of assets, which complement our existing positions, at an attractive valuation and at the right point of

the cycle. The acquisition strengthens our presence in important markets across North America, Western,

Central and Eastern Europe as well as providing new platforms for growth in emerging markets. The assets will

integrate well into existing CRH networks benefiting from our strong business-building capabilities while

providing an important platform for future development opportunities. We have maintained our disciplined

investment approach through our continued focus on capital efficiency and remain focused on bringing returns

back to peak during this cycle.”

Information on NewCo

NewCo is a global producer of cement, aggregates, ready-mix and related construction activities across four

major platforms in North America, Western Europe, Central & Eastern Europe and Emerging Markets. In 2013

NewCo produced 23mt of cement, 79mt of aggregates, 8mt of Asphalt and 10m m³ of RMC. NewCo is expected

to generate 2014E* revenue of €5.1bn and EBITDA of €752 million. Approximately two-thirds of NewCo’s

revenue is generated in the European region. Outside Europe, Canada is the largest country in terms of 2014E

revenue, generating €1.0bn, with Brazil and the Philippines generating a further combined €0.6bn.

* 2014E is used throughout this announcement to indicate numbers which are approximate pending audit finalisation

CRH plc, Belgard Castle, Clondalkin, Dublin 22, Ireland TELEPHONE +353.1.404.1000 FAX +353.1.404.1007

E-MAIL [email protected] WEBSITE www.crh.com Registered Office, 42 Fitzwilliam Square, Dublin 2, Ireland

Page 2 of 12

Acquisition Announcement – 2 Feb 2015

The Business has market leading positions and covers all segments of the building materials sector in

developed, transition and emerging markets. It operates 24 integrated cement plants together with 10 grinding

stations for a total capacity of approximately 36 million tonnes per annum. NewCo has approximately 15,000

employees across 11 countries (Canada, the United States, Great Britain, Romania, Serbia, Slovakia, Hungary

Germany, France & La Reunion, Brazil and the Philippines).

Financial Highlights

Assuming completion in mid-2015, the acquisition of NewCo is expected to be c.25% accretive to underlying

earnings and to generate a ROIC in line with CRH’s weighted average cost of capital in the first full year of

ownership. Return on equity is expected to be in the high teens in 2016 and RONA in line with previous returns

generated by CRH.

CRH proposes to finance the Acquisition through a combination of €2.0bn cash on balance sheet, bank facilities

and the proceeds of an equity placing of 9.99% of CRH’s current issued share capital.

Balance sheet strength remains a key focus for the Group. 2014E pro-forma net debt to EBITDA ratio is

approximately 3.2x, before taking account of any future disposals arising from the previously announced

portfolio review by CRH in 2014. CRH remains strongly committed to its investment grade credit rating.

Transaction Rationale

The Board of CRH believes the acquisition of Newco is a compelling strategic opportunity for CRH:

•

NewCo represents a geographically diversified portfolio of high quality assets with leading market

positions and provides a strong strategic fit across 4 strong growth platforms;

•

NewCo is highly complementary to CRH’s existing footprint and the Business integrates well with

CRH’s existing network in North America, across Europe and in Asia.

o

NewCo’s assets in Canada and the US will significantly strengthen CRH’s number one market

positions in heavy building materials in the North-Eastern United States.

o

In Western Europe, NewCo’s assets are very complementary to CRH’s existing footprint in the

region, adding positions of scale in leading European economies. They will substantially

improve CRH’s existing cement network and link up with CRH’s significant downstream

operations.

o

The Acquisition will make CRH the largest building materials company in Central and Eastern

Europe with large infrastructure demands. It will allow CRH to build on its experience and

track record of building large and successful businesses in the region (Poland and Ukraine)

and to roll out its vertical integration model.

o

The Acquisition will double CRH’s exposure to Emerging Markets in a measured and balanced

way. CRH will enter markets with attractive long term economic prospects offering significant

growth as cement consumption increases, building on the experience gained from its existing

footprint in India and China.

o

In all regions the addition of NewCo provides new development opportunities and new

platforms for future growth for CRH, allowing the Company to expand its bolt-on acquisition

* 2014E is used throughout this announcement to indicate numbers which are approximate pending audit finalisation

Page 3 of 12

Acquisition Announcement – 2 Feb 2015

model in four new platforms and expanding its vertical integration model of downstream

businesses.

