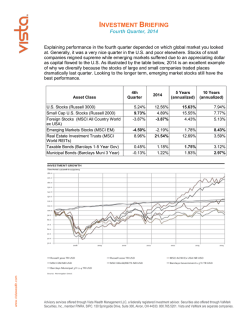

Pitchbook - Sag Harbor Advisors

SAG HARBOR ADVISORS SAG HARBOR ADVISORS REGISTERED INVESTMENT ADVISORS JAMESSANFORD M SANFORD JAMES FOUNDER++PORTFOLIO PORTFOLIOMANAGER MANAGER FOUNDER P.O. BOX 2219 PO BOX 2219 SAGHARBOR HARBORNY NY11963 11963 SAG 1 WWW.SAGHARBORADVISORS.COM WWW.SAGHARBORADVISORS.COM [email protected] [email protected] P:631-740-4498 P:631-740-4498 FAX: 631-204-6960 F: 631-204-6960 SAG HARBOR ADVISORS TABLE OF CONTENTS OVERVIEW PAGE 3 LONG ONLY BUY AND HOLD IS DEAD PAGE 4 EQUITY RISK CONCERNS PAGE 5 THE REAL “GREAT ROTATION” TRADE PAGE 6 DIFFERENTIATING FACTORS PAGE 7 PORTFOLIO OBJECTIVES PAGE 8 INVESTMENT PROCESS PAGE 9 INVESTMENT PROCESS EXAMPLE: HIGH YIELD CLOSED END FUNDS (CEFs) PAGE 10 INVESTMENT PROCESS EXAMPLE: SHORT TESLA PAGE 11 INVESTMENT PROCESS EXAMPLE: SHORT NASDAQ 100 (QQQ) PAGE 12 INVESTMENT PROCESS EXAMPLE: DIVIDEND STOCKS: CODI PAGE 13 INVESTMENT PROCESS EXAMPLE: MLPs- REFINERS PAGE 14 INVESTMENT PROCESS EXAMPLE: MLPS- NATURAL GAS PAGE 15 BACKGROUND PAGE 16 FEES/TRANSPARENCY PAGE 17 JAMES SANFORD FOUNDER + PORTFOLIO MANAGER PO BOX 2219 SAG HARBOR NY 11963 2 WWW.SAGHARBORADVISORS.COM [email protected] P:631-740-4498 F: 631-204-6960 SAG HARBOR ADVISORS OVERVIEW • • Sag Harbor Advisors (SHA) is a new type of PERFORMANCE FEE-ONLY Registered Investment Advisor which only receives fees as a percentage of the return, and nothing else. SHA has no broker dealer affiliation or Registered Rep license, for which sole purpose is to legally allow the advisor to collect commissions on the sale of products like mutual funds SHA does not receive sales kickbacks from mutual funds, 529s, or other 3rd party investment products. Other Financial Planners and RIAs often put clients in mutual funds that maximize commissions and fees, in the form of legal kickbacks from the mutual fund company. • Sag Harbor Advisors is a Registered Investment Advisor and obligated to act as a FIDUCIARY and solely in the interest of clients, unlike a BROKER. Brokers are only required to abide by the SUITABILITY RULE. • Majority of Financial Planners earn their revenue on commission of the sales of investment products, especially equity mutual funds, through dual registrations with broker dealers. Despite being defined as Fiduciaries, the SEC and FINRA do not prohibit this. Advisors have no legal obligation to disclose any commission arrangement. In this current zero interest rate environment where the fees on conservative fixed income, bond related investments have declined substantially, the skewed incentives to put clients into equity mutual funds and massive resulting conflict of interest HAVE NEVER BEEN GREATER. JAMES SANFORD FOUNDER + PORTFOLIO MANAGER PO BOX 2219 SAG HARBOR NY 11963 3 WWW.SAGHARBORADVISORS.COM [email protected] P:631-740-4498 F: 631-204-6960 LONG ONLY “BUY AND HOLD” IS DEAD SAG HARBOR ADVISORS • The SHA portfolio consists of a long/short equity strategy, focusing on long value/high dividend equities and fixed income instruments, over laid with a short portfolio of high multiple, momentum stocks. Target annual returns are 10-15% with a focus on capital preservation in market declines. SHA targets flat to positive returns in periods of US equity index declines of over 5%. Portfolio is actively traded to manage alpha, and stay ahead of geo-political events. Large portfolio turnover in case of major political, economic, or monetary policy changes. • Long only “buy and hold” investing is dead. Over $50 billion has been raised in 2014 by mutual funds setting up “alternative strategies” that engage in strategies other than just buying only stocks. These funds are shorting stocks in addition, as well as investing in fixed income and commodities exchange listed vehicles. • Long run average returns of the stock market are 7%, but if you take out the 1982-2000 period, they are much lower. Coming retirement of baby boomers, the largest population bubble in US history, coupled with that generation’s love of stocks as an investment, will lead to massive net liquidation of US equities over the next 15 years, making this 7% number very