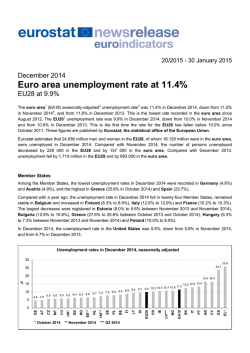

IMF Surveillance in Europe (PDF) - European Central Bank