•

The Acquisition is being executed at the right time for CRH and at an attractive valuation:

o All-time-low cost of funds;

o Heavyside sector earnings at cyclical low and industry margins at trough levels; and

o Growth phase of global construction cycle.

•

The Acquisition has significant value creation potential as CRH has identified € 90m of synergies (net of

implementation costs) (1.8% of NewCo revenue) that will be achieved in the first three years post

acquisition. These synergies will be delivered by implementing CRH’s procurement programmes,

reducing costs through operational improvements and restructuring support services. These estimated

financial benefits are contingent on the Acquisition and could not be achieved independently.

•

The transaction creates further value for shareholders by providing the opportunity to re-allocate

capital at attractive multiples in recovering regions.

•

NewCo is expected to deliver highly attractive financial returns, with ROIC expected to be in line with

CRH’s weighted average cost of capital in the first full year of ownership, with good organic earnings

growth augmented by significant additional value from synergies, cost savings and operational

efficiency improvements.

The Acquisition constitutes a Class 1 transaction pursuant to the UKLA Listing Rules and therefore requires the

approval of CRH's Shareholders. An Extraordinary General Meeting will be held in due course for CRH

Shareholders to approve the Acquisition. The Acquisition is also conditional upon 1) successful completion of

the Lafarge and Holcim merger and 2) completion of local reorganisation plans. The Acquisition is expected to

complete by mid-2015. Further details on the terms and conditions of the Acquisition are set out in the

Appendix to this announcement.

Transaction Structure

In order to effect this transaction, CRH has entered into a Binding Offer Letter with Holcim and Lafarge in which

it has committed to purchase the assets on the basis set out in this announcement. This enables Holcim and

Lafarge to enter into consultations with their Works Councils, as required by law, before they make a decision

whether to proceed with the transaction (the “Binding Offer Period”).

During the Binding Offer Period, Holcim and Lafarge have granted CRH exclusivity in respect of the assets and

cannot engage with any other party in respect of their sale. The completion of the Lafarge and Holcim merger is

conditional on the sale by Lafarge and Holcim of NewCo (excluding the Philippines Business).

Current trading and prospects

On 11 November 2014, CRH announced its interim management statement outlining its trading performance in

the first nine months of the year, in which it stated that:

“Assuming normal weather patterns for the remainder of the year and a US dollar/euro exchange rate of 1.33

(2013: 1.3281), we expect EBITDA for the fourth quarter to be broadly similar to the strong performance in the

final quarter of 2013. Against this backdrop, we reiterate our expectation for second-half EBITDA to be

somewhat ahead of last year (H2 2013: €1.08bn), resulting in expected full year EBITDA growth of c.10 per cent

in 2014 (2013: €1.475bn).”

* 2014E is used throughout this announcement to indicate numbers which are approximate pending audit finalisation

Page 4 of 12

Acquisition Announcement – 2 Feb 2015

Since that date, the Group's trading performance continues to be in line with the Board's expectations and we

expect EBITDA for the full year ended 31 December 2014 to be not less than €1.625bn with full year revenues

of €18.9bn. We expect year-end net debt to be approximately €2.5bn (2013: €3.0bn), with a net debt/EBITDA

ratio of approximately 1.5x. CRH will publish its preliminary results for the year ended 31 December 2014 on

26 February 2015.

NewCo’s estimated* outturn for the year ended 31 December 2014 was marginally ahead of initial

expectations, reflecting a strong finish to the year in the UK, while the results in the Philippines and Brazil were

slightly behind expectations.

A conference call for analysts and investors will be held today at 08.30am UK time. A presentation (the

“Presentation”) to accompany this call is available on the Results and Presentations page on CRH’s website at

www.crh.com

This summary should be read in conjunction with the full text of the accompanying appendices, the

Presentation and the Shareholder Circular which will be published in due course.