hard to achieve. GenXers and Millenials generation aren’t big enough nor as ebullient on equities due to their exposure to the “crisis era” consisting of 40% declines in 2000 and 2008, as well as mini-crisis years of 1998 and 2011. “Equity culture” mindset less prevelant in GenXers, Millenials than in Boomers. Who will buy up the Boomers liquidation? • Dividend and income return will be more crucial for investing going forward, along a with short stock portfolio. JAMES SANFORD FOUNDER + PORTFOLIO MANAGER PO BOX 2219 SAG HARBOR NY 11963 4 WWW.SAGHARBORADVISORS.COM [email protected] P:631-740-4498 F: 631-204-6960 SAG HARBOR ADVISORS EQUITY RISK CONCERNS • Current intention of the Federal Reserve to end 5 years of abnormally low interest rate environment and the end of more recent Quantitative Easing program make a “buy and hold” or “long-only” strategy outdated and ill-advised. 30+% returns on equity indices in 2013 fueled by historically unprecedented money printing, or Quantitative easing (QE) which is now due to end by June 2015 according to FED Governor survey. • Valuation of momentum-driven internet stocks, with no profits, a deep concern. Stocks trading at multiples of revenues not seen since 1999-2000 period. Non standard value metrics like “clicks” and “eyeballs” have returned. • USA economy lone man standing. Significant weakness in Europe and Japan creating earnings drag for US multinationals. Resurgent strong dollar hurting US earnings as well as commodity prices. Sharp crude oil decline leads Russia, Venezuela and possibly Brazil, Canada, Australia into recession. Possible banking collapse in Russia. • Weak commodity prices causing wave of Corporate defaults, especially in Energy and Iron Ore miners. Correction in Junk and Corporate bonds of 7% in late 2014, not matched yet by US equity indices despite high correlation. Dispersion of performance between corporate bonds and equities unprecedented. Downgrades to US energy and natural resources company earnings causing P/E multiple expansion for US equities. • • Coming retirement liquidation of baby boomer generation holdings will depress long run average return of US stock market indices, well below its 7% average. Largest retirement bubble in US history replaced by GenXers and Millenials less trustworthy of the “Equity Culture” . “Crisis Era” is not over. Russian invasion of Ukraine re-opens Cold War and reignites geopolitical tensions not seen since 1987. Iraq vs ISIS militant crisis threatens large oil producer, opens Shiite-Sunni divide. 2011-style Greek crisis is back, with January Greek elections leading to potential Greek euro exit, Greek banks collapse. JAMES SANFORD FOUNDER + PORTFOLIO MANAGER PO BOX 2219 SAG HARBOR NY 11963 5 WWW.SAGHARBORADVISORS.COM [email protected] P:631-740-4498 F: 631-204-6960 HE REAL “GREAT ROTATION” TRADE SAG HARBOR ADVISORS • The real great rotation trade is the unloading of equity holdings by retiring baby Boomers, the largest population bubble in American history. 2012 study done by Arnott and Chaves reveals that a 1% higher concentration of 70+ year olds leads to DECREASE of annual excess equity returns of 2% (SOURCE: “Absolute Return Letter” October 2013) • Boomers experienced the heyday of stock market investing, 1982-2000 and became believers in the “equity culture”. They have the largest equity holdings ( 60%) of any other American generation and constitute 40% of its consumer spending ( McKinsey Global Institute June 2012) • GenXers and Millenials lived through the “Crisis Era” with 40% stock market declines in 2000 and 2008, and mini-crisis of 1998 and 2011. They are not as big believers in the “equity culture” nor a big enough segment of the population to absorb the coming selling. • US investors over age 65 reduce equity holdings to an average 27% of their net worth, down from 47% for 35-65 year olds and 51% for those under 35. ( McKinsey Global Institute June 2012) • Federal Reserve Bank of San Francisco(FRBSF) in 2011 finds a powerful relationship between age distribution of population and the Price earnings ratio of US equity indices, which they call the “M/O” ratio. FRBSF