This Statement contains certain forward-looking statements as defined under US legislation. By their nature, such statements

involve uncertainty; as a consequence, actual results and developments may differ from those expressed in or implied by such

statements depending on a variety of factors including the specific factors identified in this Statement and other factors

discussed on pages 92 and 93 of our 2013 Annual Report and in each of our Annual Report on Form 20-F and Interim Results

contained in our Form 6-K filed with the SEC.

For further information, please contact CRH plc:

Contact CRH at Dublin (+353 1 404 1000)

Albert Manifold

Chief Executive

Maeve Carton

Finance Director

Frank Heisterkamp Head of Investor Relations

Mark Cahalane

Group Director Corporate Affairs

UBS Limited (Financial Adviser, Sponsor and Joint Corporate Broker)

Hew Glyn Davies

James Robertson

Alexandre Blanchard

Anna Richardson Brown

+44 (0) 20 7567 8000

BofA Merrill Lynch (Financial Adviser)

Jean-Eudes Renier

Peter Luck

+44 (0) 20 7995 2271

+44 (0) 20 7996 6429

JPMorganCazenove (Financial Adviser)

John Mayne

Hernan Cristerna

+44 (0) 20 7134 4315

+44 (0) 20 7134 3339

Davy (Financial Adviser, Irish Sponsor and Joint Corporate Broker)

Kyran McLaughlin

John Lydon

+353 1 679 6363

Goodbody (Financial Adviser)

+353 1 667 0400

Stephen Donovan

Joe Gill

Powerscourt (International Media)

Rory Godson +44 (0) 20 7250 1446

Drury Porter Novelli (Irish Media)

Billy Murphy +353 1 260 5000

* 2014E is used throughout this announcement to indicate numbers which are approximate pending audit finalisation

Page 5 of 12

Acquisition Announcement – 2 Feb 2015

UBS Limited, which is authorised by the Prudential Regulation Authority in the United Kingdom and regulated

in the United Kingdom by the Prudential Regulation Authority and by the Financial Conduct Authority, is acting

as joint financial adviser, corporate broker and sponsor for CRH and for no one else in connection with the

proposed acquisition and placing referred to in this document and is not, and will not be, responsible to anyone

other than CRH for providing the protections afforded to clients of UBS Limited, nor for providing advice in

connection with the placing described in this document.

J.P. Morgan Limited, which is authorised by the Prudential Regulation Authority in the United Kingdom and

regulated in the United Kingdom by the Prudential Regulation Authority and by the Financial Conduct

Authority, is acting as joint financial adviser for CRH and for no one else in connection with the proposed

acquisition and placing referred to in this document and is not, and will not be, responsible to anyone other

than CRH for providing the protections afforded to clients of J.P. Morgan Limited, nor for providing advice in

connection with the placing described in this document.

Merrill Lynch International, which is authorised by the Prudential Regulation Authority in the United Kingdom

and regulated in the United Kingdom by the Prudential Regulation Authority and by the Financial Conduct

Authority, is acting as joint financial adviser for CRH and for no one else in connection with the proposed

acquisition and placing referred to in this document and is not, and will not be, responsible to anyone other

than CRH for providing the protections afforded to clients of Merrill Lynch International, nor for providing

advice in connection with the placing described in this document.

J&E Davy, which is regulated by the Irish Financial Services Regulatory Authority in Ireland, is acting as joint

financial adviser, corporate broker and sponsor in Ireland for CRH and for no one else in connection with the

proposed acquisition and the placing referred to in this document and is not, and will not be, responsible to

anyone other than CRH for providing the protections afforded to clients of J&E Davy, nor for providing advice in

connection with the placing described in this document.

Goodbody Stockbrokers trading as Goodbody, is authorised and regulated in Ireland by the Central Bank of

Ireland, is acting as joint financial adviser for CRH and no one else in connection with the proposed acquisition

and placing described in this document and will not regard any other person (whether or not a recipient of this

announcement) as a client in relation to the proposed acquisition and placing described in this document and

will not be responsible to anyone other than CRH for providing the protections afforded to clients of Goodbody

Stockbrokers or for providing advice in relation to the proposed acquisition and placing described in this

document.

* 2014E is used throughout this announcement to indicate numbers which are approximate pending audit finalisation

Page 6 of 12

Acquisition Announcement – 2 Feb 2015

Appendix 1

Further details of the acquisition

Information on NewCo

The NewCo Group comprises a global portfolio of assets in the building materials industry, across 4 regional

platforms, currently owned by either Lafarge or Holcim:

1) Canada

• All of Holcim's assets in Canada, plus six US cement terminals and the Trident cement plant in

Montana, US.

2) Western Europe

• All of Lafarge's assets in the UK (post the acquisition by Lafarge of the remaining 50% of the Lafarge UK

joint venture) except for the Cauldon cement plant and related assets;

• All of Lafarge's assets in Germany; and

• All of Holcim's assets in France, except for the Altkirch plant and associated assets in the "Haut-Rhin"

region, all of Lafarge’s assets in La Reunion (except its minority shareholding in Ciments de Bourbon)

and the Saint Nazaire Lafarge grinding station.

3) Central and Eastern Europe

• All of Holcim's assets in Slovakia and Serbia, and all operating assets in Hungary; and

• All of Lafarge’s assets in Romania.

4) Emerging Markets

• The assets of Lafarge Republic, Inc. in the Philippines, except certain assets including the Iligan and

Mindanao cement plants; and

• Certain cement assets from Lafarge and Holcim's Brazilian footprint.

The gross assets of NewCo as at 30 September 2014 amounted to €7.8bn. Profit before tax for the year ended

31 December 2013 amounted to €0.2bn. This information is estimated. More detailed historical financial

information will be set out in the Shareholder Circular.

The NewCo businesses have operated, and until the closing date of the Acquisition will continue to operate, in

line with the customary practices of Lafarge and Holcim as regards sales, customers, suppliers, management,

employees, working capital, maintenance and capital expenditure.

CRH has existing business activities in most of the regions contemplated pursuant to the Acquisition, and

extensive experience in successfully integrating acquisitions into its footprint. Given the very limited overlap of

our operations and federal organisation structure, we would expect to fold the activities of NewCo into our

existing organisational structures in Europe, the Americas and Asia with the existing country level structures

and management of NewCo largely unchanged.

As a long term investor in the sector, CRH has a proud reputation as an employer of choice in the industry. As

an international company, we recognise the differences in custom and practice regarding employee

representation between countries. CRH intends to step into the shoes of Lafarge and Holcim in respect of

existing collective agreements etc. at a country level, so no negative impact for employees is anticipated arising

from a purchase of NewCo by CRH. Further, in common with Holcim and Lafarge, CRH is committed to the

highest international standards of employee safety and social and corporate responsibility. Accordingly, CRH

expects a very smooth transition in the area of safety, environmental management and employee relations.

* 2014E is used throughout this announcement to indicate numbers which are approximate pending audit finalisation

Page 7 of 12

Acquisition Announcement – 2 Feb 2015

Summary of Principal terms and Conditions of the Acquisition

Terms used in this summary are defined in the ‘Definitions' section of this announcement.

Key Terms

The CRH Group (through CRH International) has made a binding irrevocable offer (the "Offer") to acquire

NewCo from Lafarge and Holcim for a total EV of €6.5bn1.

Lafarge and Holcim may elect to accept the Offer following the conclusion of their works council consultation

process and have full discretion whether to do so. The Offer will remain open for acceptance until the earlier

of (a) two weeks following the conclusion of the works council consultation process and (b) 31 August 2015. It

is expected that the works council consultation will take in the region of two to three months.

The Global SPA is conditional on:

• Approval of the Acquisition by CRH’s shareholders at the EGM to be convened for that purpose;

• Successful completion of the Lafarge Holcim Merger; and

• Completion of certain local reorganisations that need to take place before closing of the Global SPA.

The long stop date for the Global SPA is the earlier of (a) three months following completion of the Lafarge

Holcim Merger and (b) 31 December 2015 but in any case no earlier than 31 August 2015.

As a Class 1 acquisition under the UKLA Listing Rules, the Acquisition is conditional on the approval of CRH’s

shareholders. CRH intends to issue a circular in February containing further details of the Acquisition and

convening the EGM, with the EGM likely to take place in March 2015. An ordinary resolution of CRH’s

shareholders is required to approve the Acquisition.