finds this ratio predicts 60% of the change in equity valuations over past 60 years. FRBSF predicts falling price earnings ratios to 8-9x earnings in the mid 2020s. (SOURCE: “Absolute Return Letter” October 2013) JAMES SANFORD FOUNDER + PORTFOLIO MANAGER PO BOX 2219 SAG HARBOR NY 11963 6 WWW.SAGHARBORADVISORS.COM [email protected] P:631-740-4498 F: 631-204-6960 SAG HARBOR ADVISORS DIFFERENTIATING FACTORS • Background: 20 years of trading experience in a wide variety of products. In addition to equities, these range from equity derivatives, convertible bonds, high yield and corporate bonds, credit derivatives, and mortgage backed derivatives. Depth of institutional trading floor experience very rare among RIAs. • Fixed Income Experience: Broad depth of knowledge of credit and equity derivatives and corporate bonds often lacking among equity PMs. US markets are poised for a major asset rotation out of bonds, as a period of unprecedented low rates comes to an end, rendering Fixed Income experiences crucial. • Performance Fee-only structure. SHA receives only a portion of the return, 20%, as long as returns are north of 3%. There is no “wrap” or management fee. No fees for returns under 3% • PM invested in same portfolio. Clients may request personal account statements • PM an actual trader, not just an asset harvester: Mr. Sanford doesn’t come from a fee gathering or administration background, and has worked on an institutional trading floor as well as an exchange floor for 21 years. • NO Broker-Dealer dual license. Advisor can NOT collect commissions on the sale of investment products, eliminating conflict of interest. JAMES SANFORD FOUNDER + PORTFOLIO MANAGER PO BOX 2219 SAG HARBOR NY 11963 7 WWW.SAGHARBORADVISORS.COM [email protected] P:631-740-4498 F: 631-204-6960 SAG HARBOR ADVISORS PORTFOLIO OBJECTIVES • 10-15% returns • Capital preservation. Flat to mildly positive returns in down markets via short picks in higher beta stocks. • Target income from dividend stocks and fixed income vehicles • Focus on value stocks • Contrarian view • Active portfolio management and turnover. Long term “buy-and-hold” is dead. • Stay in front of current events in Europe, disclocation in High Yield bond and Energy stocks, UST market technicals. • Efficient market hypothesis doesn’t hold. • 20-50% short overlay in high P/E momentum fad stocks. • Use up to 1.5/1 leverage if market views warrant. • Use only financially strong custodian (currently using TD Ameritrade). Never hold portfolio margin accounts or domicile funds in small broker-dealers. JAMES SANFORD FOUNDER + PORTFOLIO MANAGER PO BOX 2219 SAG HARBOR NY 11963 8 WWW.SAGHARBORADVISORS.COM [email protected] P:631-740-4498 F: 631-204-6960 SAG HARBOR ADVISORS INVESTMENT PROCESS • Identify equities with SUSTAINABLE high dividends in the 5-9% range. • Value stocks trading at low multiples due to irrational fund outflows. • Identify short equity candidates at extreme multiples experiencing irrational fund inflows and unsustainable momentum • Short candidates that have beat and raised estimated 5-7 times. Bar raised to unsustainable expectations • Avoid high fee mutual funds. Exposure can be achieved with low fee, liquid ETFs • Fixed income closed end funds trading below net asset value. • Preferred stocks with low duration. Portfolio currently avoiding fixed income duration risk, but poised to act in market volatility. Fixed income closed end funds overreact to sharp 10yr UST moves, and may be better rate plays than UST bonds themselves. • Rely on sell side research as well as publicly available fee based internet research • Idea sharing with former hedge fund clients and sell-side colleagues is key. JAMES SANFORD FOUNDER + PORTFOLIO MANAGER PO BOX 2219 SAG HARBOR NY 11963 9 WWW.SAGHARBORADVISORS.COM [email protected] P:631-740-4498 F: 631-204-6960 INVESTMENT PROCESS EXAMPLE: HIGH YIELD CEFs SAG SAG HARBOR HARBOR ADVISORS ADVISORS • High yield asset class correction, down 7% from 2014 highs. Spread-to-worst 150 bps wider than 2014 tights. • Closed end funds (CEFs) offer diversified high yield play, discounts to Net Asset value, lower fees • Ticker BTZ, Blackrock Credit Allocation, 7.17% current yield, 12% cheap to net asset value. • CEFs trade on exchanges, highly liquid, no minimum holding period. • BTZ pays dividend monthly. $1.46bb market cap. Modest leverage of 1.47/1. • Other Closed End Funds : FTF, Franklin Short Duration High Yield Fund, BLW, BHK. JAMES SANFORD FOUNDER + PORTFOLIO MANAGER PO BOX 2219 SAG HARBOR NY 11963 10 WWW.SAGHARBORADVISORS.COM [email protected] P:631-740-4498 F: 631-204-6960 INVESTMENT PROCESS EXAMPLE: SHORT TESLA (TSLA) • Ticker: TSLA, $206.05, $26BB market cap, 353x forward EPS. Musk says TSLA “ wont be profitable until 2020” at Detroit Auto Show. Equity valuation reflects “cult stock” status, superhero model of Elon Musk. Auto industry standard risk not priced into this stock. • Current valuation reflects sales assumption of 500,000 cars by 2020. Current sales only 32,000! Guided down from 35,000 in for 2014. • Musk is CEO of 3 firms, a major negative. Large time obligations to SpaceX, Hyperloop, Solar City. No other firm could get away with this. • Major competition emerges 2017. Electric Vehicles (EV) crowded field. GM Bolt, BMW i3 at low priced end, Audi R-8 E-tron at high end. Porshe, Volvo, Mercedes, Toyota (hybrids) launching vehicles. • US sales growth declining. China sales “fell of a cliff in late 2014” according to Musk ( Detroit Auto Show). Where is the growth region? • Delays on release of Model X, Model 3. Timeline pushed out, stock valuation can not afford it. Possible design flaw of Model X “ Crossover SUV” Too small, wing doors preclude a roof rack . • TSLA “Giga-factory” in Nevada, costing $6bb to manufacture Panasonic batteries for EVs becomes obsolete? Threat from new “solid” state technology pursued by Volvo. • Large scale use of Lithium and Cobalt in batteries leads to price surge in Rare Earths and thus battery cost? Renders impossible attempted price decreases to appeal to mass market. SANFORD .JAMES FOUNDER + PORTFOLIO MANAGER PO BOX 2219 SAG HARBOR NY 11963 11 SAG HARBOR ADVISORS WWW.SAGHARBORADVISORS.COM [email protected] P:631-740-4498 F: 631-204-6960 INVESTMENT PROCESS EXAMPLE: SHORT QQQ ( NASDAQ 100 INDEX) • Ticker: QQQ, NASDAQ 100 stock market index, consisting of high beta growth/technology stocks up 60% over previous 24 months during largest period of Federal Reserve Quantitative easing and zero interest rates. • High beta stocks deemed most sensitive to economic rebound have high embedded expectations of economic growth, and returns have been fueled by FED artificial stimulus. Economic growth already priced in, now facing international headwinds of weak economy Europe, Japan, energy/resources led recession in Canada, Australia, Brazil • Highest P/E index within US benchmark equities indices. Heavily dependent on Apple (13.5%), Microsoft, Google, Facebook, Intel, Amazon, Cisco. • Non QQQ sectors like Crude oil, iron ore, copper down >50% last 12 months. Non-Nasdaq Industrials/Resource stocks cheapest by comparison in years. Large sector rotation coming? JAMES SANFORD FOUNDER + PORTFOLIO MANAGER PO BOX 2219 SAG HARBOR NY 11963 12 SAG HARBOR ADVISORS WWW.SAGHARBORADVISORS.COM [email protected] P:631-740-4498 F: 631-204-6960 INVESTMENT PROCESS EXAMPLE: DIVIDEND STOCKS- CODI: • Ticker: CODI, Compass Diversified, 6.25x forward EPS, 8.72% div yield. • “Off the grid” diversified holding company investing in a wide variety of businesses, similar to a “mini Berkshire Hathway”. Down 13% from 2014 highs. • IPOs of incubated subsidiary businesses create value-unlocking opportunities. $900mm market cap. Owns $225mm or 40% of recently IPO’d FOXF, Fox Factory Holdings, a source of divestiture cash for reinvestment/ dividends. Accounts for 25% of market cap. • CODI just issued 6mm share secondary in Nov 2014, first in 4 years. Rare issuance overhang behind us? JAMES SANFORD FOUNDER + PORTFOLIO MANAGER PO BOX 2219 SAG HARBOR NY 11963 13 SAG HARBOR ADVISORS WWW.SAGHARBORADVISORS.COM [email protected] P:631-740-4498 F: 631-204-6960 INVESTMENT PROCESS EXAMPLE: MLPs- REFINERS- NTI • MLPs, or Master Limited Partnerships, linked to energy infrastructure in the USA are