Break Fees

If the Acquisition is not approved by CRH’s shareholders at the EGM, a termination fee of approximately €157.8

million in total (equivalent to 1% of CRH’s market capitalisation immediately prior to the date of this

announcement) will be payable by CRH to Lafarge and Holcim.

An equivalent termination fee of approximately €157.8 million will be payable by Lafarge and Holcim to the

CRH Group in either of the following circumstances:

• If Lafarge and Holcim do not accept the Offer; or

• If the Lafarge Holcim Merger does not proceed to successful completion.

Conditions

To proceed to closing of the Global SPA, the CRH Group requires:

• anti-trust approval in Canada and in Serbia and from the EU Commission; and

• the approval of the identity of CRH as purchaser of NewCo by the Administrative Council for Economic

Defence in Brazil, by the Canadian Competition Bureau, by the European Commission and by the

Commission for the Protection of Competition in Serbia; and

• certain other non-antitrust regulatory approvals in a number of jurisdictions.

The CRH Group has given “hell or high water” commitments to Lafarge and Holcim in the Global SPA in order to

ensure it obtains all the required approvals to proceed to closing of the transaction. The Global SPA provides

that, if, notwithstanding CRH's commitment to take all steps and do all things necessary to obtain the required

regulatory approvals, any approval is not obtained by the long stop date for the Global SPA, then:

•

1

the Global SPA will proceed to completion in all jurisdictions other than that in which a required

regulatory approval has not been obtained; and

The total consideration of €6.5bn is based on exchange rates as at 30 January 2015. The consideration will be paid in a combination of

Euro, Sterling and Canadian Dollars.

* 2014E is used throughout this announcement to indicate numbers which are approximate pending audit finalisation

Page 8 of 12

Acquisition Announcement – 2 Feb 2015

•

a divestiture trustee will be appointed in respect of the jurisdictions in which required regulatory

approvals have not been obtained. The divestiture trustee's mandate will be to sell the relevant

business.

If the business proposed to be acquired pursuant to the Global SPA is sold for less than the price allocated to it

in agreements, this loss will be for the account of the CRH Group. Likewise, any profit on disposal will also

accrue to the CRH Group.

CRH has agreed to "hell or high water" commitments and to the fallback divestment provisions referred to

above to give Lafarge and Holcim the necessary execution certainty they require in the context of the Lafarge

Holcim Merger.

CRH does not anticipate any significant obstacle to obtaining all required regulatory approvals to the Global

SPA.

Other Terms and Non-Solicitation

The CRH Group has agreed to acquire NewCo (excluding the Philippines Business) on a cash free, debt free

basis, with normalised levels of working capital. The Global SPA contains customary provisions to reflect this

basis of acquisition.

The Global SPA contains customary warranties from Lafarge and Holcim in favour of the CRH Group, including

in particular in relation to title, financial information on NewCo's (excluding the Philippines Business),

compliance with law, antitrust, environmental matters, litigation, tax and material contracts. The warranties

are subject to customary limitations, including as to time, de minimis and deductible amounts and caps on

liability. Separately, the Global SPA contains a limited number of specific indemnities in favour of the CRH

Group. These indemnities are also subject to customary limitations.

CRH has agreed in the Global SPA that, for a period of not less than one year from closing of the Global SPA, it

will, in respect of NewCo, maintain employee benefits on at least as favourable terms to the current terms, to

not close a plant in that period, and not to engage in any collective redundancy programme or mass lay-off.

Where CRH disposes of any business within NewCo within 18 months of closing of the Global SPA, it has agreed

to share any profit on disposal equally with Lafarge and Holcim.

If the Offer is accepted by Lafarge and Holcim, then in those circumstances the Global Tax Deed would also

become effective. The Global Tax Deed is intended to indemnify the CRH Group against the pre-closing tax

liabilities of NewCo (excluding the Philippines Business).

Philippines Transaction

The Philippines SPA and the Philippines Tax Deed are in all material respects consistent with the Global SPA and

Global Tax Deed except in three important respects.

The Philippines SPA is conditional on CRH entering into arrangements with a local partner in the Philippines

between now and closing of the Philippines SPA so as to comply with the laws of the Philippines in relation to

restrictions on foreign ownership of Philippine assets.

CRH has had exploratory discussions with potential local partners and is confident that it will be able to finalise

these co-ownership arrangements to enable completion of the Philippines SPA. If appropriate arrangements

cannot be finalised by 15 August 2015, then in those circumstances, an independent investment bank will be

appointed on a basis identical in all material respects to the divestiture trustee provisions of the Global SPA

except that any profit on a disposal will be split 50:50 with Lafarge and any loss will be for the account of CRH.

Second, the Philippines SPA is conditional on the completion of the Global SPA.

* 2014E is used throughout this announcement to indicate numbers which are approximate pending audit finalisation

Page 9 of 12

Acquisition Announcement – 2 Feb 2015

Third, as part of the Philippines Business is contained in a listed company with minority shareholders, the CRH

Group will be required to make a mandatory cash offer to the minority shareholders in the same terms as

those which will be applicable to Lafarge in the Philippines agreement as at closing. The mandatory offer will

be structured such that completion of the mandatory offer will be contemporaneous with the completion of

the Philippines SPA.

Principal terms of the Financing

CRH proposes to finance the Acquisition through a combination of cash on balance sheet, new bank facilities

and the proceeds of an equity placing of approximately 9.99% of CRH's current issued share capital.

CRH has agreed a €6.5bn senior unsecured bridge loan facility with Bank of America Merrill Lynch International

Limited, J.P. Morgan Limited and UBS Limited (as bookrunners and mandated lead arrangers) and Bank of

America Merrill Lynch International Limited as Agent and Bank of America, N.A. as lender. Such facility consists

of a €2.0bn Tranche A with an original maturity date of 31 December 2015, a €3.5bn Tranche B with an original

maturity date of 30 June 2016, and a €1.0bn Tranche C with a maturity date of 30 June 2018 (together the

"Facilities"). The full amount of the Facilities is available to be utilised to complete the Acquisition.

CRH has the option to extend the maturity dates in respect of up to the full amount of Tranche A and Tranche B

twice, each time by a period of six months. The drawn amount of the Facilities shall bear interest at the rate of

EURIBOR plus a margin, which is subject to certain step-ups according to a time and credit ratings based

schedule. The undrawn amount of the Facilities shall, from one month after the date of the Facilities, incur a

fee calculated as a portion (which is subject to step ups over time) of the margin. All payments in respect of

interest and fees payable by CRH to the finance parties under the Facilities will be made in Euro. The Facilities

can be repaid prior to maturity without any break cost (provided that such repayment takes place at the end of

the interest period applicable to the relevant loan being prepaid).

Subject to certain carve-outs, the Facilities contain provisions requiring mandatory prepayment from disposal

proceeds and the proceeds of capital markets transactions. The Facilities contain customary representations

and undertakings in relation to the Acquisition. The terms and conditions are otherwise substantially similar to

CRH's existing €2.5bn revolving credit facility dated 11 June 2014.

Cash from balance sheet of €2.0bn will also be used to fund the Acquisition.

* 2014E is used throughout this announcement to indicate numbers which are approximate pending audit finalisation

Page 10 of 12

Acquisition Announcement – 2 Feb 2015

Management and employees

CRH attaches great importance to the skills and experience of the existing management and employees of

NewCo, who are expected to contribute to the success of the Combined Group.

General Meeting

As a result of its size, the Acquisition constitutes a Class 1 transaction for the purposes of both the UK and Irish

Listing Rules and is therefore conditional upon the approval of CRH’s Shareholders. A General Meeting will be

convened in due course. The purpose of the General Meeting is to consider, and if thought fit, pass a resolution

to approve the Acquisition.

Recommendation

The Board considers that the Acquisition is in the best interests of the Shareholders as a whole. Accordingly,

the Board intends to recommend that Shareholders vote in favour of the resolution to approve the Acquisition

to be put to the EGM, as all Directors intend to do in relation to their own beneficial shareholdings, which in

aggregate amount to 319,740 shares as at 1 February 2015, representing approximately 0.043% of the total

number of voting rights in the Company as at that date.

Further Information

Further details in relation to the Acquisition will be set out in the Shareholder Circular which is expected to be

published in February 2015. CRH Shareholders' attention is drawn, in particular, to the risk factors which will be

described in detail in the Shareholder Circular.