historically less correlated with commodity oil prices, yet suffered by sector association with the 50% down move in crude oil and 50-70% downward move in Oil Exploration and Production stocks, creating opportunities. “Baby in the bathwater”. Refiners, Natural Gas, and “Midstream” energy companies focused on transportation and storage trade at opportunistic levels • MLPs pay high dividends which can grow over time, raging from 5-10%. Dividends are not taxed until the asset is sold, creating a tax advantaged holding. • Ticker: NTI, Northern Tier Energy, $21.53, is a singlerefinery variable MLP in Minnesota which cracks North Dakota Bakken and Canadian Oil-Sands crude, which are plentiful in supply with limited sales outlets. NTI realizes larger crack spreads than other refineries • NTI's trailing dividend yield is 12.6%! Refiners face a risk of accidents or temporary maintenance shutdown, a risk more than compensated with that yield JAMES SANFORD FOUNDER + PORTFOLIO MANAGER PO BOX 2219 SAG HARBOR NY 11963 14 SAG HARBOR ADVISORS WWW.SAGHARBORADVISORS.COM [email protected] P:631-740-4498 F: 631-204-6960 INVESTMENT PROCESS EXAMPLE: MLPS- NATURAL GAS- EXLP • Ticker: EXLP, Exterran Partners, Natural Gas midstream firm, 9.92% div yield (highest ever). Focuses on natural gas compression services. • All MLPs including Nat Gas traded off with Crude Oil E&P MLPs regardless of zero crude exposure. Natural Gas is a regional commodity independent of OPEC or Middle Eastern geopolitical issues. • Stock at 5 year lows, off 25% from its highs since September 2014. • USA has major Nat Gas reserves greater than domestic demand. Lifting of export ban to be a boon for compressor, liquification and transportation firms • Nat Gas replacing coal fired utilities, as well as Nuclear, given post-Fukishima concerns. Far less carbon content than Coal or Crude Oil. US trucking fleet slowly switching to gas fired vehicles. JAMES SANFORD FOUNDER + PORTFOLIO MANAGER PO BOX 2219 SAG HARBOR NY 11963 15 SAG HARBOR ADVISORS WWW.SAGHARBORADVISORS.COM [email protected] P:631-740-4498 F: 631-204-6960 SAG HARBOR ADVISORS FEES/TRANSPARENCY • 20% of return and nothing else. No fees is returns are under 3% annualized. • T+1 liquidation. Clients may un-designate the RIA and take control of portfolio intraday, or request liquidation • Website client view at TD Ameritrade. • Clients may move money fee-free in and out of portfolio account to a checking account • All funds domiciled at an entity independent of RIA. Current custodian TD Ameritrade • All administration done by TD, statements prepared independently • NO RIA control over custody of funds, no preparation of returns, statements. • Audited returns calculated daily by Blueleaf. • PM invested in portfolio in an amount equal or greater to 80% if personal liquid net worth. Clients may access PM’s account statement at any time. JAMES SANFORD FOUNDER + PORTFOLIO MANAGER PO BOX 2219 SAG HARBOR NY 11963 16 WWW.SAGHARBORADVISORS.COM [email protected] P:631-740-4498 F: 631-204-6960 SAG HARBOR ADVISORS BACKGROUND JAMES M SANFORD, CFA, the Founder and Portfolio Manager of Sag Harbor Advisors has worked on Wall Street since 1991. Mr. Sanford, formerly a Managing Director, served as an Institutional Sales Trader to Hedge Fund clients for 18 years from 1994-2012. The final 2 years of his banking career were spent at boutique firm Gleacher & Co, marketing high yield, investment grade, distressed and subordinate corporate bonds as well as preferred stocks to hedge funds. Prior to that he spent 11 years as a Managing Director at Credit Suisse from 1999-2010 marketing credit derivatives and convertible bonds. From 2005-2007 Mr. Sanford managed a 6 person Hedge Fund Credit Sales team at Credit Suisse within the overall Credit Sales group and was the #1 US salesperson by revenue in 2007 and 2008. Mr Sanford performed a similar sales role at JP Morgan from 1993-1999 on the JP Morgan Institutional Equity Derivative and Convertible Bond Group. His first job after graduating from Amherst College in 1991 was as a trading assistant for a Specialist firm on the American Stock Exchange from 1991-1993. Mr