Definitions

“Acquisition” means the proposed acquisition by the CRH Group of NewCo;

“Binding Offer Letter” means the irrevocable offer by the CRH Group addressed to Lafarge and Holcim to

acquire NewCo (excluding the Philippines Business pursuant to the terms of the Global SPA);

“Can $” means Canadian dollars;

“CHF” means Swiss francs;

“CRH Group” means CRH plc and/or its subsidiary undertakings;

"EBITDA" means Earnings Before Interest, Taxation, Depreciation and Amortisation;

“EGM” means the extraordinary general meeting to be convened by CRH for the purpose of considering an

ordinary resolution to approve the Acquisition;

“Global SPA” means the share purchase agreement pursuant to which the CRH Group will acquire the Target

Company excluding the Philippines Business;

“Global Tax Deed” means the tax deed between the CRH Group, Lafarge and Holcim in relation to NewCo

(excluding the Philippines Business);

“Lafarge Holcim Merger” means the proposed merger of Lafarge and Holcim by way of tender offer in

accordance with the Guide Regulations of the AMF and the Rules of Euronext Paris;

"NewCo” means the entities to be acquired by the CRH Group pursuant to the Global SPA and the Philippines

SPA.

* 2014E is used throughout this announcement to indicate numbers which are approximate pending audit finalisation

Page 11 of 12

Acquisition Announcement – 2 Feb 2015

“Offer” the offer made by the CRH Group to acquire NewCo excluding the Philippines Business under the

Binding Offer Letter;

“Philippines Business” means the entities to be acquired by the CRH Group pursuant to the Philippines SPA;

“Philippines SPA” means the share purchase agreement pursuant to which the CRH Group will acquire the

Philippines Business;

“Philippines Tax Deed” means the tax deed in relation to the Philippines Business;

“Shareholders” mean the holders of ordinary shares in CRH plc; and

“Sterling” means pounds sterling.

Disclaimer

UBS Limited ("UBS") is authorised by the Prudential Regulation Authority and regulated in the United Kingdom

by the Financial Conduct Authority is acting as joint financial adviser, corporate broker and sponsor for the

Company in connection with the matters set out in this announcement; J.P. Morgan Limited ("JPM"), which is

authorised by the Prudential Regulation Authority in the United Kingdom and regulated in the United Kingdom

by the Prudential Regulation Authority and by the Financial Conduct Authority, is acting as joint financial

adviser for CRH in connection with the matters set out in this announcement; Merrill Lynch International

("BAML"), which is authorised by the Prudential Regulation Authority in the United Kingdom and regulated in

the United Kingdom by the Prudential Regulation Authority and by the Financial Conduct Authority, is acting as

joint financial adviser for CRH in connection with the matters set out in this announcement; and J&E Davy

("Davy"), which is regulated by the Irish Financial Services Regulatory Authority in Ireland, is acting exclusively

as joint financial adviser, corporate broker and sponsor (in Ireland) for CRH in connection with the matters set

out in this announcement (each of UBS, JPM, BAML and Davy a "Bank" and collectively the "Banks"). Each Bank

is not, and will not be, responsible to anyone other than CRH for providing the protections afforded to its

respective clients or for providing advice in relation to the proposed acquisition or any other matters referred

to in this announcement. Apart from the responsibilities and liabilities, if any, which may be imposed on any

Bank by the Financial Services and Markets Act 2000, each Bank accepts no responsibility whatsoever and

makes no representation or warranty, express or implied, for the contents of this announcement, including its

accuracy, fairness, sufficiency, completeness or verification or for any other statement made or purported to

be made by it, or on their behalf, in connection with CRH or the acquisition, and nothing in this announcement

is, or shall be relied upon as, a promise or representation in this respect, whether as to the past or the future.

Each Bank accordingly disclaims to the fullest extent permitted by law all and any responsibility and liability

whether arising in tort, contract or otherwise (save as referred to above) which they might otherwise have in

respect of this announcement or any such statement.