Sanford, who completed his 3 year CFAS program in 1998, has a vast wide ranging product background, a rarity for RIAs and even most Equities Portfolio Managers. Please see his complete resume which is attached in Appendix A. JAMES SANFORD FOUNDER + PORTFOLIO MANAGER PO BOX 2219 SAG HARBOR NY 11963 17 WWW.SAGHARBORADVISORS.COM [email protected] P:631-740-4498 F: 631-204-6960 SAG HARBOR ADVISORS DISCLAIMER • These materials are for discussion purposes only and do not constitute an offer to sell or a solicitation of an offer to purchase interests in any product or fund, which can only be made pursuant to an Offering Memorandum. The recipient of the materials is deemed to have agreed not to (i) reproduce or distribute these materials and (ii) disclose any information contained in these materials without the prior written consent of Sag Harbor Advisors.. • The data and information used in the accompanying Analysis contained herein have been obtained from sources that Sag Harbor Advisors and/or its affiliates ( “SHA”) believe to be reliable, subject to change without notice, its accuracy is not guaranteed, and it may not contain all material information concerning the securities which may be the subject of the analysis. Neither SHA nor its affiliates make any representation regarding, or assume responsibility or liability for, the accuracyor completeness of, or any errors or omissions in, any information that is part of the analysis. SHA may have relied upon certain quantitative and qualitative assumptions when preparing the analysis which may not be articulated as part of the analysis. The realization of the assumptions on which the analysis was based are subject to significant uncertainties, variability and contingencies and may change materially in response to small changes in the elements that comprise the assumptions, including the interaction of such elements. Furthermore, the assumptions on which the analysis was based may be necessarily arbitrary, may made as of the date of the analysis, do not necessarily reflect historical experience with respect to securities similar to those that may be the contained in the analysis, and does not constitute a precise prediction as to future events. • Because of the uncertainties and subjective judgments inherent in selecting the assumptions and on which the analysis was based and because future events and circumstances cannot be predicted, the actual results realized may differ materially from those projected in the Analysis. Nothing included in the analysis constitutes any representations or warranty by SHA as to future performance. No representation or warranty is made by SHAas to the reasonableness, accuracy or sufficiency of the assumptions upon which the analysis was based or as to any other financial information that is contained in the analysis, including the assumptions on which they were based. Members of the SHA shall not be liable for either (i) any errors or omissions made in disseminating the data or analysis contained herein or (ii) damages (incidental, consequential or otherwise) which may arise from your or any other party’s use of the data or analysis contained herein. The information that contained in the analysis should not be construed as financial, legal, investment, tax, or other advice. You ultimately must rely upon it’s own examination and professional advisors, including legal counsel and accountants as to the legal, economic, tax, regulatory, or accounting treatment, suitability, and other aspects of the analysis. SHA does not assume any responsibility for investment decisions. • This document is for informational purposes and does not constitute an offer to sell or buy any securities, and may not be relied upon in connection with any offer to sell or buy any securities JAMES SANFORD FOUNDER + PORTFOLIO MANAGER PO BOX 2219 SAG HARBOR NY 11963 18 WWW.SAGHARBORADVISORS.COM [email protected] P:631-740-4498 F: 631-204-6960 SAG HARBOR ADVISORS JAMES SANFORD FOUNDER + PORTFOLIO MANAGER PO BOX 2219 SAG HARBOR NY 11963 19 WWW.SAGHARBORADVISORS.COM [email protected] P:631-740-4498 F: 631-204-6960

© Copyright 2026