This announcement shall not constitute an offer to buy, sell, issue, or acquire, or the solicitation of an offer to

buy, sell, issue, or acquire any securities in the United States (including its territories and dependencies, any

state of the United States and the District of Columbia), Australia, Canada, Japan, South Africa, Jersey or any

other state or jurisdiction where such offer for sale of securities would be unlawful. The contents of this

document should not be construed as legal, business, financial, tax, investment or other professional advice.

This announcement is not for publication, distribution or release, directly or indirectly, in or into the United

States (including its territories and dependencies, any state of the United States and the District of Columbia),

Australia, Canada, Japan, Jersey or any other state or jurisdiction where such distribution would be unlawful.

The securities of CRH have not been and will not be registered under the US Securities Act of 1933, as amended

(the "Securities Act"), or with any securities regulatory authority of any state or jurisdiction of the United

States, and may not be offered, sold, resold or otherwise transferred, directly or indirectly, in or into the United

States except pursuant to an exemption from, or in a transaction not subject to, the registration requirements

of the Securities Act and in compliance with any applicable securities law of any state or other jurisdiction of

the United States. Any sale in the United States of the securities mentioned in this announcement will be made

solely to "qualified institutional buyers" (within the meaning of Rule 144A under the Securities Act) who are

* 2014E is used throughout this announcement to indicate numbers which are approximate pending audit finalisation

Page 12 of 12

Acquisition Announcement – 2 Feb 2015

also "accredited investors" (as defined in Rule 501(a) (1), (2), (3) or (7) of Regulation D under the Securities Act)

in transactions not involving a "public offering" and in accordance with an exemption from registration under

the Securities Act. There will be no public offer of securities in the United States.

This announcement contains or incorporates by reference "forward-looking statements". These forwardlooking statements may be identified by the use of forward-looking terminology, including the terms

"believes", "estimates", "anticipates", "projects", "expects", "intends", "aims", "plans", "predicts", "may",

"will", "seeks", "could", "would", "shall" or "should" or, in each case, their negative or other variations or

comparable terminology, or by discussions of strategy, plans, objectives, goals, future events or intentions.

These forward-looking statements include all matters that are not historical facts and include statements

regarding the intentions, beliefs or current expectations of the Board concerning, among other things, the

Company's results of operations, financial condition, prospects, growth, strategies and the industries in which

the Company operates.

By their nature, forward-looking statements involve risks and uncertainties because they relate to events and

depend on circumstances that may or may not occur in the future or are beyond the Company's control and

difficult to predict, that could cause actual results and performance to differ materially from any expected

future results or performance expressed or implied by the forward-looking statement, including those

accompanying such forward-looking statements and under “Risk Factors” in our Annual Report on Form 20-F,

filed with the U.S. Securities and Exchange Commission (the “S.E.C.”) on March 13, 2014 and “Principal Risks

and Uncertainties” in our 2014 Interim Results contained in our Form 6-K filed with the S.E.C. on August 20,

2014. Forward-looking statements are not guarantees of future performance and are based on one or more

assumptions. The Company's actual results of operations and financial condition and the development of the

industries in which the Company operates may differ materially from those suggested by the forward-looking

statements contained in this announcement. In addition, even if the Company's actual results of operations,

financial condition and the development of the industries in which the Company operates are consistent with

the forward-looking statements contained in this announcement, those results or developments may not be

indicative of results or developments in subsequent periods.

The forward-looking statements contained in this announcement speak only as of the date of this

announcement. The Company and the Board expressly disclaim any obligations or undertaking to , and do not

intend to, update or revise publicly any forward-looking statements, whether as a result of new information,

future events or otherwise, unless required to do so by the FCA, the London Stock Exchange, the Irish Stock

Exchange, the Central Bank of Ireland or by applicable law. No statement in this announcement is or is

intended to be a profit forecast or profit estimate or to imply that the earnings of the Company for the current

or future financial years will necessarily match or exceed the historical or published earnings of the Company.

Where information contained in this announcement has been sourced from a third party (including Holcim

and/or Lafarge), the information has been accurately reproduced and, so far as the Company is aware and has

been able to ascertain from that information, no facts have been omitted which would render the reproduced

information, or information derived from it, inaccurate or misleading.

* 2014E is used throughout this announcement to indicate numbers which are approximate pending audit finalisation

© Copyright 2026